How Australian equities provide tax-effective income and growth

To most readers, domestic equities is an asset class that needs no introduction. But the fundamental basis of investing in Australian shares can often be overlooked - that is, by purchasing shares you are a becoming a part-owner of a businesses and ultimately share in their profits. While markets can be irrational - generally speaking, as profits grow so should the share price and dividends.

So how has owning parts of publicly listed Australian companies fared for Australian investors over the years? The data will tell you that, overall, Australian equities have provided very good long-term returns despite bouts of panic, pain and the odd corporate collapse.

Fellow academics, Dimson, Marsh and Staunton, who published the 2020 Global Investment Returns Yearbook for Credit Suisse estimate that Australian shares have recorded the highest real returns (returns after inflation) of all major equity markets over the period 1900-2019. That is to say at 6.8% p.a over the last 120 years, the lucky country has delivered the best market returns over the long run among global peers.

The same academics also estimate that Australian equities have earned more than 6% p.a. more than bond and cash investments. And because they undertake an international comparison, they don’t even factor into account the value of franking credits which have further added to returns for Australian investors over the past 30 odd years.

In my opinion, our taxation system is a compelling (but not the only) reason for many Australian investors, particularly retirees, to consider adding an allocation of actively managed domestic equities to their income generating investment portfolios. I will explain just how much addition income can be generated through franking credits shorty. First, a quick explanation.

What are franking credits?

Franking credits are taxation credits that often accompany dividends paid to investors. They represent a tax credit for the Australian company tax that’s already been paid by the company. For large companies, this franking credit is normally based on a 30% company tax rate.

A $7 fully franked dividend, therefore, carries a $3 franking credit (being 30% of the pre-tax $10 profit from which the dividend is paid). These franking credits can be exceptionally valuable for Australian investors, as the credit can be used to offset against personal or superannuation tax payable, and for low tax investors, is refundable. For example, for a pension phase superannuation investor who is subject to a zero-tax rate, the government will actually fully refund franking credits.

Plato estimates that franking credits have added an extra 1.4% p.a. to the share market returns to Australian tax- exempt investors over the past 15 years.

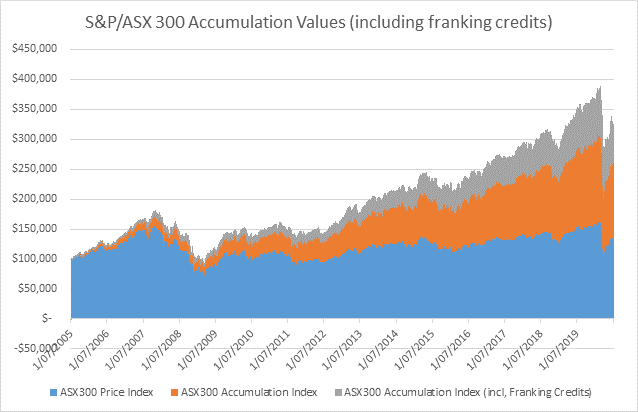

Figure 1 shows the accumulated capital growth, cash dividend and franking credit returns from $100,000 invested into Australian shares from 1 July 2005 to 30 June 2020, based on the S&P ASX300 Tax Exempt Franking Credit Index.

For tax-exempt investors, Australian shares have generated a total return of 8.1% p.a. over that time, comprised of 2.4% p.a. capital growth, 4.3% p.a. cash dividends and 1.4% p.a franking credits.

Figure 1 also highlights the power of compounding. Annual total returns of 8.1% p.a. have compounded an initial $100,000 investment to over $300,000 over 15 years.

Figure 1. Returns on Australian shares for the 15 years to June 30, 2020.

Source: Plato, S&P.

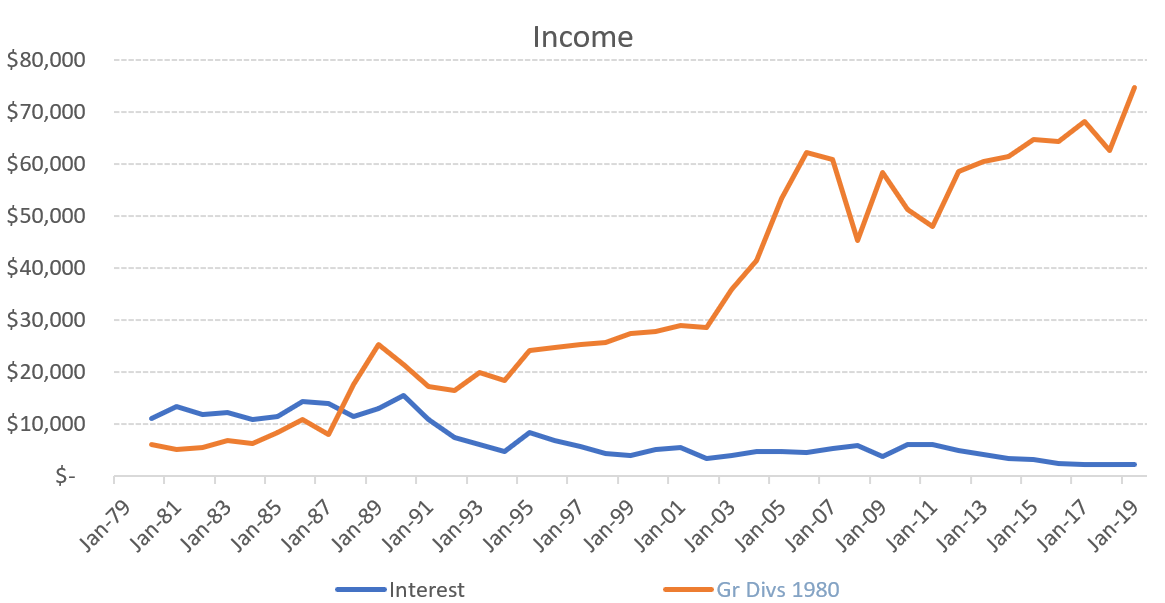

To give you a longer-term perspective on investing in Australian equities for income, in Figure 2, we have plotted the annual income stream (including franking credits) generated from $100,000 invested in Australian equities way back at the start of 1980 and up to 2019. For comparison purposes we also plot the income stream from a similar $100,000 invested in bank bills. Interest rates were double digit in the 1980’s and interest income exceeded dividend income until the late 1980’s, but after that annual gross dividend income steadily grew to over $70,000 in 2019.

Note, this is not intended to be a comparison of capital returns, as equities and bank bills have different risk profiles.

Figure 2. Gross income generated from a $100,000 investment in Australian Shares at the start of 1980.

So, history tells us, domestic Australian equities, can provide both capital growth and great income potential - a dual role in an investor’s portfolio.

Liquidity is also a consideration for many when allocating capital to different asset classes and Australian large cap equities are broadly very liquid investments. Whether one purchases shares direct, or invests via a managed fund, normally one can sell or liquidate those investments and receive the proceeds within 2 days, although some managed funds may have longer settlement periods.

But there are risks

Both graphs above highlight, in parts, just how volatile the ride can be for Australian equity investors in the short-term.

In figure 2 you can see that whilst dividends have steadily grown over the past 40 years, there were periods of lower dividends. Notably dividends fell in the ‘recession we had to have’ in 1990-1992 and during the GFC in 2008/09. It also highlights that dividends rebounded after these setbacks as the economy improved on the back of fiscal and monetary stimulus.

Most recently, the height of COVID-19 pandemic here in Australia highlighted the risks in short term Australian equity investing. The S&P/ASX 300 Share Price Index fell 36% from its peak in late February to March 23, as panic spread about the impacts of the pandemic. As pandemic concerns have eased, the market has rebounded significantly off its March 23 lows, jumping 31% higher to June 30.

During the ‘recession we had to have’ and the GFC, dividends fell approximately 30%, and we expect a similar decline in dividends is likely in 2020 due to the economic impacts of COVID-19 pushing Australia into a recession. But the reality is, that income from all asset classes will fall significantly. For example, the Reserve Bank of Australia cut interest rates from 75bp to 25bp in March in response to the pandemic, representing a 67% cut in income on overnight cash.

Making ends meet

Those record-low cash rates have made it, arguably, harder than ever for many investors, particularly retirees, to generate income. But despite volatile times in equity markets strong dividends from Australian shares can help investors make ends meet.

COVID-19 has also highlighted the one free lunch of investment – diversification. Whilst companies like Qantas and Virgin have been impacted by the pandemic, many other companies are doing very well.

Traditionally Australians have looked to the Big Four banks and Telstra for income, but at Plato, we have been looking beyond those for many years.

In a post-lockdown world (at least outside of Melbourne, for now), we are very positive about the profit and dividend outlook for companies like Fortescue Metals (iron ore), Woolworths (groceries). Wesfarmers (Bunnings and Officeworks) and CSL.

Indeed, we believe there is scope for many companies to maintain or increase dividends in the current environment, but one needs to be very discerning. Stock selection will be very important. Separating the wheat from the chaff is key... Or in this case separating strong dividend payers from “dividend traps”.

Dividend traps are stocks that have historically paid dividends and may be trading on “good” historical dividend yields, but are likely to have to significantly cut or completely omit dividends for some time. Avoiding dividend traps is key to equity income investing, and we focus a lot of our research effort on avoiding these traps.

Wayne Gretzky, the famous Canadian ice hockey player, famously said: “Skate to where the puck is going, not where it has been.” We have a similar philosophy at Plato with regards to income. Investors need to move their portfolio to where the future income is going to be, rather than what has produced income in the past, but may not be a great opportunity going forward.

By avoiding dividend traps and actively rotating our holdings into companies with the highest likelihood of strong future dividends, the Plato Australian Shares Income Fund has been able to deliver 3.7% pa more gross income than the market since inception (9 September 2011 to 30 June 2020) as well as outperforming the S&P/ASX 200 Index on a total return basis (11.1% total return since inception).

In dollar terms, an initial investment in the Plato Australian Shares Income Fund at the inception date of 9 September 2011 of $100,000 would have generated gross income of just over $100,000 (including franking credits) over that time, with a capital value above $110,000 as at 30 June 2020. This level of income is $34K above that income generated by the S&P/ASX 200 Index during the last 8 years and 8 months.

While past performance is not an indicator of future performance, what I attempt to highlight is the way a diversified and actively managed portfolio of quality Australian equities could help investors make ends meet from Australian shares, as opposed to just trying to select one or two high yielding stocks, which carries significantly higher levels of risk. This is how we at Plato attempt to help investors solve the ‘income puzzle’.

Want to learn more about Australian Equity income?

Plato Investment Management is an Australian owned boutique equities fund manager specialising in maximising retirement income for pension phase investors and SMSFs. To find out more click "contact" below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006.

Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street Global Advisors, responsible for over $10B in active and enhanced equity investments. Earlier he held various positions at Westpac Investment Management, including Chief Investment Officer, Head of Equities. During his time at Westpac he was also instrumentally involved in the mergers of BT and Rothschild.

Don has a strong interest in responsible investment and governance. He has a PhD in Finance and a Bachelor of Commerce with First Class Honours from UQ, and a University Medal.

Featuring

Dr Don Hamson,

Plato Investment Management

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006.

Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street Global Advisors, responsible for over $10B in active and enhanced equity investments. Earlier he held various positions at Westpac Investment Management, including Chief Investment Officer, Head of Equities. During his time at Westpac he was also instrumentally involved in the mergers of BT and Rothschild.

Don has a strong interest in responsible investment and governance. He has a PhD in Finance and a Bachelor of Commerce with First Class Honours from UQ, and a University Medal.

1 topic

1 stock mentioned

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006. Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street...

Expertise

Comments

Comments

Sign In or Join Free to comment