Uncertain about property prices? Head up the capital stack

Akin to the debate over the shape of the economic recovery, the big question for the Australian housing market isn’t if prices will fall. It’s by how much, and more importantly: what next?

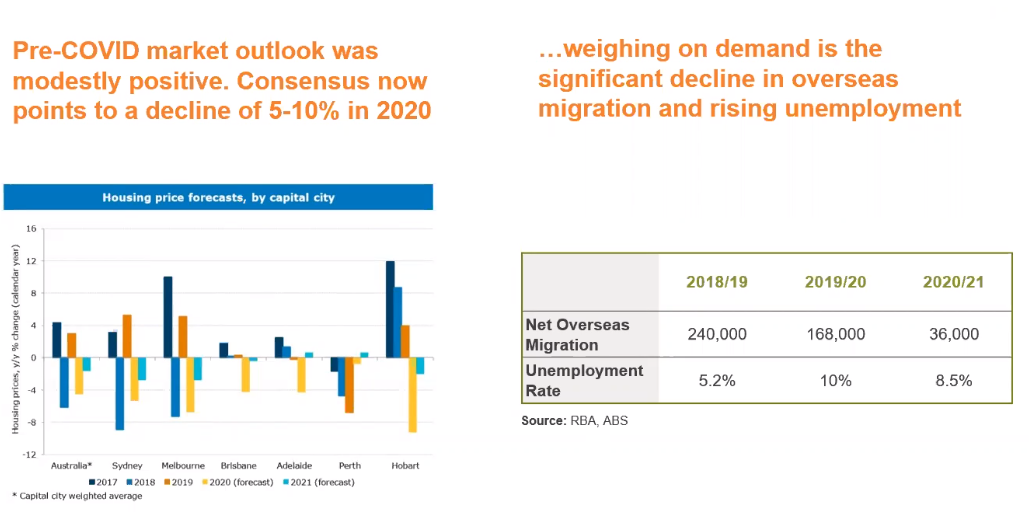

Real estate debt specialist Freehold Investment Management expects the implications of COVID-19 to translate into an up to 10% decline in national house prices this year from their previous peak, before flattening in the first half of calendar 2021.

“The negatives weighing on the market are rising unemployment and declining net overseas migration, which is predicted to drop 30% this calendar year and an 85% next calendar year,” Damien Cronin, who co-manages the Freehold Debt Income Fund with Omar Khan, told investors at a recent client webinar.

Graph 1: House price forecasts (click to enlarge)

SOURCE: ANZ RESEARCH, FREEHOLD INVESTMENT MANAGEMENT

SOURCE: ANZ RESEARCH, FREEHOLD INVESTMENT MANAGEMENT

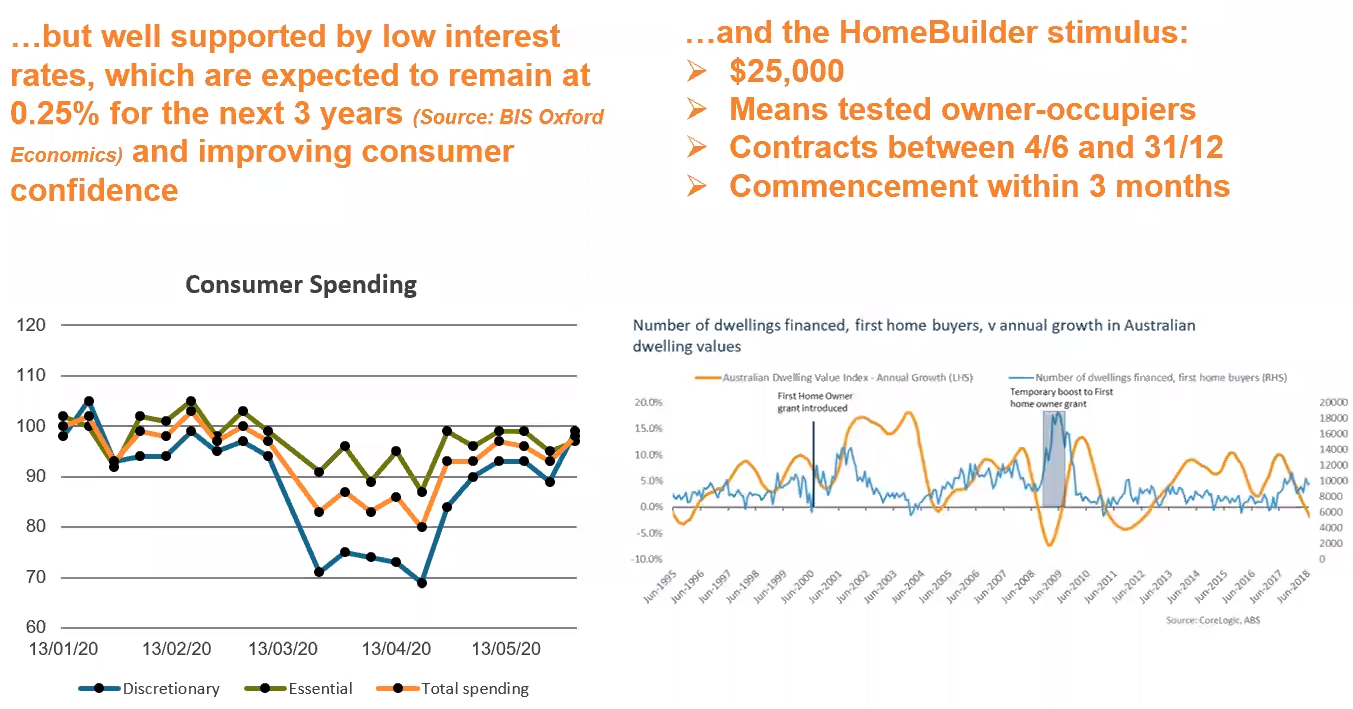

But that’s about as bad as things will get before supporting mechanisms start to take effect and buoy the sector:

- Firstly, interest rates are at an all-time low and are expected to remain at 0.25% for the next three years. This will assist in consumer confidence.

- Secondly, the Australian Government’s HomeBuilder stimulus package will contribute $25,000 per dwelling, in addition to state incentives as a further sweetener for buyers.

- Thirdly, there will be less housing stock released into a government-stimulated market with improving sentiment.

Graph 2: Supporting mechanisms for housing (click to enlarge)

SOURCE: ALPHABETA, ILLION (JUNE 2020), FREEHOLD INVESTMENT MANAGEMENT

SOURCE: ALPHABETA, ILLION (JUNE 2020), FREEHOLD INVESTMENT MANAGEMENT

A general recovery in economic activity should underpin a stabilisation in prices in 2021, according to Cronin. “Obviously, those factors in conjunction with population growth and employment in the broader economy really do drive house prices in this market,” he says.

Managing investment risk in a falling market

A falling housing market requires careful navigation for managers like Freehold, whose fund provides capital to finance the purchase of land, residential construction and completed residential stock and pays out 7-8% monthly annual returns in the form of interest paid to unitholders.

Against such a backdrop, Cronin says he’s taking a conservative approach to lending and a bias towards quality developers with a track record of delivering quality projects on time. The debt fund has an average LVR (loan-to-value ratio) of under 55% to withstand material price declines.

“With that backdrop of a 10% decline in the housing market, senior debt for us remains a very good place to be on a risk-adjusted basis. We’re also mindful of that outlook when we assess any new opportunities and bake that into our underwriting to ensure that we maintain the sort of coverage that we want.”

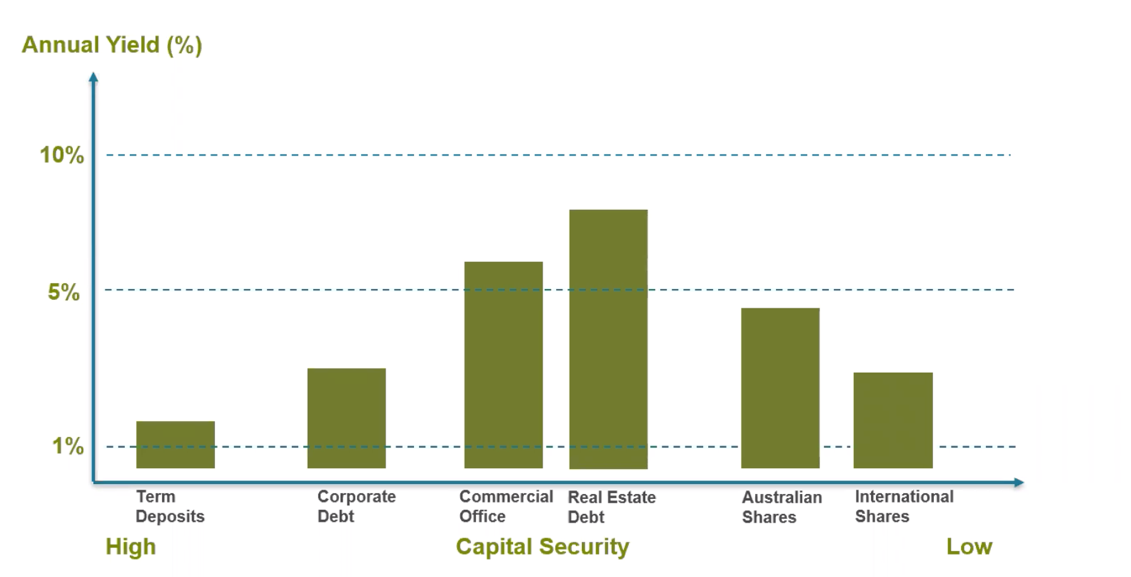

Investors' income challenge

At the webinar, the Freehold Debt Income Fund’s co-manager Omar Khan also spoke about the challenge investors’ face in generating yield. With term deposits at only ~1.5% and equity dividends falling as well as prices being challenged, investors are seeking alternatives for a stable income.

Graph 3: Yield comparisons across asset classes (click to enlarge)

SOURCE: FREEHOLD INVESTMENT MANAGEMENT (FOR ILLUSTRATIVE PURPOSES ONLY)

SOURCE: FREEHOLD INVESTMENT MANAGEMENT (FOR ILLUSTRATIVE PURPOSES ONLY)

He pointed to growing interest in secured real estate debt, which ranks higher in the capital stack (think security) than equity and produces an average gross return of 8-12% per annum with significantly less drawdown risk relative to equities.

"We believe real estate debt is a very attractive investment class in the current climate for the yield, capital security, and liquidity it offers. The last point, liquidity, is important to note because the average term of the loan tends to be between 12 to 24 months, and hence investors can be repaid periodically in a well-diversified fund."

Here, Omar discusses the 3 reasons why real estate debt appeals to income investors and explains the growing role of this asset class. You can also listen to Freehold's generating income from real estate debt webinar here.

Focus on recurring income and low volatility

Throughout the market volatility, Freehold has been able to pay a monthly income distribution consistently, and the fund is performing above its target return of 7 – 8% p.a. Learn more about their strategy here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Featuring

.png)

Omar Khan,

Freehold Investment Management

Omar has over 15 years' experience across funds management and real estate. His experience extends across structuring, due diligence, capital raising, as well as managing and growing funds management businesses.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

4 topics

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment