Removing barriers to your performance

Brett Gillespie

Global Macro

It’s the time of year we typically take stock – both personally and professionally. And if you are reading this, presumably financially as well. And we make our New Year resolutions! Of course, we joke about NY resolutions, because so many of us fail to keep them. So why make them? Indeed my wife refuses too – she advises it is the most unsuccessful time of year to make a resolution!

But being the start of a New Year, I thought I might touch on some of my own experiences with resolutions/goals. If you prefer just a view on the market, skip to the outlook section below.

If you haven’t skipped, I wonder have you watched “Billions”? (1) I must say I thoroughly enjoyed the show, though it does do a dis-service to the hedge fund industry. It would be easy to assume from watching the show that hedge funds only made money through illegal activities.

I’ve traded for macro hedge funds for over 15 years now. And I can tell you that no investment professionals work harder or are more committed to excellence and performance than my colleagues in this space. (2)

But that is not why I mention it. If you have watched the show you were likely intrigued by the traders visiting the “performance coach”. Played by Maggie Siff, “Wendy Rhodes” is the firm’s in-house psychiatrist. Traders in a rut would visit her and get “coached”. When people ask me about “Billions”, and are hedge funds really like this, they often raise Wendy Rhodes as one of the most intriguing aspects of the show.

I too have a coach. In fact for a while I had two coaches! One in Sydney and one in Connecticut. My Connecticut coach focussed on “business issues” – trading discipline, staff, management etc. My Sydney coach was more focussed on mental issues – what was holding you back from being your best? I benefitted immensely from both of them.

Which brings me back to NY resolutions. And goals. When I reflect on my coaching sessions, we actually don’t spend an awful lot of time on the goals. Because the goals are obvious. Generate the best performance you can for your clients. And live a happy and fulfilled life. (Of course they are not one in the same.)

Where we spend the time is on how to do that. On the business side – the focus is on process and repetition.

What are you doing well, what can you do better, what should you consider doing that you haven’t thought of. What can you do to get the best from your staff and keep them motivated?

Plenty to talk about, plenty to monitor, plenty to score progress on. A good coach will guide you through these questions and offer suggestions you have not thought of. And the answers are typically steps you need to take, habits you need to form, not goals per se. (3)

On the mental side, it is more akin to the psychology of an athlete. To take a trade, a position, particularly a large one, you are saying you know better than the rest of the world. You have to be confident in your process. And like any partaking that requires confidence, be it investing, sport or even surgery, once you start doubting yourself you make mistakes – or in sporting parlance you have a “slump”. So a mental coach focuses on this. What is holding you back from being your best? What steps can you take to address that? This is often very different to goal setting. It’s about identifying what is undermining your confidence, or holding you back from performing at your best.

Let me give you a personal example. Around the end of 2006 I was having an inevitable drawdown (losing money for my fund). And I was getting worried and stressed. My coach said, “Well, if you don’t perform what’s the worst that can happen?” “Well”, I said, “if I don’t perform for another year I will likely lose my job. There are no similar jobs in Sydney. So that could be two years without a bonus, then no job, so I would probably have to sell the family home. That would create so much stress that I would likely end up divorced, living in a small unit in Surrey Hills on my own!”

He said “Would that be so bad?”

I replied “Well, I think so…”

“So why won’t you get another job?”

I explained the specialised nature of my work, and that the same job (at the time) did not exist in Sydney. He said “What about something similar? Have you looked? Why don’t you go looking for a job?”

It seemed extreme to me. After all, the last thing I wanted to do was leave my fund! But I followed his advice, and within 3 months had two good job offers. Not the same, but good none the less. I had a Plan B…

My coach explained how I was catastrophizing. By making me physically seek out a job offer, my catastrophic scenario, my fear, suddenly evaporated. In the next 3 years I posted one of the best performances at my firm. Indeed, I was asked to present at the annual conference and talk about what contributed to my performance, and I relayed this story – of a coach paid for by the firm telling me to look for a job elsewhere!

Now this improvement didn’t result from a goal. It resulted from removing a barrier to my success. And the focus was on the steps required to remove that barrier. So when you consider your New Year resolutions, do you need goals or do you need to remove barriers. Then ask yourself what steps do you need to take?

Now for financial goals. Again, the goal does not need to be discussed much. Quite simply it is to achieve the best risk adjusted return you can, commensurate with your risk tolerance and investment horizon. It’s the steps that matter.

So as we look into 2018, what steps should you be taking with your finances? Will that much forecast bond sell-off emerge this year? Should you be moving defensive after such a stellar year for equities?

The Outlook

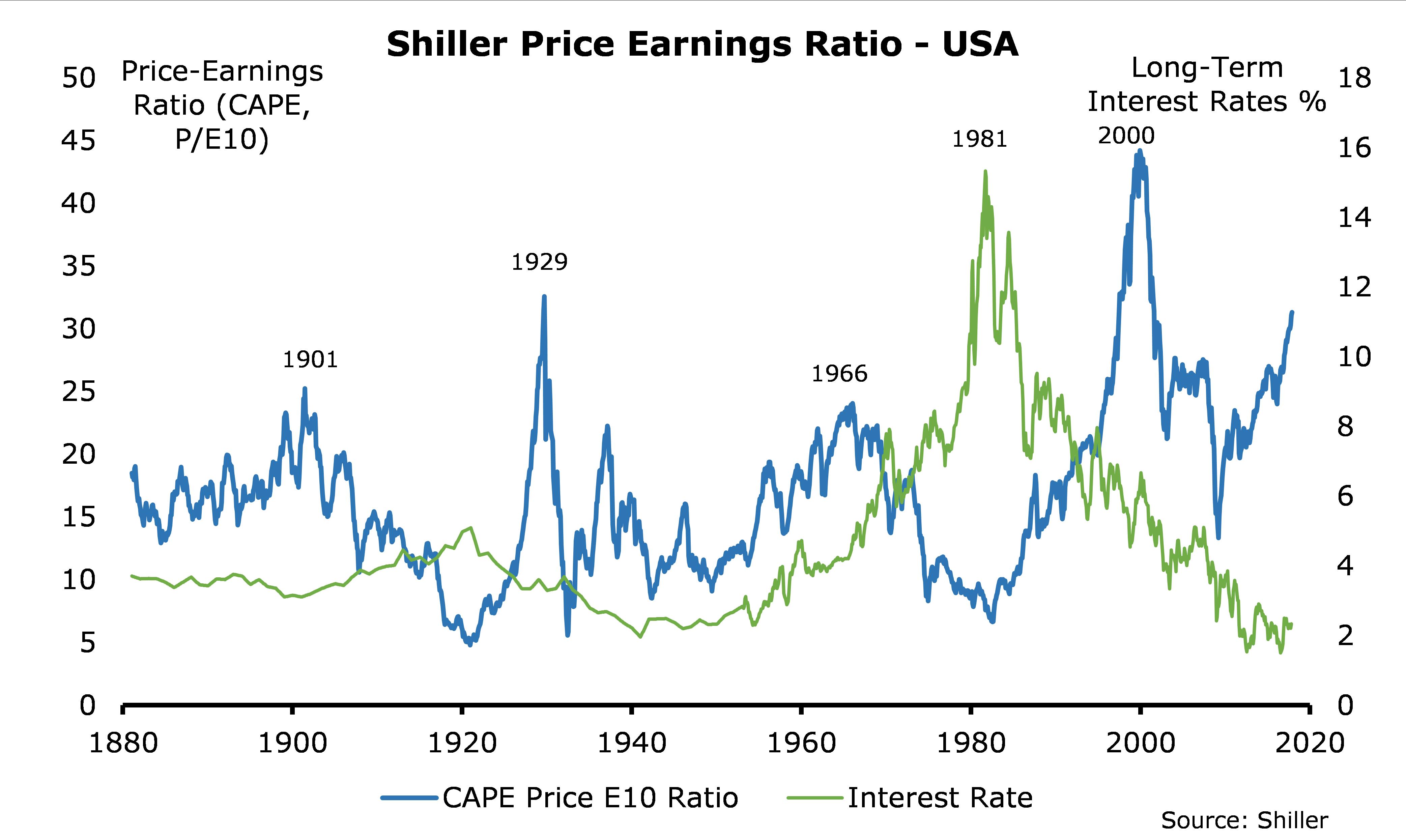

By most measures, US equities are overvalued. Supported by bond yields that are suppressed by global quantitative easing, the cyclically adjusted price earnings ratio (CAPE) is about the second highest it has been in the last century.

Our forecast is for bond yields to rise driven by two distinct factors

- Core inflation rising to 2% (4) in the next 3-6 months (worth 40-50 basis points)

- Suppressed risk premiums (5) rising about 90 basis points over the next 12-18 months.

If we are right, this size bond market move would warrant a 10-15% correction in equities.

Of course, a lot of people thought this at the start of 2017 as well. And a defensive position turned out to be exactly the wrong decision for 2017.

So will 2018 be different? We think so. But better still, we think 2018 will be very interesting. And by interesting I mean opportunities. In particular in global interest rates.

You see, there are two key questions when it comes to generating macro returns from interest rates. What are bond rates going to do (the more important rate for equity markets). And what are cash rates – set by the central banks – going to do? 2018 is going to be a very active year for global central banks.

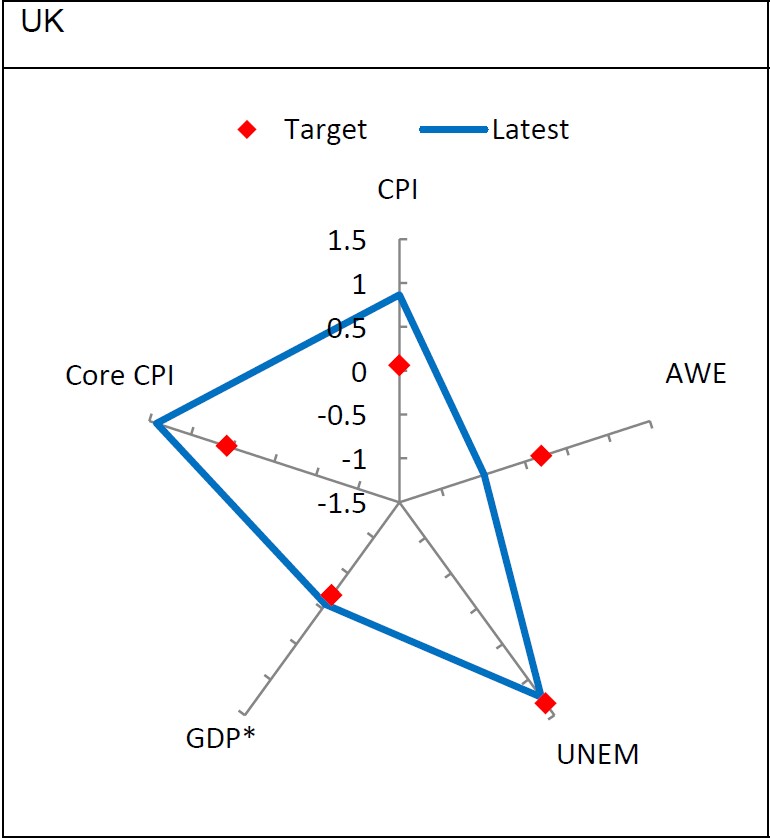

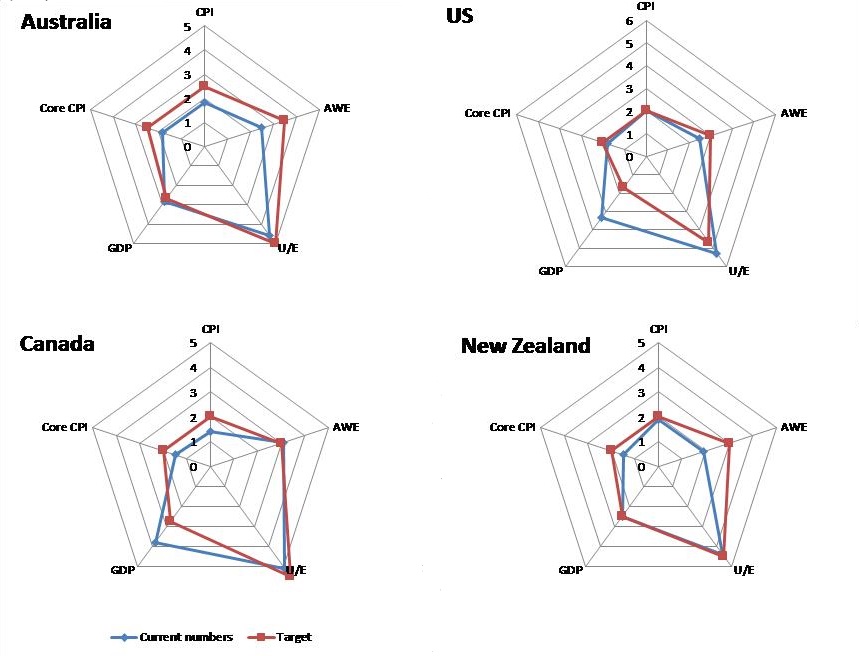

How can I be so sure? Because the world has healed. Kristin Forbes(6) demonstrated this eloquently in her parting speech from the Bank of England (BOE) Board last June with the following diagram;

The indicators listed are the key indicators that feed into a decision to change rates. The red dot is the target for the BOE. The blue line shows where they were relative to target. The blue line “outside” the red dot would warrant a cash rate higher than “normal”, or neutral. She was highlighting that every measure but AWE (average weekly earnings) was performing better than/at their target – yet they still had an emergency setting for rates.

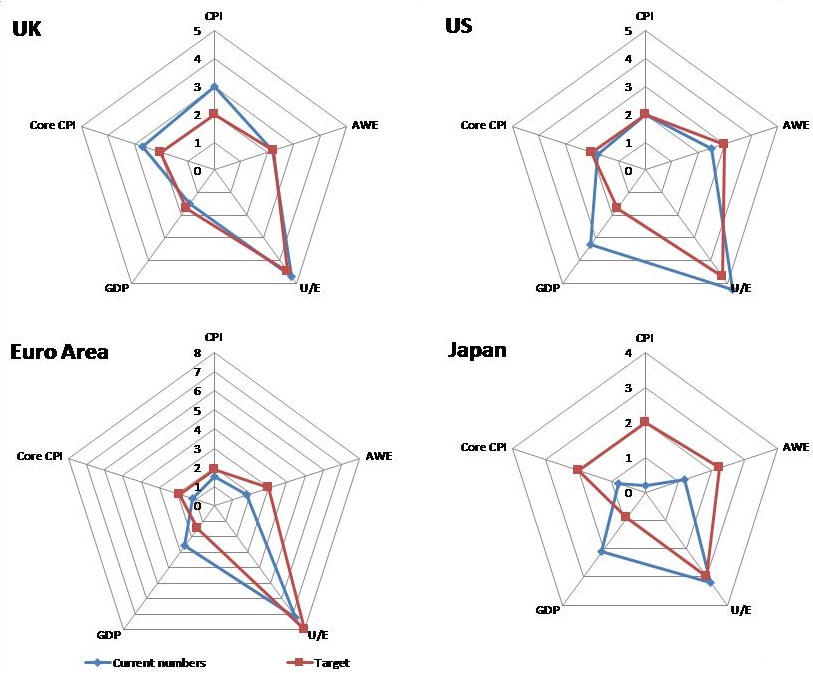

Our economist Tim Toohey has recreated a similar analysis for all the countries we look at. Here is a sample. Again if the blue line is “outside” the red line, it means the indictor is stronger/higher than the central bank’s target. It would indicate they should be targeting a neutral cash rate, perhaps even restrictive.

We can clearly see why the US, Canada and the UK hiked this year. And we can see that Australia and NZ are very close to the conditions that warrant a hike.

This diagrams tell us how healthy the economy is. But there is another big factor for central banks in setting policy. It is what Glenn Stevens once described as the policy of least regret. (7) Over the last decade, central banks globally have erred on the side of easier policy. When they weighed the risks of falling back into recession, versus the risk of an uncontrolled pickup in inflation, they concluded their policy of least regret would be to over-stimulate their economies.

2017 marked a shift in the policy of least regret for the US, Canada and the UK.

There are now two larger risks on the central banks minds;

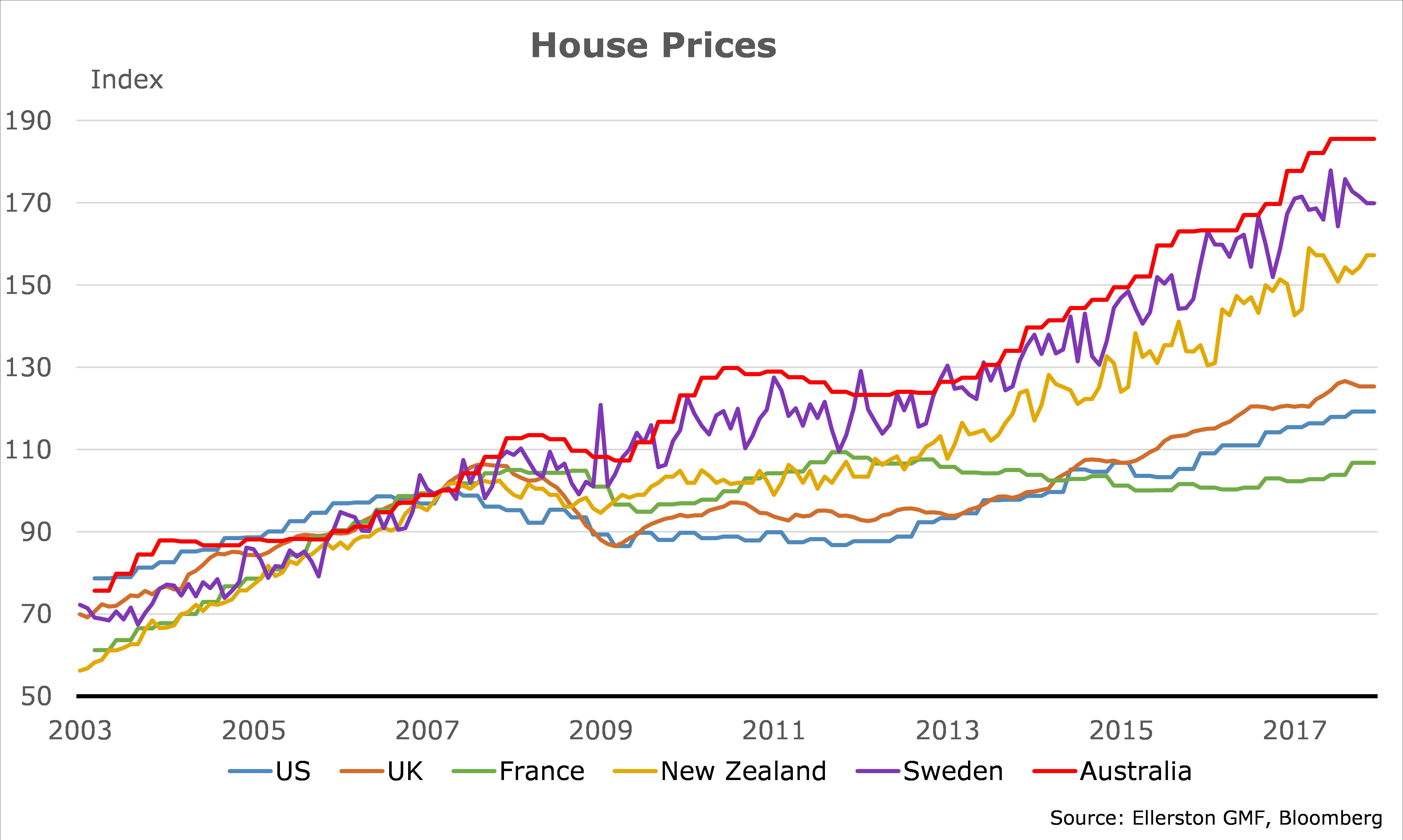

- The boom in assets prices. Housing markets across the world have fully recovered, and in many cases are well above pre-GFC levels. (Australia 85% higher than 2007!) Now concerns are turning to financial stability. Are they sowing the seeds for another housing market crash? The world has clearly healed now (based on the diagrams above). And what’s more, it is healing very quickly. The policy of least regret is quickly turning to leaning against the housing boom.

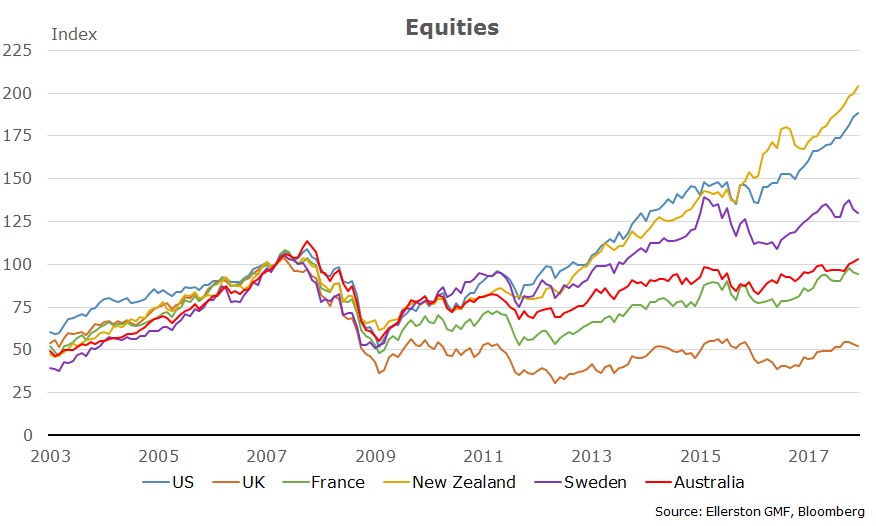

And the equity boom… Not many would realise the US S&P 500 is up over 100% from its pre-crisis level. (And 265% from its 2009 low). The December Fed minutes show some Governors are getting a little concerned with the recent acceleration in US stocks. (8)

- The other risk? Wages. With historically low unemployment rates in the US and UK, will wages suddenly rise? History and indeed surveys suggest so. And once wages have started to rise, they have tended to rise very quickly. That’s why in the past 30 years, central banks have moved the cash rates back to normal (neutral) levels well before wages started to rise. In most countries today, that would require a 1.5-2% rise in cash rates. If wages were to start rising quickly now it would be a year or two before the Fed could achieve a high enough cash rates to quell them. And then they would have to be so aggressive that would cause a recession. Not what you want…

So as economies approach a position of rather rude health, we find central banks fears are shifting. “What’s the worst that can happen?” they ask themselves. A year or two ago it was a premature hiking of interest rates that snuffed out the recovery. Now it is a potential bubble/bust in asset prices driven by low interest rates, and/or the risk of a bond market crash/recession if wages start to rise quickly. They are now looking forward, not backwards, and it is just a little scary. When it comes to the policy of least regret, 2017 marked a sea change.

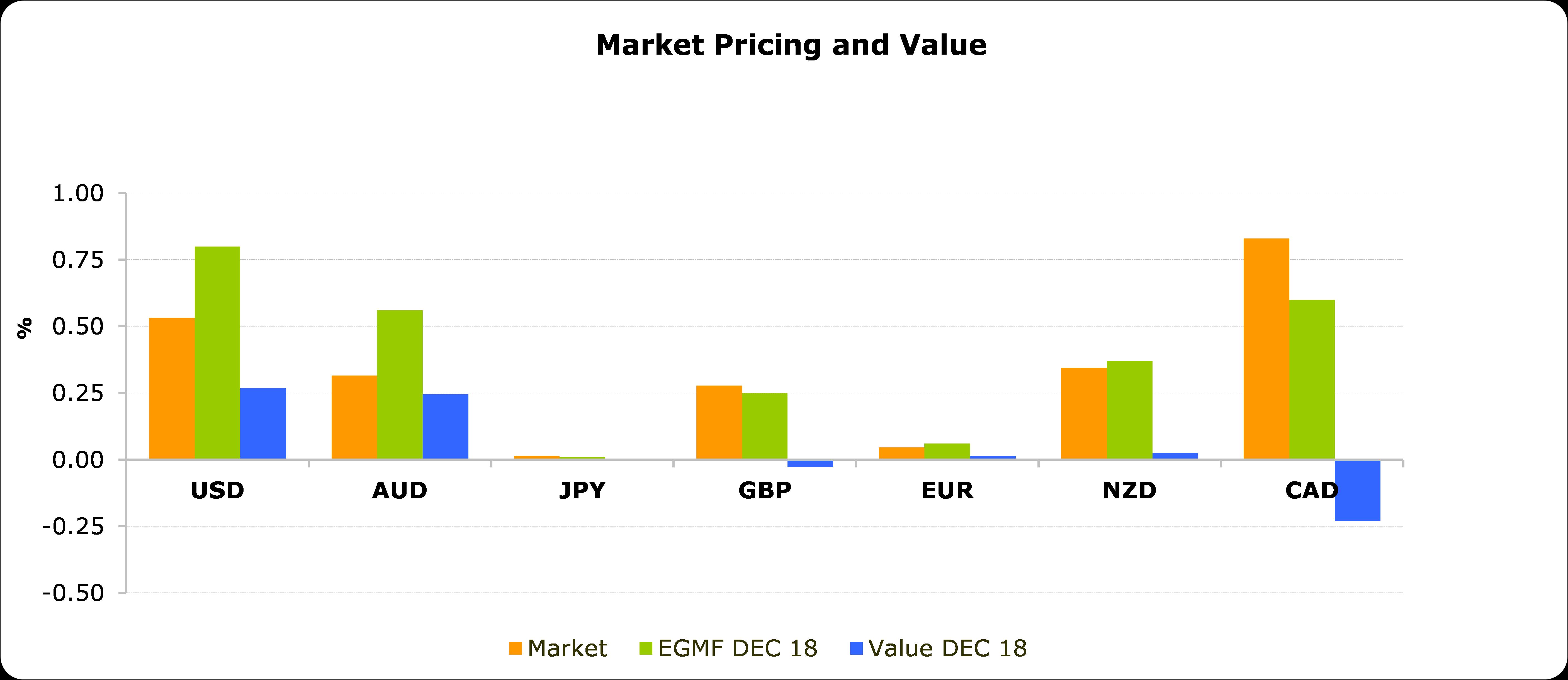

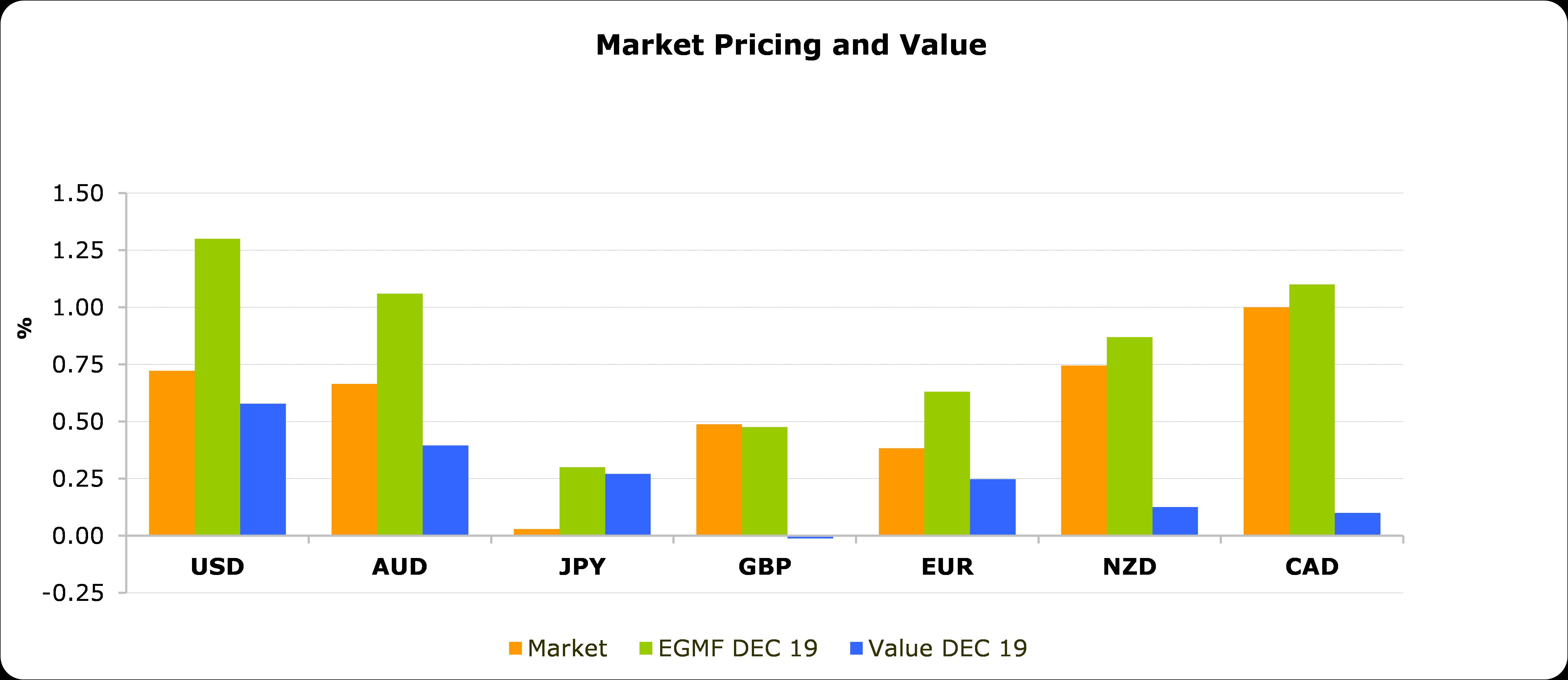

So as we enter 2018, the policy of least regret will continue to argue, if not scream, for rate hikes. This is our most confident call. The orange bars in the chart below shows what the futures market currently prices for rate hikes in 2018. The market, as do we, expect many active central banks. Our forecast is in green. In 2018, we expect 3-4 hikes from the US and 2-3 hikes from Canada, 2 hikes from Australia and 1-2 from NZ, and a hike in the UK. (9)

The futures market will likely price two hikes in Europe through to the end of 2019. And a hike in Japan.

Will equity markets cope? I do a bit of Fermi-ising here (10). Conservatively, I would assign 65% confidence to our inflation call in the US, and 60% confidence to our risk premium call. Smart people can reasonably disagree on the outlook for a sharp acceleration in wages in the US, but assigning a 25% chance is not too controversial. And let’s say a 10% chance that growth just inexplicable weakens. When I construct a probability tree I get a;

- 80% chance the Fed hikes more than expected.

- 70% chance that US bond yields rise more than 0.5%.

- 50% chance US equities have a correction of more than 10% during the year. (11)

We see the best opportunity in pursuing a) – more hikes than expected from the central banks.

In particular, we are positioned in the US, Australia, New Zealand and Europe for higher cash rates being priced in the futures markets in 2018 and 2019. We have typically constructed 3 or 4:1 risk reward trades for something we see as a 70-80% chance. That’s exciting.

And we are also exposed to b) of course! A steeper yield curve. In options though to limit the downside.

Good luck in 2018 with your personal and professional goals (steps). And hopefully you are at least thinking about what financial steps you are taking to navigate 2018 safely.

For further insights from Ellerston Global Macro, please visit our website

Footnotes

- a TV series on Stan about running a large corrupt hedge fund in Connecticut

- I also managed real money for 5 years and proprietary bank capital for 8, so I have some perspective

- "Outliers: The story of success” by Malcolm Gladwell outlines how “greatness” requires enormous time – the so-called 10,000 hour rule. A good coach will ensure your 10,000 hours is well directed.

- (VIEW LINK)

- (VIEW LINK)

- (VIEW LINK)

- (VIEW LINK)

- Both charts are normalized to 31st March 2007.

- This is our central expectation. As the data evolves so will our forecast. The potential range is large given the risk of anything from asset bubbles bursting through to a wages break-out in the US. Volatility has the potential to pick up significantly

- (VIEW LINK)

- All rounded to nearest decile

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

1 topic

Brett Gillespie

Investor

Global Macro

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

Expertise

Brett Gillespie

Investor

Global Macro

Brett has worked in the financial services industry for over 28 years. Most recently he was Head of Global Macro at Ellerston Capital. Prior to that he spent over 10 years as Senior Portfolio Manager at Tudor Investment Corporation.

Expertise

Comments

Comments

Sign In or Join Free to comment