From Xero to Hero

Xero is by no means an up-and-comer in the fintech space, nor an undiscovered gem. At NZ$3.7bn market cap, the business already sits on the radar of many growth investors. While the business has enjoyed fairly spectacular early success, the inherent growth still available remains an attractive proposition to us.

Founded in 2006, Xero is now the leading cloud-based accounting software provider for small and medium sized businesses across Australia, the UK and New Zealand with over 1.03m active subscribers. Investors can sometimes baulk at a meaningful growth opportunity purely as a result of an already stellar amount of growth achieved. One should never be afraid of a larger market capitalisation if the size of the underlying opportunity remains suitably significant. When looking at the growth momentum currently underway at Xero as a point of reference, of the 1.03m active subscribers listed at the end of March 2017, 318,000 of these were only added in the last 12 months.

Leverage to a growing thematic

Xero provides investors an opportunity to gain exposure to the increasing adoption of cloud-based software. With the advent of multiple personal computing devices and the need for employees to access software programs remotely, cloud-based solutions provide businesses and their staff with the ability to access files, data and applications at any time from any device. With the added cost benefits of not requiring investment in hardware to run many of these applications, the uptake of cloud software continues to grow. A recently released report from the ABS Business Characteristics Survey reported just under a third (31%) of SME’s now use at least one paid cloud computing service, with the figure rising to as high as 60% for businesses employing in excess of 200 people.

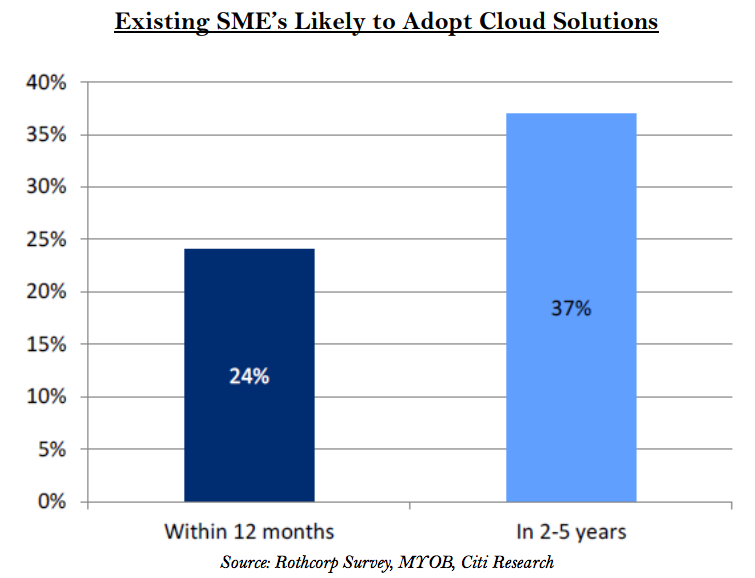

For users of accounting software in the SME space, the adoption figure is slightly lower with penetration of cloud products in the accounting space sitting somewhere around the ~20% mark. As more SME’s grow comfortable with cloud offerings in other areas of their business, it would be a reasonable expectation that this number begins to rise to at least a level in line with other software solutions. An industry survey conducted in December 2014 indicated 24% of existing SME’s were likely to adopt cloud accounting software in the next 12 months, while 37% indicated they would likely do so in the next 2-5 years.

Attracted to the growth in cloud-based software, and following positive feedback from a number of early adopters across both SME’s and their underlying accountants, we had been closely following the progress of Xero since about 2012. While we could see the underlying thematic remained highly attractive, we felt the valuation the market had placed on the business (using primarily a price/revenue based multiple) appeared excessive given the level of cash burn the company was still achieving and the likely requirement for a number of capital calls from investors to fund ongoing growth and R&D.

As a business that has never had a traditional desktop solution, the company has only ever been able to acquire customers via the conversion of existing incumbent desktop users that utilise a competing product (and/or in attracting new SME’s as they are established). The accounting software space as an industry is certainly attractive one with an oligopoly-type industry structure, high barriers to entry, strong pricing power and relatively high switching costs faced by underlying customers. Unfortunately, it is those attributes that make it exceedingly difficult for a new entrant such as Xero to penetrate the market in their first few years of growth.

As is often the case with first movers in disruptive business models, the company is forced to invest significantly in new platforms and technologies to ensure a best-in-class user experience, alongside the establishment of a fairly sizeable sales and marketing team to ensure critical market share gains. These investments obviously come at a significant cost and while the market was prepared to look through near term losses and attempt to value the size of the prize at the end of the journey, we felt the risk/reward equation at that stage still felt too longer-dated. As a result, whilst we were exceedingly impressed with the product offering (backed by countless glowing reviews from a number of large industry users of the product) and recognised the structural tailwinds building behind cloud adoption, we determined to continue to stay close to the business but not yet deploy capital until we could gain a better understanding around the path for the business to be self-funding.

Seeing the benefit now of previous investment in the business

Fast forward a couple of years and the business has now begun to materially benefit from its early investment in product development and sales, with net subscriber adds continuing to grow well in the core markets of Australia, the UK and New Zealand. On the back of higher gross margins and increasing cost efficiencies across all expense lines, the business is now poised to move into positive EBITDA and operating cashflow from FY18, with positive NPAT and free cashflow expected shortly thereafter.

Our portfolios will always maintain a strong preference toward businesses that are generating free cashflow and as a result we need to be very confident in a company’s ability to reach cashflow breakeven if we choose to deploy capital prior to the event. For Software-as-a-Service (SaaS) businesses like Xero, we can look toward the ‘Lifetime Value’ metric of the business to provide some comfort around future cashflows. Lifetime value is essentially the estimated aggregate gross margin that is contributed by the average customer over the life of the customer relationship.

In Xero’s case, the quantum of the Lifetime Value has continued to grow significantly – the Company estimated total group subscriber lifetime value at NZ$1.5bn at the end of FY16, which figure has now been more recently updated as closer to NZ$2.2bn. That is effectively NZ$700m of added value to the business in less than a year via adding more subscriptions, a lower churn rate of customers and some pleasing increase in gross margin.

With a growing subscriber base in which to spread incremental marketing and R&D costs, the business is now in a fantastic position for future growth and is generating extremely high incremental returns on capital. With revenue growing at 40%, NZ$113m cash on balance sheet and a clear line of sight to reach cashflow breakeven within the next 18 months (with existing cash reserves), we have subsequently initiated a position in the business.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

2 topics

1 stock mentioned

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management