House Prices to Fall in 2018

In the AFR today I outline my views on markets for 2018, including forecasting that Aussie house prices will fall year-on-year for the first time since 2012---after we projected house price increases every year between 2013 and 2017---and that US inflation will surge (in fact, US inflation has already spiked according to an important new index released by the New York Federal Reserve). Click on that link to read for free or AFR subs can use the direct link here. Excerpt below:

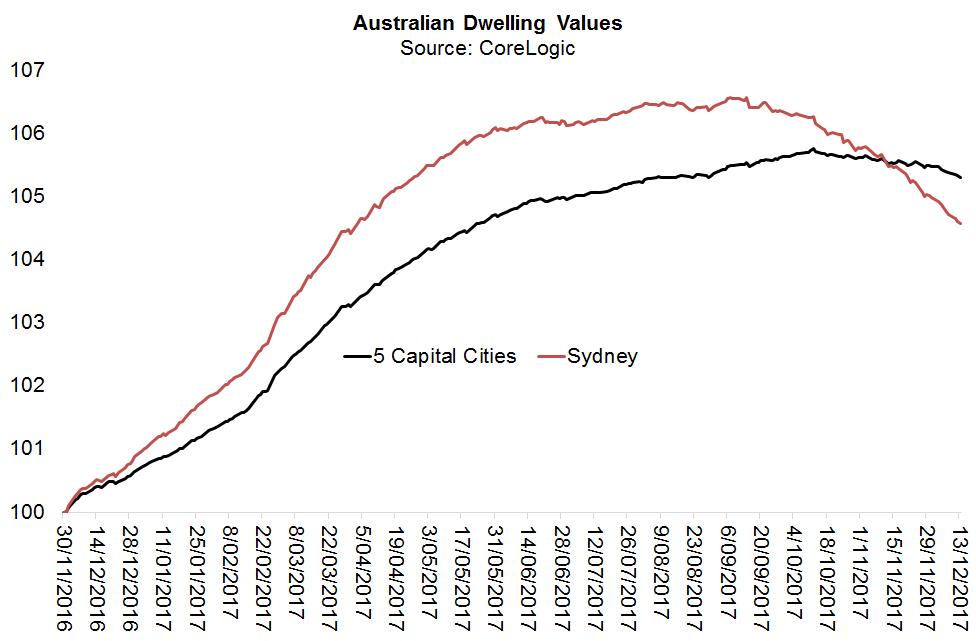

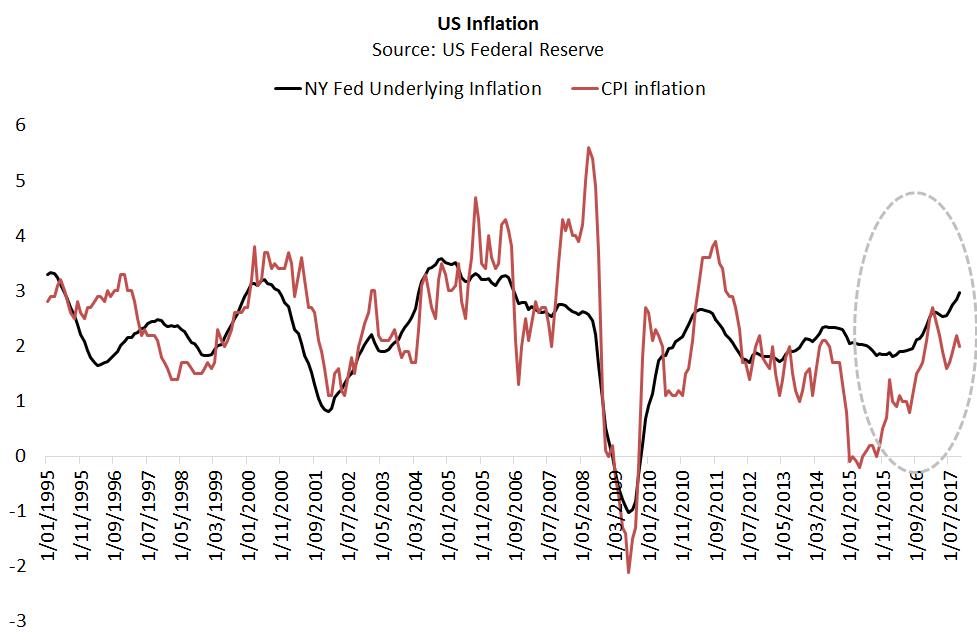

"After forecasting house price rises every year since 2013, I'm happy to double-down on our April 2017 call that the boom is over and project that prices will fall in 2018. While Sydney prices started sliding on September 14 the national five-capital city index did not roll over until October 10 according to CoreLogic numbers. (I sold my house a couple of weeks ago.) Whereas Sydney values have slumped 1.9 per cent, prices across the five capital cities have corrected by a more modest 0.4 per cent. And there will likely be the normal seasonality afflicting this data (values typically pull back in December). It's also interesting to observe that there has been no capital appreciation in the stubbornly ebullient Melbourne market since November 24. If our contrarian case for Australia's jobless rate falling below 5 per cent in 2018 comes to pass (the RBA's brighter boffins reckon it will be 5.5 per cent in December), the central bank will have no choice but to raise rates once or twice assuming it acts rationally. This will reinforce the magnitude of the expected correction. Here there are solid precedents. After the last big bubble that kicked off in earnest in 2001 and ended in December 2003, Sydney prices fell 6.3 per cent in the following three years. In the 12 months after their 2003 peak, dwelling values in Melbourne and across the five largest cities declined by 3 per cent and 3.5 per cent respectively. Of course back in 2003, the household debt-to-income ratio was merely 150 per cent, which is miles below the current 194 per cent mark. Remember that before the RBA blew this latest bubble with irresponsible rate cuts between 2013 and 2016, the debt-to-income ratio was sitting at 167 per cent. The massive blowout is a function of its financial imprudence, repressing savers in the name of bailing out borrowers. Although Sydney prices fell 2.1 per cent annually over the three years spanning December 2003 to December 2006, Australia's jobless rate actually dropped from 5.7 per cent to 4.5 per cent. And the RBA's cash rate climbed from 5.25 per cent to 6.25 per cent. Contrary to economist claims, house prices can in fact fall while the labour market improves. Now fast-forward to the most recent case study. This superseded the January 2009 to June 2010 boom when national prices jumped 20 per cent care of the RBA's 2008 rate cuts. After the cash rate increased from its then "crisis level" of 3 per cent to 4.75 per cent, home values shrunk 6.7 per cent between late 2010 and early 2012. As a minimum I expect prices to match this result. Assuming 100 basis points or more of rate increases, my central case is a 10 per cent plus drawdown in what should be a relatively benign mean-reversion in Australia's otherwise unprecedented house price-to-income ratio. The doves tell us the RBA will never hike again because inflation is dead. But one need look no further than the US economy, where the jobless rate has declined to 4.1 per cent, to see through this ruse. The New York Federal Reserve has just launched a monthly measure of US inflation, called the underlying inflation gauge (UIG), which it says is a "more accurate forecast of inflation compared with [traditional] core inflation measures". After troughing in December 2015 at 1.84 per cent, the New York Fed's UIG has spiked to 2.96 per cent in October 2017. This is way above the median UIG estimate since 1995 of 2.2 per cent, and higher than the December 2006 level of 2.7 per cent. Make no mistake doves, high core inflation in the world's largest economy has arrived. The laws of supply and demand are inviolable and if labour market tightening persists, wage inflation will lift off its low base. The US Federal Reserve expects three rate hikes in 2018, but this supposes the jobless rate only contracts from 4.1 per cent to 3.8 per cent by the end of the year. Our analysis implies it will fall to around 3.5 per cent, which brings a fourth hike on to the table." Read the full article at AFR here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

3 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment