Four hot roll-ups we are avoiding

Avoca Investment Management

Avoca Investment Management

Everyone loves a roll-up: Buy assets on a lower multiple to the one that you currently trade on and grow EPS. It’s as simple as that. Often the strategy doesn’t even require synergies to make it work. It can work whether or not the underlying market is exhibiting growth. If you operate in a highly fragmented industry not driven by IP, the opportunity for seemingly limitless EPS growth is palpable. But whilst roll-ups have the potential to perform well for extended periods, they can prove to be a dangerous style of investment for four reasons:

- The PE re-rate that the market generally imputes to a roll-up as it progresses means that the velocity of roll-up has to accelerate over time to ‘feed the beast’;

- Almost by definition, the quality of targets diminishes as the roll-up progresses;

- The size of acquisition has to keep growing to maintain the growth meaning strategy can morph from well-judged bolt-ons to ill-judged blockbusters (e.g. Slater & Gordon); and

- As a result of the first three points, often the rollup nears its PE zenith just at the point that the market refuses to keep funding the roll-up. This can drive simultaneous EPS downgrades and PE collapse resulting in catastrophic stock price decline.

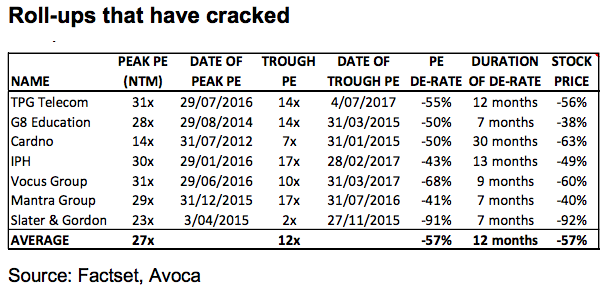

Professional investors are usually aware of this phenomenon but generally think they are prescient enough to ride the upswing and get off before the downswing. No doubt some investors are indeed clever enough to do just this. But the speed of PE collapse can surprise even the most astute investors. The table below highlights that whilst some roll-ups de-rate gradually, some do so more rapidly if a surprise event intercedes.

The event that triggered each of these collapses varied. For TPM, it was a shock margin contraction in FY 17 guidance driven by NBN transition. For GEM, it was buying Sterling Child Care at higher than typical EV/EBIT multiples as ‘a defensive move’ to shut out a competitor. For VOC, it was a series of downgrades driven by a combination of NBN-related issues and under-delivering acquisitions (such as NextGen). For MTR, it was a combination of downgrades driven by poor occupancy in the resource states of Queensland and WA, and a large acquisition in Hawaii that surprised the market (not in a good way).

So our view on roll-ups is to proceed with caution. As the duration of the roll-up lengthens and the PE rerate becomes more stretched, proceed with extreme caution.

4 hot roll-ups

In our space, the current ‘hot’ roll-ups are Corporate Travel Management (CTD), AMA Group (AMA), Costa Group (CGC), and BWX (BWX).

We hold none of them. Whilst we see potential merit in CTD’s strategy to build out a global corporate travel agent offering via roll-up, it is very difficult to determine whether they are adding value via this strategy or just buying cheap earnings. It has been a stellar stock market performer to date but as they say, “it’s not over until the corpulent soprano sings”.

CGC is interesting because it is a roll-up in just about the most perfectly competitive, commodity market there is – agriculture. They are doing it on a capital light model – wherever possible, leave the costly land in a REIT or with some other landlord. It has worked to date partially because their key commodities (such as avocadoes) have been going through a strong cycle.

However, it will be sorely tested when their key commodity prices turn down or yields fall due to climatic conditions because lease payments are fixed meaning the earnings impact could be severe. A PE of 26x is almost unheard of in agriculture and must also be prompting copycats thereby intensifying competitive bidding for assets.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

4 stocks mentioned

Avoca Investment Management

Avoca Investment Management

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

Expertise

Avoca Investment Management

Avoca Investment Management

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Investment Theme

When dumb money beats smart money, it’s time to worry

Livewire Markets