TOL - 1st Jun, 2021

Like it or not, it's 11 o'clock in mining

Mining is booming: a number of mineral commodities have recently set new records and share prices of major miners have also reached fresh all-time highs. Ultra-accommodative global monetary policy settings have ushered in an era of ‘free money’ which has inflated asset markets. Liquidity in the form of investor funding is pouring into mining equities, and this has opened a window which only ever occurs in the latter years of a boom – the ability to conduct large mining IPOs. Large mining IPOs define 11 o’clock on the Lion Clock – a time when liquidity is uber-abundant, the market rewards growth, puts high values on exploration assets, junior companies perform strongly and is the final (often multi-year) episode of the boom.

Figure 1 - The Lion Clock (Source: Lion Selection Group)

This might not prove to be a popular conclusion, it hasn't been when it was 11 o'clock before. And, it is certain to ignite debate which is absolutely welcomed. A personal request - please do not justify any perspectives with the phrase "its different this time...".

Mining Cycles and the Lion Clock

The Lion Clock depicts the mining cycle according to liquidity indicators that are diagnostic of the different stages of the cycle. Mining cycles are defined by equity prices of mining companies, but the underlying driver of mining equity prices is liquidity – money flowing into, or out of the mining sector. The availability of funding drives behaviours in the market and the sector which are characteristic of cycle maturity.

There are two aspects of mining cycles that must be emphasised:

- Mining is cyclical and regularly enjoys booms, which have always ended with a bust.

- The top of any market cycle, mining booms included, are notoriously hard to pick. Increased liquidity (which is easy to spot) is not what causes a bust, but creates conditions that are ripe for a collapse following a suitable catalyst (which is the highly unpredictable ingredient).

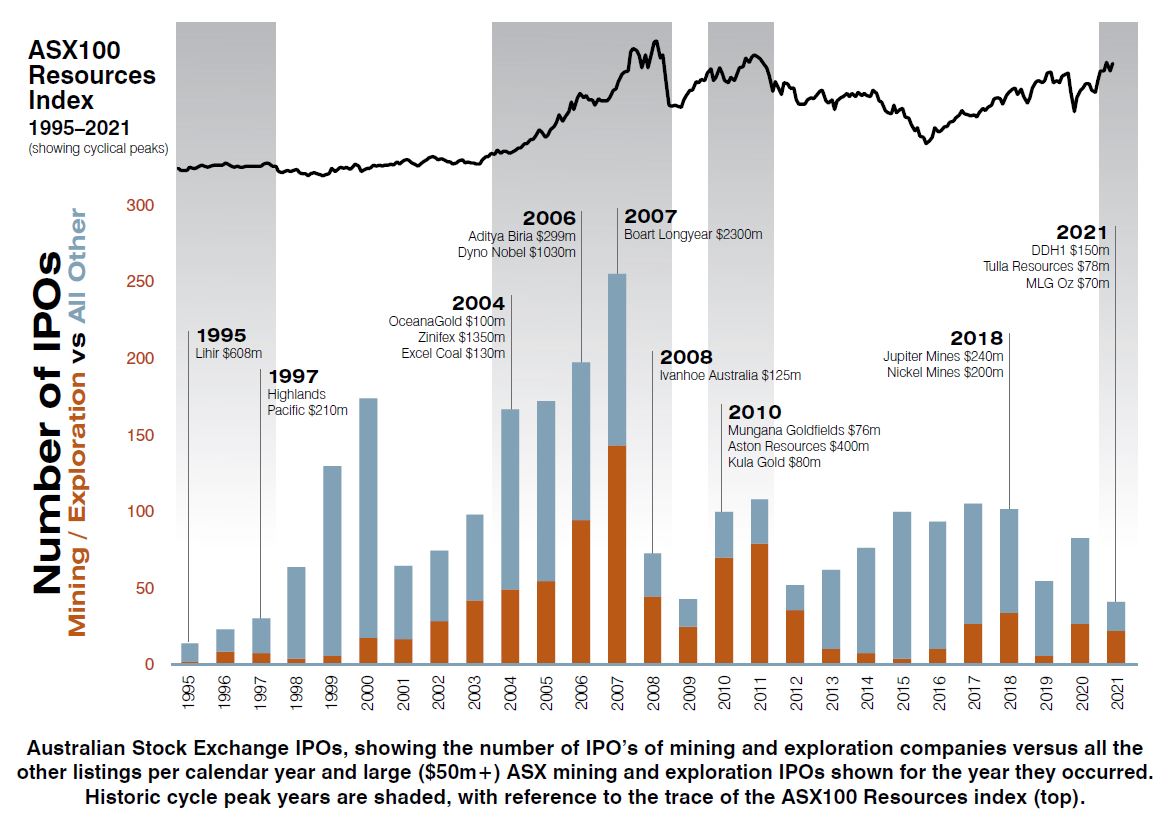

Mining and Exploration IPO’s – the litmus test of 11 o’clock

The number and size of mining and exploration focused IPOs is the best litmus test of liquidity there is for the mining sector. In a weak mining market (such as 2015), an exploration IPO is extremely challenging and listing an established or hopeful miner is impossible, but in boom time you can list just about anything and the number and size of mining and exploration IPOs are high.

There were five exploration IPOs onto ASX in 2019 and 26 in 2020. Year-to-date there have been 25 which is almost as many as the 2020 full year and raising $10m or more for an exploration IPO now appears more the rule rather than the exception. Large mining IPO deals are also clearing the market: there have been three IPOs in 2021 raising A$70m or more (Tulla Resources, DDH1 and MLG Oz) in the mining sector.

But it’s the IPO pipeline that really demonstrates the sort of liquidity that is around for miners at present, it looks as well stuffed as a Christmas stocking:

- According to the Australian Financial Review, copper focussed 29Metals is in advanced stage of IPO preparation for an ASX listing and is expected to raise in excess of A$500m

- A London listing for Russia and West Africa focussed Nord Gold has been touted which would reputedly attract a multi-billion dollar valuation.

- In Indonesia, where the local exchange has seen the emergence and impressive growth of several substantial local gold businesses, an IPO to raise US$500m and list the Toka Tindung gold mine was well advanced before being postponed in April to await a better gold price.

These deals aren’t alone – there are others with the aspiration to raise over A$100m and establish new, significant sized mining businesses under serious contemplation but so far less visible, that are likely to target listings on Australian, European and Asian exchanges whilst the liquidity window is wide open.

Combining just the visible potential of 29Metals and Nord Gold listings with the current ASX trend of increasing number and size of mining and exploration IPOs puts 2021 on track for a year commensurate with years such as 2006 or 2010.

The emergence and tempo of large mining focussed IPOs is a serious signal from the market which betrays unusually high liquidity that has historically only presented in the lead up to cyclical peaks. Typically the investment market has only supported large (multi $10’s millions to $100’s millions raisings) mining or exploration focussed IPOs in the 2-3 years prior to the peak of a cycle. Mining Mega IPOs (those that raise in excess of A$1 billion) are rare and tend to be quite close to the cycle peak. The best historic example is the IPO of Glencore, which raised US$11B to list on the London Stock Exchange in 2011 within months of the peak of the hottest mining market for decades.

Figure 2 - Mining IPO activity versus the market (Source: supplied)

Transactions, COVID and the proverbial naughtier sibling

Large mining takeovers are also a useful cyclical indicator, and the Lion Clock shows these as the cycle moves from 10 to 11 o’clock. There is an expectation driven by the precedents of recent cycles that these sort of deals might be outrageously priced, or define new all-time crazy deal sizes to create much larger companies or for a major miner to strategically put its foot on a truly world class project.

Recent deals such as the mergers of Northern Star and Saracen, Endeavour and Teranga, or SSR and Alacer have all created companies that have leap-frogged rivals to move to higher tiers of gold producers, and they are great examples of the sort of paper takeovers that can occur at this point of the cycle, even if they lack (going on the very little amounts of hindsight that so far exist) outrageous pricing.

This begs the question: has the sector has become exuberant enough to justify being near a cycle peak ?

Anyone who’s behaviour was ever highlighted as an example of what not to do to their (usually younger) siblings know – halos are eventually dislodged, most often by the wearer. In 1997, the exposure of a massive fraud and false gold discovery at Busang in Indonesia not only led to the collapse of Bre-X Minerals, it brought about a seismic shift in sentiment toward miners. All at once, distrust spread across the market and miners were sold off as exuberance (which was abundant) was seen as a sign of certain rot. Miners were bestowed the unofficial title of ‘least reliable’ sector of the global equity market. Fortunately for miners, this was soon usurped by the technology sector following the dot-com bubble and bust.

The mining bust of 2011-15 has a great deal in common with the bust of 1997-99: miners were sold down against an otherwise buoyant equities market owing to (fairly well deserved) investor distrust toward the mining sector. But with no dot-com wreck, investors’ memories of financial recklessness in the mining sector from circa 2011 remain all too clear. Whilst miners can access abundant funding, the investment market still remains wary of deals that might not obviously create value.

The global proliferation of the COVID-19 virus may also have had an impact, as travel became restricted and borders closed sometimes on short notice. This must certainly have posed a challenge to due diligence for potential deals and might explain why many of the deals that have been completed in the era of COVID-19 have been more or less jurisdictionally confined.

Emissions targets versus takeover targets and the rush to be most responsible

Without an obstructive smoke screen of someone else’s poor behaviour (like a tech wreck), miners have needed to resort to outstandingly good behaviour in an attempt to restore some previous standing. The mining sector has embraced the broader equity market push toward greater transparency on Environmental, Social and Governance performance and most would agree the products of this are mostly welcome improvements.

It is however a little more than tongue in cheek to say that some miners need to work hard at this to restore investors’ confidence to the extent that they might one day conduct a large transaction because investors, like parents, are quite capable of punishing previous poor behaviour by withholding permission for a separate activity.

There was a significant clean out of the global mid-tier by a multi-decade consolidation drive that concluded in the 2000’s and as a result ideally sized takeover targets are scarcer than they have been in previous cycles. For now, it might just be easier for a number of miners to achieve emissions, gender balance or local employment targets than to identify a growth acquisition target that also justifies a value proposition significant enough to make it the focus of their investors.

Outlook: risks to liquidity

An oversupply of liquidity doesn’t cause a crash, but substantially reduces the need for miners to be fiscally responsible because excess expenditures can be readily funded. The longer liquidity remains high the greater the risk that a bust will take place, as a result of an adequate catalyst. History is extremely firm with this outcome.

Risks to commodity prices – many of which are close to all-time highs:

- Iron Ore: resumption of large-scale production out of Brazil.

- Battery materials: demand expectations fail (or is slow) to meet newly developed supply.

- Gold: interest rates increase to combat inflation.

Risks to financial performance of miners:

- Most indications are that financial behaviour of miners is regarded broadly as responsible, so mining sector exuberance is not yet a risk to the cycle.

Risk of inflation; interest rates versus asset values:

- Many large economies have limited ability to manage inflation (should it be reflected in measures) because of the risk to asset markets (eg US equity market, the Australian housing market), high government debt levels and risk to enterprises and individuals who leveraged themselves with cheap credit.

- The global equity market has surged in response to global stimulus and record low interest rates, and any substantial equity market correction would affect mining equities.

The greatest risk of a mining bust appears to be aligned with a general equity market correction in a similar fashion as 1987 or 2008.

Post script

The Lion Clock is a concept that was developed by Robin Widdup (founder of Lion Selection Group) in the 1980's whilst a mining analyst at JB Were. This concept has been refined, but little changed in over 30 years, and Lion update the clock when it spies the type of characteristics that betray a change in liquidity toward the mining sector. The commentary above is extracted from Lion's Quarterly report for the period ended 30 April 2021, which can be found here.

Leading Australian Mining media outlet, MiningNews.net published an article on 3 May 2021 where the prominent but anonymous commentator Dryblower ruminated on the mining cycle. Dryblower’s conclusion was very similar to our own, if justified differently.

"The Lion clock is not yet signalling crash, nor is it a finely tuned investment guide, but it can provide a useful early-warning signal about what comes next."

Drybower, Via MiningNews.net 3 May 2021

Four reasons to register for Livewire’s 100 Top-Rated Fund Series

Livewire’s 100 Top-Rated Fund Series goes live on 1 June 2021. Register now if you want:

- To get first access to a list of Australia’s 100 top-rated funds

- Detailed fund profile pages to help you compare performance, fees, and philosophy

- Exclusive in-depth interviews with expert researchers from Lonsec, Morningstar and Zenith.

- One-on-one videos and articles with 16 of Australia’s best fund managers

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

2 topics

1 stock mentioned

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

Expertise

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management