Microcap Managers Continue to Outperform ETF’s

We are half way through FY18 and microcap and small caps indexes have continued where they left off in Q1, and then some. Once again, microcaps significantly outperformed large caps. The S&P/ASX All Ordinaries Accumulation Index returned as you will recall a minuscule 1.0% for the Q1FY18. In stark contrast, the S&P/ASX Emerging Companies Index posted a robust 8.9% return for the Q1FY18 quarter. The Q2FY18 score card reads as follows the S&P/ASX All Ordinaries Accumulation Index returned a respectable 8,2%. The S&P/ASX Emerging Companies Index however continued to power ahead with a hefty 15,3% return for the quarter.

Stand Out Sectors

The returns from microcaps is not totally unexpected given that the top sectors in the S&P/ASX Emerging Companies Index, constituting just over 43% of the index are material and information technology. The sector weightings of these two sectors are much more pronounced in the S&P/ASX Emerging Companies Index compared to the S&P/ASX All Ordinaries Accumulation Index or the S&P/ASX 200 Accumulation Index. In the large cap indexes the financial sector dominates driven by the big 4 banks.

Both the materials and information technology sectors have been very much in vogue right across the market in the last 6 months. Hence, the performance of these sectors has been driving index and manager returns alike.

Fund Closures and New Additions

The second quarter of FY18 saw plenty of action in LIC microcap space. Towards the end of the quarter we saw the successful IPO listing of the Spheria Emerging Companies LIC (SEC:ASX) on the boards. We have added the LIC to our universe and will report on its performance going forward. We will also follow with interest the performance of this vehicle with the near identical managed fund vehicle offered by the same investment manager as an interesting case study over time.

Also, just before Christmas we saw Contango Microcap LIC (CTN:ASX) change its name to the NAOS Small Cap Opportunities (NSC:ASX) owing to CTN shareholders voting for NAOS Asset Management to take over as the investment manager of the LIC. This brings our LIC universe to 9. Interestingly, 7 out of the 9 Microcap & Small Cap Focused LIC’s were launched in the last 3 years.

On the managed fund side, we are also adding two new names to our fund universe.

The Peak Opportunities Fund is a particularly interesting in that it offers a style of investing not available in the microcap space currently. At least not as a fully dedicated strategy or mandate. I would best describe it as special situations investing or strategy. The fund participates in microcap ipo’s, placements, underwriting of rights issues, reverse takeovers and seeks to enter and exit these types of corporate actions at a profit. The fund celebrated its 1 year birthday at the end of 2017 and recorded a 39% return. An impressive first year.

The Prime Value Emerging Opportunities Fund is an active, high conviction and benchmark unaware vehicle. It seeks to invest in companies with sound balance sheets, good management and with solid growth prospects. The fund has just celebrated its 3 year birthday in October and has returned 14.1% annualised per annum since inception

Stand Out Manager Performances

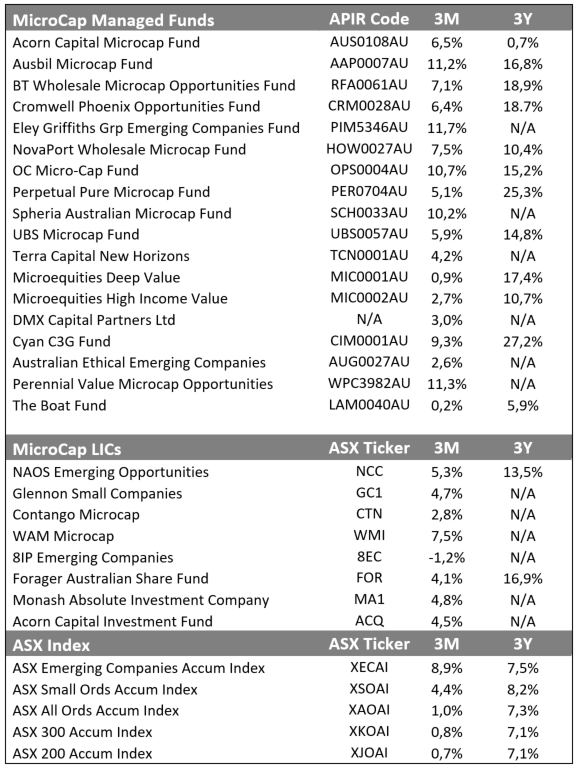

Stand out performances from the active managers in the quarter came from microcap vehicles managed by OC Funds Management, Wilson Asset Management and Acorn Capital. With Acorn’s LIC The Acorn Capital Investment Fund (ACQ:ASX) taking the blue ribbon registering a return of 19.4% for the quarter.

Most managers did manage to log double digit returns for the quarter which is not surprising given the strong performance of the index and the general equity market. However, the managers which lagged both the index and their peers for the quarter were The Boat Fund, MicroEquities and Naos. Now, my usual caveat applies, no investor should judge a manager on a single quarter performance no matter how positive or negative the performance was.

The table provided gives both the 3 month and 3 year returns for fund managers who have such track records. This gives some perspective on their longer-term performance and serves as a reminder to guard against reading too much into short term performance.

A passing glance, down through the list of the 3 year returns in the table below shows the majority of fund managers have outperformed both large and small cap benchmarks.

Microcap outperformance versus large caps and ETF’s

Over a 3-year time horizon, active microcap managers by and large have an excellent track record of delivering alpha to their investors They have also delivered superior returns versus that of the mainstream index funds and ETF’s. This evidence should be food for thought in investor’s overall asset allocation decision.

Stand out performers over 3 years continue to be Cyan, Perpetual and BT.

The Curious Case of the Microcap Benchmark

One of the most curious things about looking at the universe of microcaps mangers is the disproportionate use of the S&P/ASX Small Ordinaries Accumulation Index as the benchmark for the funds and performance fees calculations. No fewer than 15 of the 28 vehicles in our universe use this index as its benchmark.

Now some of the funds in our universe could be classed as small cap funds as they straddle the line in terms of the market caps of their holdings. This makes classification a bit of grey area. However, if we take the Perpetual Pure Microcap Fund for example you would think that it would use the S&P/ASX Emerging Companies Index as it benchmark given the name of the fund and its investment strategy and mandate? Yet, it uses the S&P/ASX Small Ordinaries Accumulation Index for its benchmark.

Indeed, just 2 funds in our universe actually use the S&P/ASX Emerging Companies Index as their benchmark.

Now, I am not saying one benchmark is better than the other but it is curious that so many funds use a benchmark which in name at least is perhaps not the most relevant or appropriate for the funds strategy and mandate. This is perhaps something investors current or prospective can query with the relevant managers to getter better understanding as to why one was selected over the other.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I focus on ASX listed microcap and nanocap stocks which is anything from $10mil to $300mil market cap and everything in between. This truly is the under-researched part of the ASX. My hope is to bring you interesting microcap stocks and news.

1 topic

3 stocks mentioned

I focus on ASX listed microcap and nanocap stocks which is anything from $10mil to $300mil market cap and everything in between. This truly is the under-researched part of the ASX. My hope is to bring you interesting microcap stocks and news.

I focus on ASX listed microcap and nanocap stocks which is anything from $10mil to $300mil market cap and everything in between. This truly is the under-researched part of the ASX. My hope is to bring you interesting microcap stocks and news.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

Morgans’ top large-cap picks for October 2025

Morgans Financial