How should you read a broker report?

Broker reports are one of the most widely-used information sources for equity investors of all stripes, and there is no doubt they can be a very useful source of background information on an industry or company. In addition, they provide financial forecasts, valuation estimates and, of course, the analyst’s overall conclusion: buy, sell or hold.

But how should you think about using this information in forming your investment decisions? It would be tempting to think that a professional broking analyst who closely follows a company should be able to provide an authoritative investment view in relation to that company, but is it as simple as that?

One way to shed some light on this question is to analyse the historical evidence. We live in an age of abundant data, and it is not hard to gather a history of broker recommendations, and look at how those recommendations have fared in a statistical sense.

A simple place to start is with a metric called the “Recommendation consensus”. This is a statistic that is calculated by converting every analyst’s recommendation on a stock into a number from 1 to 5 (where a “strong sell” is 1 and a “strong buy” is 5), and averaging across all analysts who cover the stock. This gives us a single figure which, in theory, should tell us something about whether a stock is a good investment candidate.

Recently, we assembled recommendation consensus data for a broad sample of ASX-listed companies stretching back over 15 years. The results were interesting.

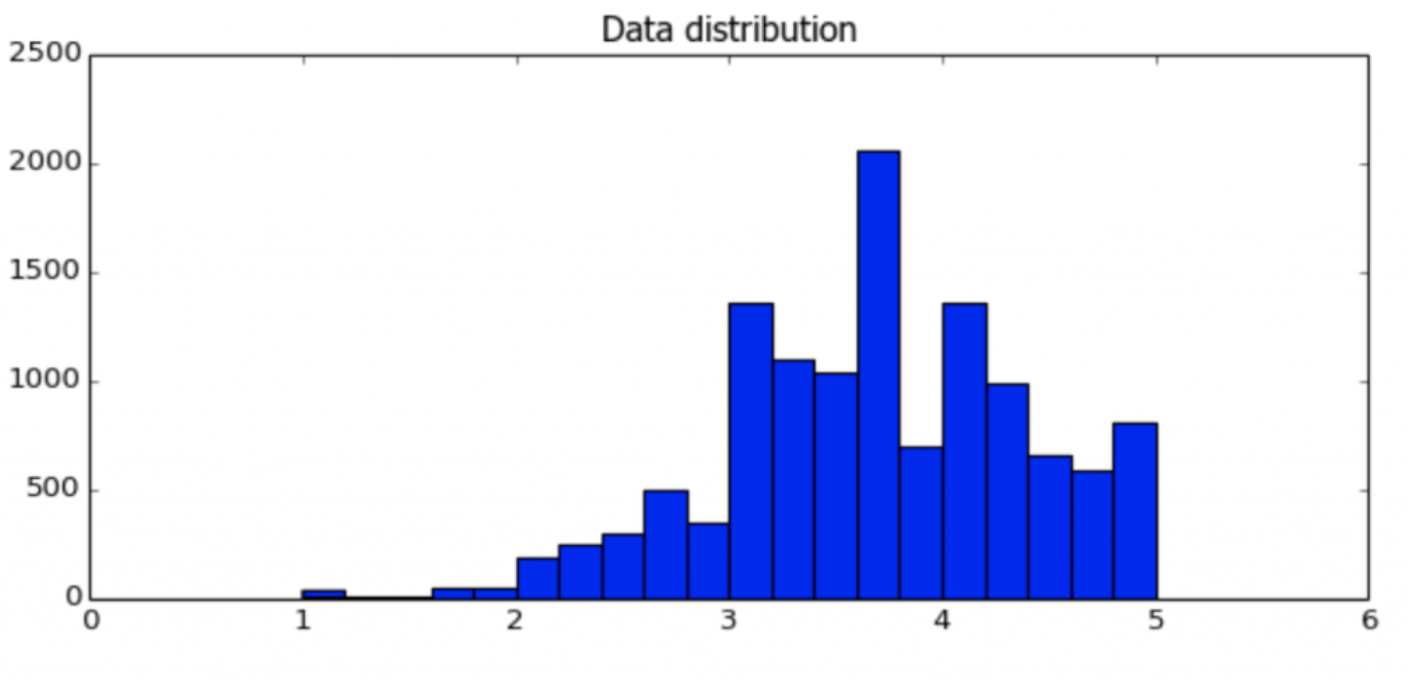

Firstly, we can look at the distribution of recommendations, which is set out below:

The first things that jumps out from the chart is its asymmetry. There are very few observations between 1 and 2, and not many between 2 and 3. The distribution is concentrated between 3 and 5, meaning there are a lot of “buy” and not so many “sell” recommendations. This will come as no surprise to many people. Brokers have clear incentives to stay on good terms with the companies they cover (for example to maintain access to management, or to be in a position to pitch for capital raising roles), and so a reluctance to make a “sell” call is understandable. However, it serves as a reminder that when looking at any form of advice you need to be mindful of how it may be shaped by the adviser’s incentives.

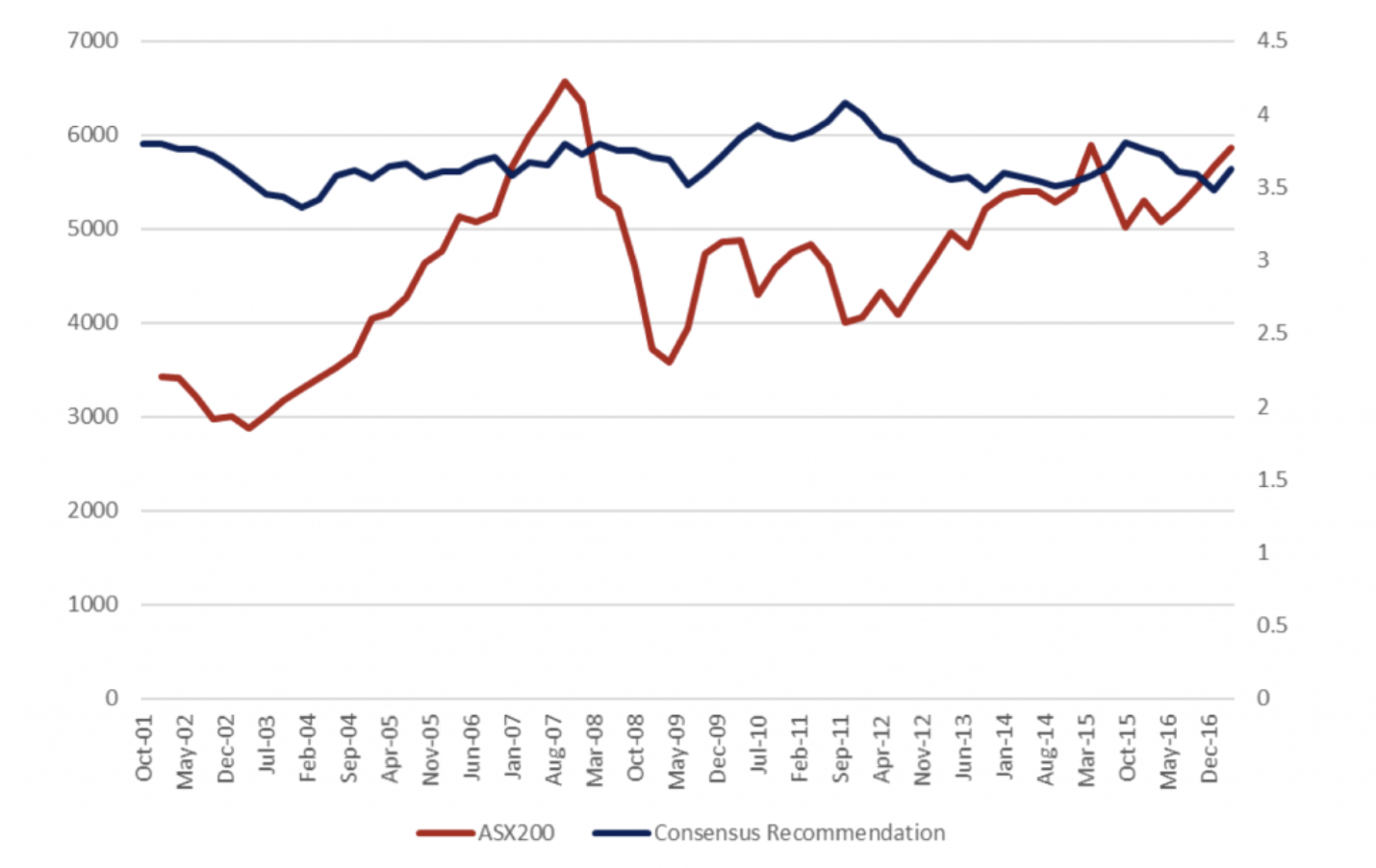

Next, we can look at how the consensus recommendation has changed over time. In the last 15 years, we have seen a wide range of equity market conditions, including a period of attractive valuations at the bottom of the Global Financial Crisis (GFC), and more recently a period of more expensive valuations.

In an ideal world, broker recommendations would all be singing “buy” when markets are cheap, and “sell” when they are expensive. However, as the chart below indicates, this dynamic is subtle at best, with the average recommendation consensus staying within a fairly tight range. Once again, we need to think of this in the context of broker incentives, both at the level of the broking house (who may wish to encourage investors to trade between stocks, rather than exit the market when prices are high), and the individual analyst, who may need to manage career risk by making relative, rather than absolute, recommendations.

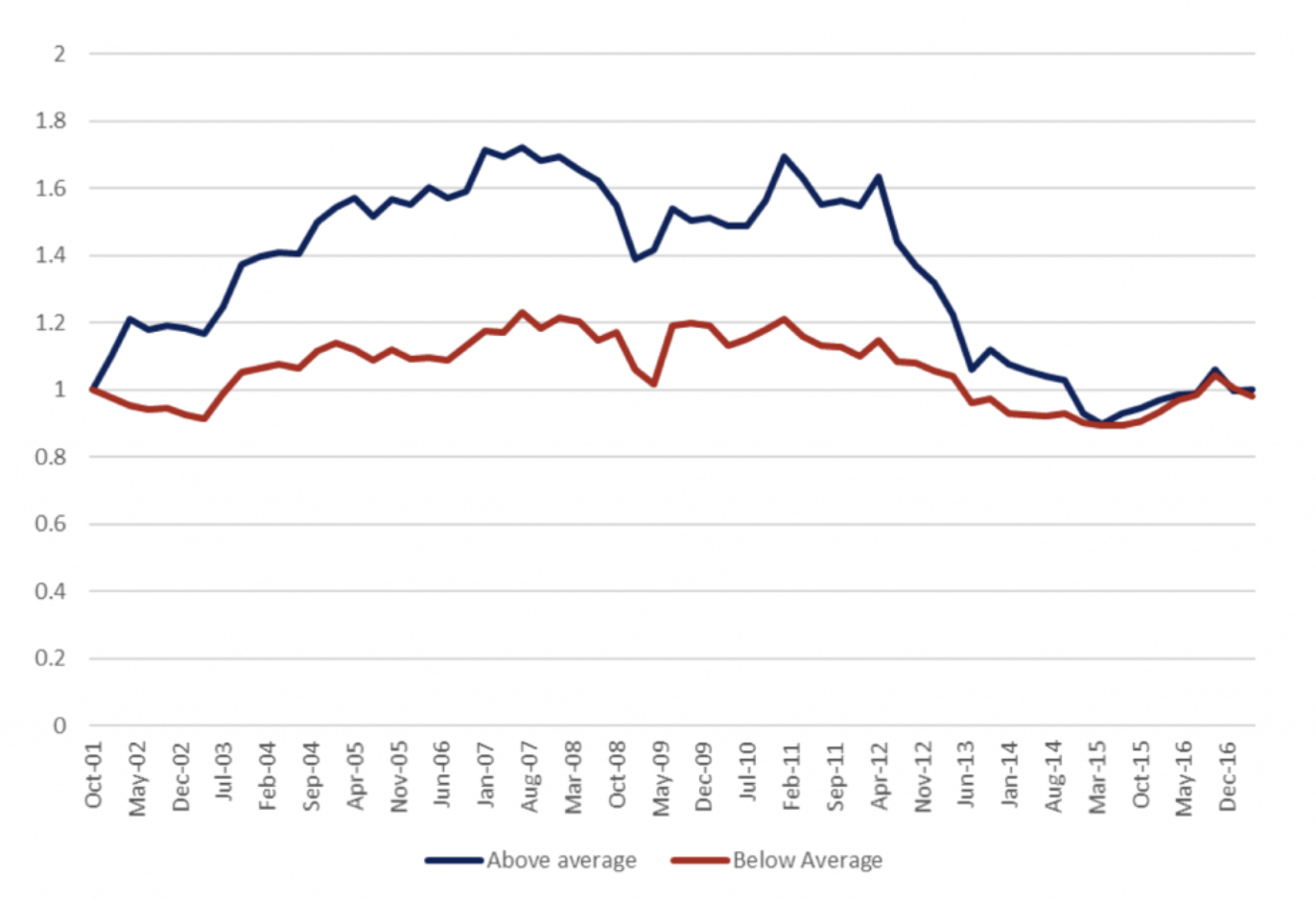

This brings us to the interesting bit: Do companies with a recommendation closer to 5 make significantly better investments than companies with a recommendation closer to 1?

To address this, we split the data into two groups: one containing all the companies with a higher-than-average consensus recommendation, and one containing all the companies with a lower-than-average recommendation. We do this analysis on a risk-adjusted basis, which means that we adjust for the beta of individual companies when looking at outperformance. In a market that goes up strongly, high beta companies will naturally do well (and vice versa), and we risk-adjust to remove this effect from the analysis.

The results are as follows:

As you can see, the first seven or eight years of our sample period saw the higher-recommendation companies delivering better investment performance than the lower-recommendation companies. However, the reverse has been true in more recent years, and the two portfolios end up with pretty-much identical risk adjusted returns over the full period.

It is not obvious to me why this should be the case. One could argue that the industry pressures faced by the broking industry in recent years have led to a loss of experienced talent and a reduction in the quality of sell-side research, but there are other hypotheses that could also be put forward to explain the change in performance. Interestingly, the peak of outperformance for the “Above average” portfolio pretty much coincided with the start of the GFC.

While we can’t definitively explain the pattern above, we can conclude that simply basing investment decisions on the recommendation consensus does not look like a very powerful investment strategy to be following today.

This is not to say that broker research is without value. It continues to provide a good source of industry and company information, and a measure of what near term earnings the market might be expecting from a business. Also, it seems likely that the very best analysts should offer greater insight than a consensus measure that reflects the views of all analysts.

As is often the case, genuine investment edge proves to be an elusive beast, and to extract real value from broker research, investors need to do some homework. In my view, a reader who understands the author and their motivations, and who thinks critically about the information provided, can extract considerable value from a good piece of broker research.

If you would like to read more articles by me, please click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our investment process. Tim remains a shareholder of Montgomery Investment Management.

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Comments

Comments

Sign In or Join Free to comment