How will rising CV-19 cases impact global equity markets this week?

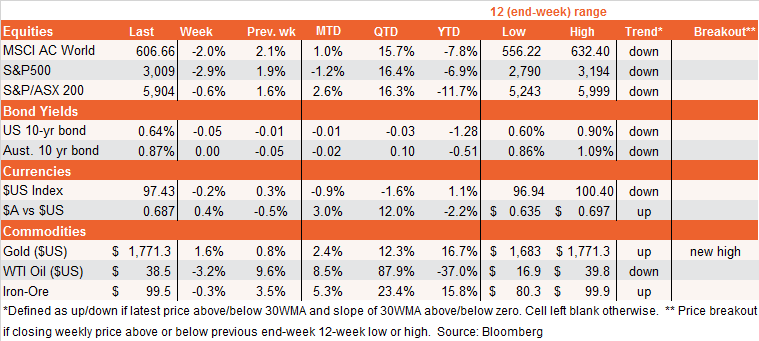

The continued rise in in U.S. COVID-19 cases further undermined risk sentiment last week – even though, as U.S. President Trump noted, increased testing appears an important factor behind the rise (although the percentage of positive tests is also increasing). The S&P 500 lost 2.9%, with a hefty 2.4% decline on Friday. Gold again demonstrated its safe haven status, rising 1.6% and breaking above its consolidation range of the past few months. At 3,009 points, the S&P 500 is now a hair’s breadth away from its 11 June closing low of 3,002 (and intra-day low of 2,965 on June 15), which if broken would confirm the first significant ‘lower high’ and ‘lower low’ in the rally since late March.

In terms of the week ahead, what’s critical for markets of course, is not so much the rise in CV-19 cases per se, but whether this leads to a return of draconian lockdowns in major U.S. States. So far at least, that’s not been the case, with Texas and Florida focusing on closing down bars again, given evidence that it’s the partying younger population that is fuelling the current outbreak. That could also account for the relatively low death rate so far, though this could also reflect lags. Either way, the obvious market focus this week will be whether the case count and/or death rate rises, whether it spreads to other States and if more restrictive ‘stay at home’ orders are introduced. By contrast, if the rate of new cases starts to stabilise before more restrictive measures are introduced, stocks could breathe a huge sigh of relief this week.

In terms of economic data, last week we got decent May bounce-backs in both manufacturing and non-manufacturing PMI indices in Europe and the U.S. – as expected – though weekly U.S. jobless claims again failed to drop as quickly as the market hoped. This week U.S. payrolls on Friday are expected to show an encouraging 3 million further lift in employment during June (after a 2.5 million gain in May), with the unemployment rate dropping to 12.3% (from 13.3%). Of course, this will leave many millions still unemployed (employment collapsed by 20 million in April), and the market will start to consider this re-opening data bounce as old news if new restrictions are soon imposed.

Australian market

Australia’s own COVID-19 breakout in Melbourne attracted much focus last week, but as in the U.S., the fact draconian new social distancing restrictions have not been introduced was something of a relief. Melbourne is trying valiantly to tackle the problem with more targeted measures this time around, and whether this can remain the case will be a natural local market focus this week.

In terms of data, official retail sales on Friday should merely confirm the strong May bounce-back evident in preliminary data already released. May home building approvals on Wednesday, however, are expected to drop around 10% after holding up better than feared in April. Also due Wednesday, Core-Logic is likely to reveal the second successive modest monthly fall in national house prices in June, though I note the validity of this data has come under some question of late given the high level of non-disclosed sale prices. To the extent it’s more likely very weak rather than very strong house price results are being withheld, the degree of recent house price weakness could be somewhat understated.

Despite last week’s risk-off sentiment, it’s noteworthy that iron-ore prices and the $A remained fairly resilient – with the former still being helped by supply side disruptions in Brazil and China’s ongoing economic rebound.

Never miss an insight

Each week I will publish my latest thoughts on the macro events shaping the ETF landscape. To be the first to read my insights, hit the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

3 topics

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets