How to prepare for widening spreads

Credit spreads, the difference in yield between a bond and a debt security with equal maturities, have tightened towards historically low levels in recent years. This has investors asking, how much further they can go and what will happen if, or more likely when, they start to widen again?

There are a number of factors at hand that may impact both the timing and the magnitude of the widening including the potential unwinding of quantitative easing (QE) globally and tail risk events such as heightened geopolitical unrest.

Before considering these outside factors let’s review the current credit market fundamentals, valuations and technicals.

Corporate leverage is high but stable and earnings are strong

In the March earnings season we saw the increase in leverage, which had been occurring over recent years, finally peak. To date in the June earnings reporting season, leverage has stabilised and earnings have been strong – both of these fundamental facets are positive for credit markets. Importantly, near term risks are limited and defaults are likely to remain low due to easy access to funding, low interest rates, term out maturity profiles and the improving economic backdrop.

Valuations are tight, but not concerning

Credit valuations are tight but this is unlikely to be a catalyst for widening as valuations can remain at these levels for long periods of times (possibly a number of years). In addition, flows into investment grade credit remain very robust with heightened levels of issuance to meet the insatiable demands in the current low interest rate environment. Hence it’s unlikely that any of these factors will lead to a sudden surge of widening credit spreads.

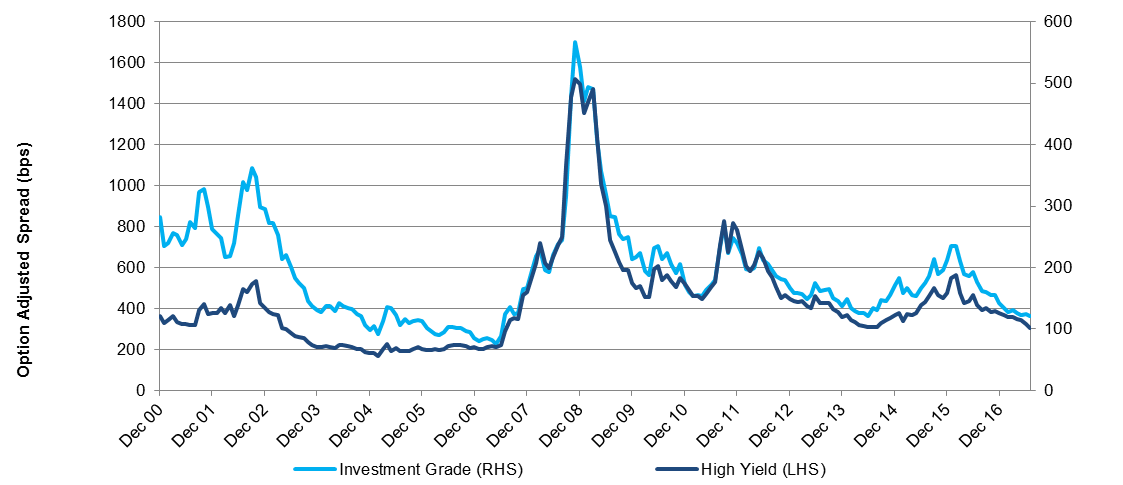

Fig 1: Credit spreads are reaching historic lows but can stay at this level for a period of time

Source: Barclays as at 31 July 2017. Investment Grade: Barclays Global Corporate Aggregate Index. High Yield: Barclays Global High Yield Index

A market correction of some degree is probable…

The size and speed of it is likely to be more tied to the global unwinding of QE than the above factors. As the central banks reduce or halt their asset purchasing programs, all else the same, this will remove these large price-insensitive buyers from the market and they will need to be replaced by another source of demand.

The likely outcome is a decompression in spreads with higher risk securities the most likely to be impacted. In the low yielding environment, investors have been forced into these sectors to meet return hurdles but these sectors are unlikely to actually align with their natural or neutral risk profile. Hence an unwinding of this somewhat forced carry trade will likely result in a net flow out of these higher yielding securities causing a widening in spreads (due to the downward price action).

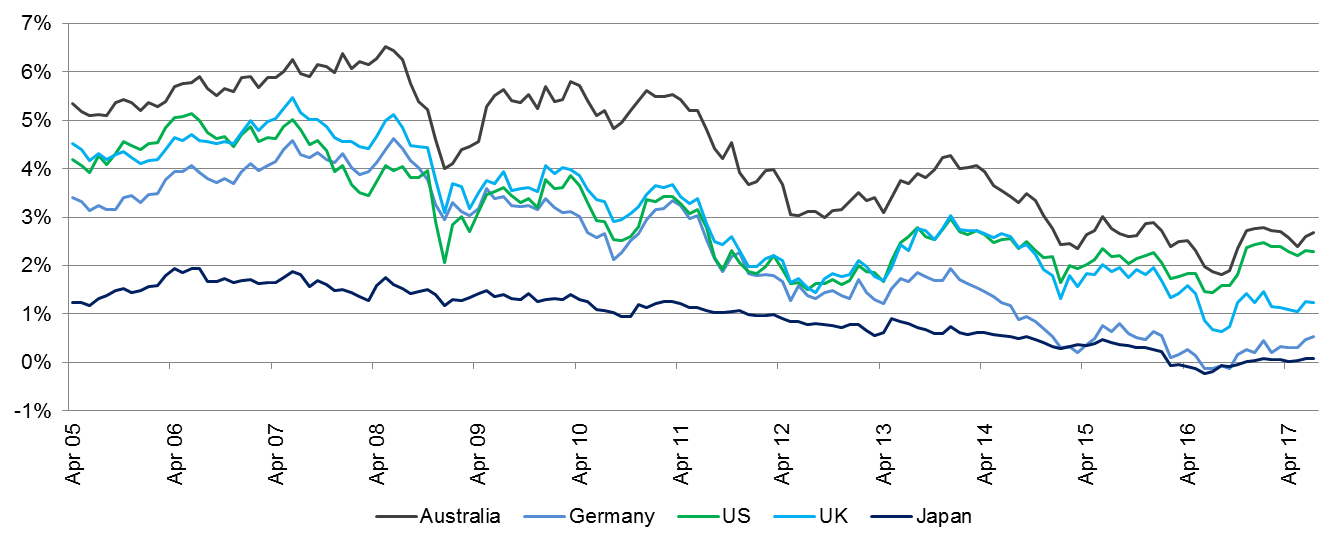

Fig 2: Globally interest rates have continued to grind lower, spiking demand for credit

Source: Bloomberg as at 31 July 2017. Generic 10-year government bond yields.

Increased geopolitical uncertainty remains a tail risk to markets

Increased geopolitical uncertainty remains a tail risk to markets in general and whilst credit markets have remained resilient of late this remains an unknown variable that could derail market stability. There is also the unknown risks as central banks, who have previously been a stabilising factor for markets, start to taper QE – a process that we’ve not yet lived through, making it impossible to learn from prior situations and predict how the market may react. In addition to rates shock in monetary policy, any price shocks in oil also have the potential to turn market sentiment and derail technical support, particularly in the high yield market. Political risks are also an unknown with Italian elections in 2018, Brexit and the US Administration’s inability to pass policies that had been expected to positively impact growth as well as continued political instability in the US. Overall we view the occurrence of these risks as potential not probable.

How we are positioning ourselves

A move wider in spreads may come in many forms – be it a slow grind wider, a sudden shift and to what magnitude, or spreads remaining steady whilst rates rise globally. Each of these scenarios will impact credit funds in different ways.

We believe that returns often overcompensate for credit risk, and that diversification across a large pool of lowly correlated assets will generate positive ‘value-for-risk’ outcomes.

But with a sudden and large move wider in credit spreads (the worse of the possibilities) this would create liquidity issues as investors all seek to exit positions at the same time. Funds / Investors with less diversification are more likely to see a larger negative impact against this backdrop.

For further insights from Colonial First State Global Asset Management, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

The word “sentier” means path. We chose a brand name that reflects our long-term commitment to following our own path; to invest responsibly over the long term for the benefit of our clients and the communities in which we invest.

First Sentier Investors

The word “sentier” means path. We chose a brand name that reflects our long-term commitment to following our own path; to invest responsibly over the long term for the benefit of our clients and the communities in which we invest.

First Sentier Investors

The word “sentier” means path. We chose a brand name that reflects our long-term commitment to following our own path; to invest responsibly over the long term for the benefit of our clients and the communities in which we invest.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

4 undiscovered gems as gold prices hit record highs

Livewire Markets

Equities

Bizarre: The $11m microcap sitting on a $21m cash pile

Livewire Markets