FY 2020 – a year to forget, and a year to remember

Here are some insights into the 2020 financial year, how the insights have guided portfolio construction, and where the market is now.

Vladimir Lenin wrote that there are decades where nothing happens; and there are weeks where decades happen. Well, financial year 2020 in global markets featured three distinct periods. The first half of the year saw the momentum behind stocks offering high growth potential continue (in an ultra-low interest rate environment), highlighted by the strength in tech-related stocks such as Facebook, Apple, Amazon and Microsoft. I discussed in last year’s report that the valuations between them and the rest of the market were stretched. The elastic became even more taut in 2020.

The next period covering the months of December, January and February saw what I’d describe as the commencement of a rational market rotation into under-priced quality industrial and cyclical ‘value’ stocks. The significant discrepancy in valuations between growth and value began to reduce – albeit slowly. It seemed that our investment thesis was coming to the fore, assisting the performance of the stocks in our portfolio. Many growth stocks trod water with the market focused on the three ‘T’s of Tech, Trade, and Trump.

The final period saw the three ‘T’s pushed aside by the global COVID-19 pandemic. As we now all know, while principally causing the tragic deaths of hundreds of thousands, and illness of millions, around the world, the novel coronavirus has also affected every level of economic activity: from individual lock-downs; to the closure of state and international borders; to businesses having to either stop operations or move to work from home; to the ceasing of most international business and recreational travel. There has never been a pandemic that has resulted in such a rapid and globally synchronised economic shutdown.

Markets reacted accordingly, registering the fastest technical bear market in history as investors looked for the safety of bonds and bailed out of stocks deemed most leveraged to the global economy. This included some of the stocks held in our portfolio, particularly in financial services and building. Markets hit their low point on March 23 when peak fear was met by the peak fiscal and monetary response associated with governments’ ‘whatever it takes’ policies. At the time of writing, many market indices have returned to their highs, or are close to them.

At this juncture I would remind you of what I see as the key investment and market points stemming from the crisis markets:

- Short term, the market has followed a typical post-crisis path

Markets have followed a typical post-crisis path. All stocks are sold heavily, reach a low, then those stocks showing extraordinary growth or defensive positioning recover quickly. In this case, the technology stocks such as Amazon, Apple, Facebook and Microsoft were purported to show both of these positive attributes, retaining their growth potential, while also benefiting from investor fears that the rest of the ‘real’ economy will be impacted heavily by the COVID-19 shutdown.

On the surface, it can appear that there has been a disconnect between the performance of the markets, returning as they have close to or at record highs, versus the challenging macro environment. In certain cases that is correct, particularly in the areas of the market deemed as high growth, and, given their size within the major market indices, those indices have moved higher as well.

However, to say a “V”-shaped recovery has been priced in across the market breadth is incorrect. The most macro-sensitive stocks still remain well below their calendar 2020 highs. In our case this refers to US and European bank holdings. As at June 30, Bank of America was trading 33% lower than where it started 2020, and JP Morgan similarly down 34%. Commodity-based stocks such as Royal Dutch Shell have struggled to recover from the March lows and it is still down some 46% from the beginning of the year. On this basis, significant economic uncertainty is still being priced into markets, but it is being obscured by investors’ interest in the tech stock complex known more generally as FAANG+M.

- March 2020 was a rare investment opportunity

We believe that March was probably the bottom in the markets, with “peak fear” crossing over with a “peak response” from government authorities. This, I believe, created another one of those very rare investment opportunities, which tend to come around every 10 years. For example, we had the 1987 crash which left companies like Coca-Cola selling on a quite extraordinary price to earnings ratio (P/E) of 10. We had the TMT period around 1999, where the old economy was selling on single digit PEs. Then in 2009 we had the post-GFC environment, which produced, as I said at the time, a once in a lifetime opportunity in credit, and a once in a generation opportunity in equities.

And so we come to the COVID-19 period, where, 11 years after the GFC, I believe there was a once in a lifetime opportunity in those cyclical sectors of the market that were most impacted by the shutdown of many parts of the economy. This opportunity should not be discounted in terms of the quantum of gains we may be able to source. Post-1987, Coca-Cola traded sideways for about a year, but then proceeded to rise by 20 times over the next 30 years.

I am not saying that our quality industrial and cyclical stocks, either ones that we have held for some time or our more recent purchases, will rise by that amount, but just to point out that: a. gains can be significant; and b. the market actually gives you an opportunity after these big downturns to buy what can be very discounted valuations. The same was true with BHP in the post-TMT period, and the global franchises like Visa in the post-GFC period. Now, we are again at what I believe to be a major secular shift in the performance of different types of businesses in the market and which ones will generate an appropriate return for investors over the next decade. For example, commodity stocks are close to an all-time relative valuation low compared to the rest of the market.

Copper and gold miner Freeport-McMoRan is an illustration of a stock in this sector that is showing a wide valuation disparity with the market. It has one of the highest quality, low cost, long life, copper and gold ore bodies in the world. However, at the trough price of March the company was selling at approximately an 18% free cashflow yield based on the then distressed copper price of $2.30. Freeport has recovered but at the time of writing was on a 12.7% free cashflow yield assuming the current copper price of $2.90. Compare that to bonds yielding close to 0%.

- Valuation, not macro, is the issue and always is

It is easy at these times of crisis to concentrate on macro issues. When will we come out of the pandemic? When will a vaccine become available? When will global borders re-open to the same extent that they were? When will job markets normalise? Such questions, although valid, to my mind are very difficult to accurately forecast. Instead, we are concentrating as we have always done – on individual valuations and their validity in a long term context.

Referring again to Freeport-McMoRan, if an investor is receiving a 9% free cashflow yield in an environment where investors were pricing in an economic shut-down, then we are getting paid to wait. If the macro environment does improve, and copper goes to $3.50-$4, then on the current valuation it is trading at a very attractive 40% free cashflow yield. So in this context the macro situation is more a distraction, creating the opportunity to buy businesses at such reasonable levels.

Our portfolio

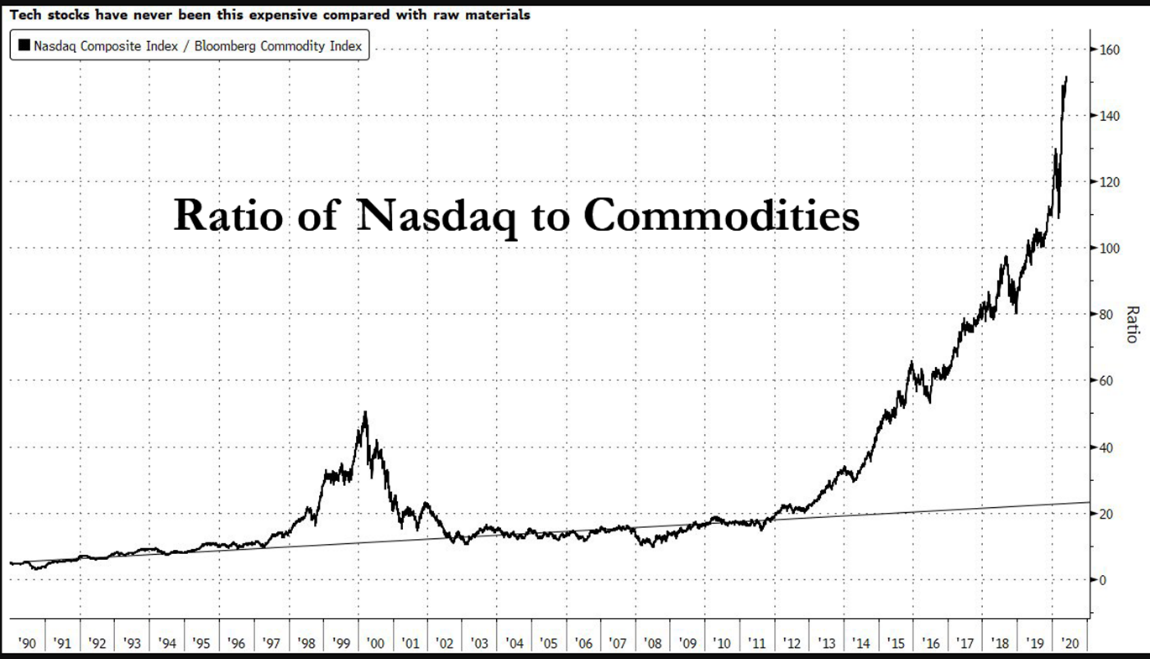

Portfolio construction has been centred on two factors. Firstly, the record low valuation in the more cyclical/ industrial sectors of the market versus growth stocks. For example, the ratio of tech stocks to commodity prices is now far higher than at the time of the Global Financial Crisis, and versus the rest of the market commodity companies are trading in the bottom quartile of valuations – a rarely seen event.

The other key point that is framing our long term investment is our belief that not only are we at the end of the bull market in interest rates, but we are at the turning point in inflation. About 40 years ago when we had double digit inflation, it would have been ill-advised to suggest that one day we will have negative interest rates. However, government action and economic events have made that a reality.

We are now in a position where monetary authorities are pledging to kill deflation, while government fiscal policies are running significant debt-funded stimulus around the world as they attempt to shore up economic activity. Inflation is unlikely to appear in the immediate future, but to me we are at the start of the turning point which precipitates the re-emergence of inflation.

In terms of portfolio activity, prior to COVID-19 we had reduced our net invested position to 81% as some of our investments were starting to sell at the lower end of our exit price range. With the sudden decline in markets we have increased our invested position to approximately 90%.

The largest movement in the portfolio has been in the expansion of positions in the materials sector, including Freeport-McMoRan (copper), Newmont Mining (gold), Teck Resources (copper and zinc) and Boliden (zinc). We also increased our positions in quality industrial stocks like Siemens and re-established a position in Alphabet (Google) a globally dominant franchise.

We used the weakness in the Australian Dollar in early 2020 to increase our exposure here, giving us some protection from the appreciation of the AUD in the fourth quarter of FY2020.

In conclusion

What is clear to me is that when you look at valuation metrics at the end of March, it would appear to have been a once in a lifetime opportunity in quality cyclical and industrial stocks with the upside return possibility equal to or greater than what I saw post-GFC with the market in general.

We feel the pandemic has not simply delayed our thesis, but the fiscal and monetary actions will have the effect of essentially making the thesis inevitable. The unknown factor is the timing. In the short term, behavioural biases have not declined and their effects will be exaggerated by the weight of the index funds. This is why it is so important to have a longer time horizon so as to let the thesis play out to its full extent and in doing so profit from it. It’s amazing how often - if one has patience - the conventional “wisdom” proves itself to be wrong.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I'm PM Capital’s founder, CIO, first investor in our Global Companies Fund and its portfolio manager since its inception in 1998. Across all of our funds we invest independently, with integrity and in the best interests of of our co-investors.

........

The content reflects opinions as at the time of writing and may change. PM Capital may now or in the future deal in any security mentioned. It is not investment advice.

3 topics

I'm PM Capital’s founder, CIO, first investor in our Global Companies Fund and its portfolio manager since its inception in 1998. Across all of our funds we invest independently, with integrity and in the best interests of of our co-investors.

I'm PM Capital’s founder, CIO, first investor in our Global Companies Fund and its portfolio manager since its inception in 1998. Across all of our funds we invest independently, with integrity and in the best interests of of our co-investors.

Comments

Comments

Sign In or Join Free to comment