Hard to fault Westpac's result

Today marked the conclusion of the May profit reporting season, with Westpac finishing the season well with a strong result that was well-received by the market. May has been a kinder month for shareholders in the major Australian banks than March and April, with three of the four major banks releasing their profit results for the past six months.

What we have seen over the past seven days has mostly been a well-executed exercise by the bank CEOs in addressing the concerns of nervous investors and demonstrating that their underlying businesses are performing well and are still very profitable.

Hard to find much to fault

After looking through hundreds of pages of bank results over the past week, Westpac’s result appears to be the strongest and it was hard to find much to fault.

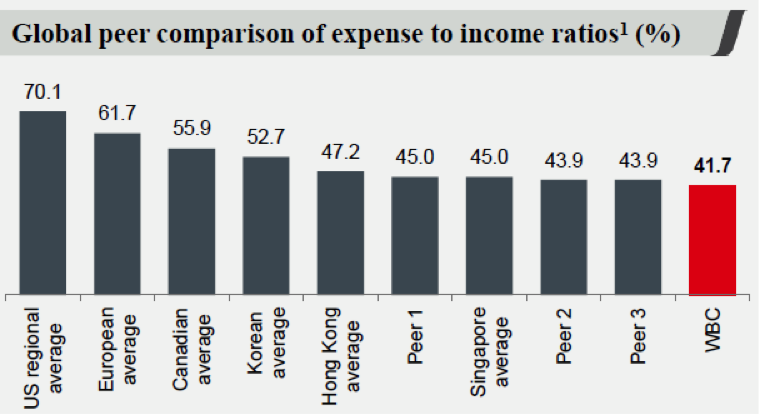

Profits were up 6% to $4.25 billion, return on equity (ROE) solid at 14% and cost to income ratio declined to 41.7%.

Westpac expects their costs to serve customers to decline as the bank’s customers shift to digital and self-serve channels rather than going into a branch.

Whilst the Australian banks may create the impression as being staid and bureaucratic, they are actually amongst the most efficient banks in the world.

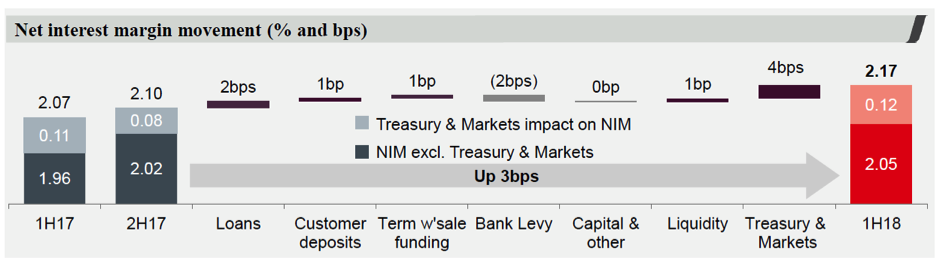

Another highlight of the Westpac was the increase in the bank’s Net interest margin to 2.17% from higher deposit and loan spreads. Looking at the below table, Westpac has seen the benefit from both repricing existing loans higher and in declining costs from term deposits and wholesale funding. These actions have more than offset the impact of last year’s bank levy.

Loan book looks fine

During the Royal Commission, Westpac was required to present a portfolio of 420 loans to be analysed by accounting firm PWC. Based on this very small sample size, two weeks ago Westpac was downgraded by a prominent investment bank, based on concerns about lending standards and poor credit quality.

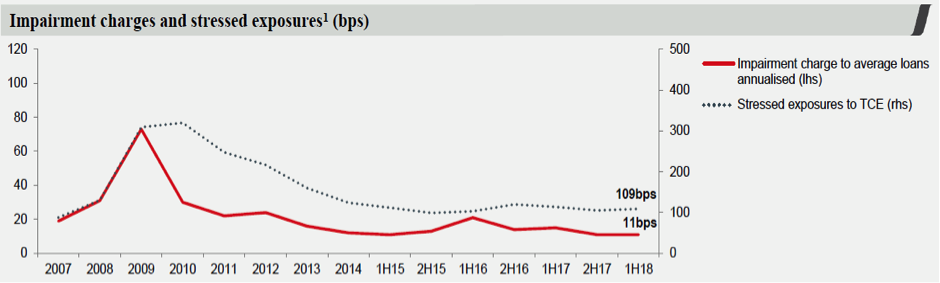

This saw Westpac’s share price fall by almost 5% on fears that the bank would report higher bad debts. However, this morning Westpac reported a very low bad debt expense of 0.11% across their entire loan book of $701 billion. This result shows the danger of extrapolating a small sample across a large loan book.

The below table shows the massive earnings tailwind that Westpac (like all banks) have enjoyed over the past 10 years as bad debt charges have consistently trended lower to the historic lows we are currently seeing.

What will the main impact of the Royal Commission be?

In comparison to the other major financial institutions, Westpac has faced a higher level of scrutiny than ANZ Bank, but less than CBA, NAB and Commonwealth Bank.

Where the Royal Commission will impact Westpac is in tightening the bank’s lending controls, which is likely to slow down credit growth and increase the costs and time taken to originate a loan.

Given where we are in the property cycle, we would not be unhappy to see Westpac lose market share to non-bank lenders for riskier lending.

The non-bank sector refers to lenders that are not allowed to take deposits from the public but can make loans by sourcing funds from the wholesale capital markets. Non-bank lending has grown rapidly over the last year in response to APRA limiting lending on investor and interest-only loans by the major banks.

Happy holders

This was a good result from Westpac, showing the resilience of the bank’s consumer and business bank divisions. Westpac is a core bank position in the Maxim Atlas Core Equity Portfolio and see that it trades on an undemanding valuation with a PE of 11.6x with a fully franked yield of 7%.

Read our coverage of other bank results

ANZ: Solid result despite Royal Commission

Key takeouts from NAB's result

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

3 stocks mentioned

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why my mum might help pop the CBA bubble

Elston Asset Management

Equities

Is the end of globalisation the end of global equity investing? The follow up...

Arteqin Capital Limited