George Constanza and the art of doing the opposite

I know I’m not alone in saying that watching old episodes of Seinfeld is one of my favourite ways to unwind – I’ve even done the Kramer Reality Bus Tour in New York! Yet it came as a bit of a surprise when the episode ‘The Opposite’, where George Costanza finds great success by ‘completely ignoring every urge towards common sense and good judgement’ and doing the exact opposite, reminded me of my own approach to investing in shares.

Don’t get me wrong, I’m certainly not suggesting that Australian equity investors ignore their good judgement when making investment decisions! Rather, the episode stood out because it conveyed a message that going against conventional wisdom and instinct can potentially lead to better long-term outcomes. I argue that this mindset is critical for successful equity income investing over the long term. In an investing context, conventional wisdom and investor perceptions are often expressed through rules of thumb and other simplifications.

The trouble with rules of thumb for equity income investors

For equity income investors, the problem with these rules of thumb and related simplifications is that they often result in satisfying only one objective (eg. short-term income needs), while ignoring other objectives and, potentially, introducing additional unintended issues. When concepts are simplified, the basic assumptions upon which they are based are often ignored and the concepts are applied more broadly than they were originally intended. The end result can be an investment strategy that appears to address desired outcomes over shorter timeframes, without addressing some or all of the originally intended long-term objectives.

Notable commentators (more qualified than George!) have encouraged investors to go against conventional wisdom and do the opposite in the past. Warren Buffett famously said “be fearful when others are greedy and greedy only when others are fearful”. When it comes to equity income, doing the opposite is more important than just adopting a contrarian investment style. It’s about reflecting on all aspects of your investment philosophy and approach to ensure that all objectives are achievable over the long term.

Over the coming months, I will share thoughts on the emphasis that many investors place on high franked dividend yield stocks as part of an equity income strategy. Generating a sustainable income stream from investments is a particularly important consideration as investors move into retirement. At this stage of an investor’s lifecycle, investment income is typically being used to fund retirement, potentially over several decades. This makes income an important long-term concept.

Yield and income – same same, but different

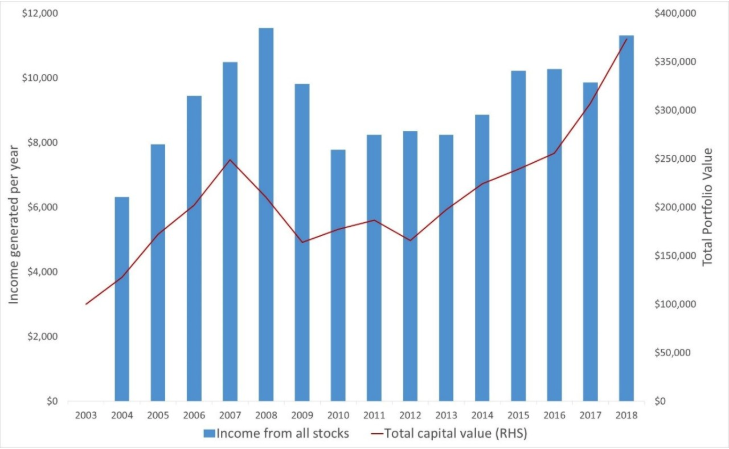

In recent years, expected returns and income from traditional income asset classes have been low following years of global yield compression. As a result, investors have increasingly looked towards growth assets, like equities, to meet their income requirements. The status quo response has been to target an equities mix that tilts towards higher yielding investments to match the desired portfolio yield target. This simple approach is often adopted because the terms yield and income are habitually used interchangeably when describing investment strategies. And yet there are important differences! I often discuss this chart with clients, which shows the value of dividend and franking credit income generated each year from a simple buy and hold strategy.

The case for using equities for income is sound: Annual dividend (and franking) income generated

Source: Colonial First State Global Asset Management, FactSet. Income and capital over 15 years calculated assuming a total investment of $100,000 equally weighted across all index constituents of the S&P/ASX 100 index as at 30 June 2003 that have the required 15 year price and dividend history (57 stocks). Data to 30 June 2018.

To help explain the important differences between yield and income, let’s consider a hypothetical strategy that invested $100,000 equally in each stock in the S&P/ASX 100 index in June 2003. Of these original 100, just 57 are still listed – these stocks therefore form the sample for our analysis. The remaining 43 ASX 100 constituents from 2003 have been delisted for various reasons since then – these stocks are excluded from the analysis as a full 15-year price and dividend history is unavailable.

The blue bars show that the $100,000 investment generated income of more than $6,000 in the first year alone and that dividends continued to provide a resilient source of income over the 15-year period. It’s understandable that investors are attracted to the apparent stable growth income characteristics of Australian shares.

Share price performance matters just as much as yield

While it’s true that Australian shares have provided appealing income streams, investors often extrapolate this and conclude they can increase the amount of income generated each year by limiting their investments to stocks that pay high dividend yields. But is this simple approach likely to deliver the desired outcome? Targeting higher income from equities by tilting a portfolio towards stocks with higher yields changes the underlying portfolio holdings. In turn, it’s important to consider how the share price performance of this different portfolio impacts income generation. There’s an additional need to understand the role that capital growth plays in generating an attractive income stream from shares over time.

It may seem counterintuitive, but equity investors aiming to maximise their dollar income return over the long term must maintain a focus on the growth returns of the equity market. Let’s see this in action in the chart below.

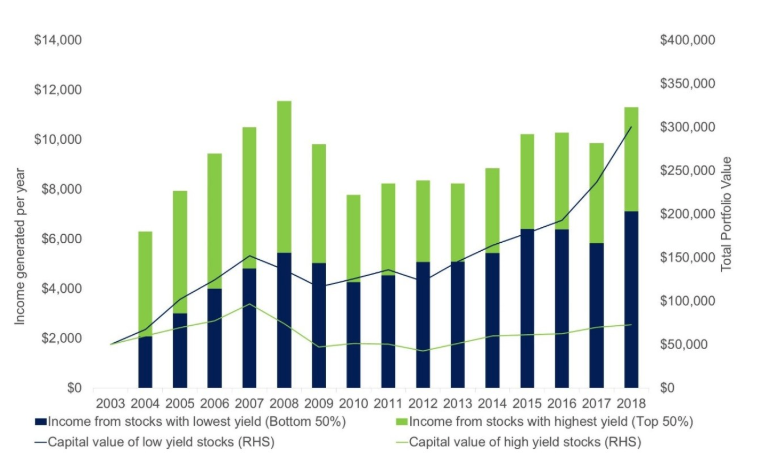

A focus on high yield alone does not necessarily generate higher long-term dollar income

Source: Colonial First State Global Asset Management, FactSet. Income and capital over 15 years calculated assuming a total investment of $100,000 equally weighted across all index constituents of the S&P/ASX 100 index as at 30 June 2003 that have the required 15 year price and dividend history (57 stocks). Data to 30 June 2018.

In this chart, I have split the attractive long-term income stream generated from the Australian shares into two groups, depending on their grossed-up dividend yield at the start of the period. The green bars show the dollar income generated from stocks with the highest yields (top 50% of stocks) and the blue bars show the dollar income generated from stocks with the lowest yields (bottom 50% of stocks). Investors that targeted above-average yield stocks would actually have been worse off from a dollar income received perspective over the long term, even after accounting for the benefit of franking credits. Those with a keen eye might have observed that the high yield cohort produced higher levels of income in the first few years of the investment. That’s true, and it’s understandable that some investors prioritise this given the immediacy of their income needs. But the investment challenge for most investors is longer term in nature, including the generation of income over potentially long time periods in retirement. I’ll explain a way to balance the need for near-term income whilst remaining focused on generating attractive long-term dollar income later in this series of papers.

Aim higher than high dividend yield alone

I’m not advocating an approach of only investing in low yield stocks for income. Rather, the key takeaway from the two charts is that higher dividend yields alone do not necessarily ensure that higher levels of dollar income will be generated over the long term.

What has produced this counterintuitive outcome? As we have seen in the chart, the lower yielding cohort collectively rewarded shareholders with a much higher level of capital growth. The lower yielding stocks’ delivery of greater long-term dividend income was not attributable to their dividend policy or yield, but rather their significantly higher total return, comprised of both dividend income and capital growth. Importantly, when it comes to income generation from shares, each year’s capital return provides the base upon which the following year’s income return is generated. This is the key to long-term dividend income growth. In short, strong total returns will drive attractive income from equities over time. Maximising income and after-tax total returns from equities over the long term requires investors to consider yield and growth together, rather than focusing on yield alone.

Does the above analysis imply that the dividend yield concept is flawed? Certainly not. The concern is that investors instinctively apply yield valuation metrics as a proxy for future cash flow generation.

One of the side effects of being an Australian equities fund manager is that nearly every aspect of life can play a role in identifying attractive investment ideas and themes. I unashamedly admit to being interested in TV adverts as a guide towards current consumer trends or the number of cranes on the city skyline as an indicator of construction activity. But I never thought an episode of Seinfeld could be so enlightening!

Want more insights on Australian income?

A series of regular news updates, research papers, investment strategy updates and thought pieces from some of Colonial First State Global Asset Management's leading experts can be found here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Rudi is Head of the Equity Income and Target Return Income Funds, and is responsible for investment strategy, stock selection, portfolio construction, investment process enhancement and management of the Equity Income investment team

2 topics

1 contributor mentioned

Rudi is Head of the Equity Income and Target Return Income Funds, and is responsible for investment strategy, stock selection, portfolio construction, investment process enhancement and management of the Equity Income investment team

Expertise

Rudi is Head of the Equity Income and Target Return Income Funds, and is responsible for investment strategy, stock selection, portfolio construction, investment process enhancement and management of the Equity Income investment team

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

Ross vs the AI hype: her shocking prediction revisited

Livewire Markets