How do microcap managers perform in the long-term?

Active microcap managers demonstrated in FY17 that this part of the stock market can be a great alpha generator for managers (and their investors). In this wire, we ask how they have stacked up against their benchmarks over 3, 5 and even 10 years...

Alpha is there if you do the work

A lot of leg work is required by microcap managers as 70% of the stocks outside the ASX top 200 companies have no broker coverage or sell side research at all, according to recent research by Perennial.

Of course, academics will tell us active managers can’t generate alpha and ETF product promoters will tell us active management is dead. As popular discourse maintains that the majority of active managers can’t outperform the index or the ETF’s, which track them over time.

Therefore, what if we delved into some longer-term performance figures of active Australian microcap managers... what would it reveal? We took a look, just in case FY17 was just a good year for microcap managers, the stats from which we discussed in our last wire and can be accessed here.

Performance over the long-term

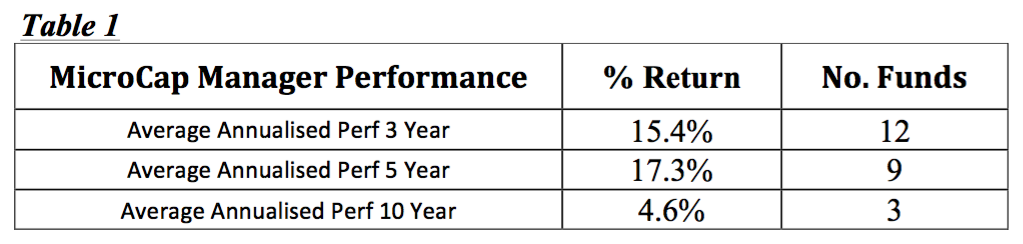

Table 1 outlines the average annualised performance of active Australian microcap fund managers over 3, 5, and 10 years and the number of funds comprising the average.

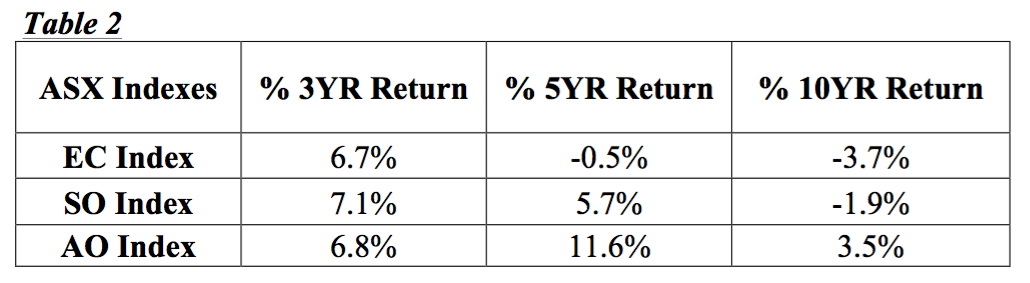

Table 2 illustrates the annualised returns of the following 3 indexes’

- The ASX Emerging Companies Accumulation Index (EC)

- The ASX Small Ordinaries Accumulation Index (SO)

- The ASX All Ordinaries Accumulation Index (AO)

Even a cursory appraisal of the data attests that active Australian microcap fund managers have delivered nothing short of stellar performance over the long term.

Be it versus The ASX Emerging Companies Accumulation Index (EC) the ASX Small Ordinaries Accumulation Index or even the broader Australian share market if we take the All Ordinaries Accumulation Index as a general proxy for it.

Has the whole field delivered?

It must also be noted that these are the index returns where no fees or expenses have been deducted. Thus, the ETF’s which track these indexes would provide slightly lower returns due to the fees and expenses drag over time, no matter how low these fees are. Consequently, the outperformance versus ETF’s would be even higher than that of outperformance achieved over the index returns displayed in table 2. Ah, but what if one or two microcap funds are just dragging up the average you say?

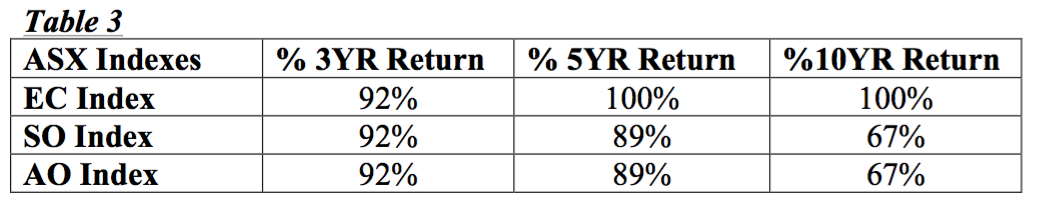

Table 3 displays the total percentage of funds which outperformed the index on a relative basis.

As can be seen the majority of active microcap fund managers are outperforming the index or the ETF’s designed to track them over time.

I don’t want sound like I am here to bash ETF’s, I am not. ETF’s have their place in the market and investors portfolios. However, one must be careful not to blindly accept that active managers can never outperform the index over time. Similarly believing that low-cost ETF’s are the panacea investors have been searching for in order to generate acceptable portfolio returns at a reasonable cost can also be fool hardy. In other words, don’t throw the baby out with bath water.

Active Australian Microcap Managers have a strong track record of delivering solid returns to their investors. So, taking a step back from all the hoopla surrounding ETF’s currently and researching some of the fund managers listed in my previous wire may be a start for advisors or self-directed investors looking for some alpha in their portfolio.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I focus on ASX listed microcap and nanocap stocks which is anything from $10mil to $300mil market cap and everything in between. This truly is the under-researched part of the ASX. My hope is to bring you interesting microcap stocks and news.

5 stocks mentioned

I focus on ASX listed microcap and nanocap stocks which is anything from $10mil to $300mil market cap and everything in between. This truly is the under-researched part of the ASX. My hope is to bring you interesting microcap stocks and news.

I focus on ASX listed microcap and nanocap stocks which is anything from $10mil to $300mil market cap and everything in between. This truly is the under-researched part of the ASX. My hope is to bring you interesting microcap stocks and news.

Comments

Comments

Sign In or Join Free to comment