Miners are Exploring again. It's 8 o'clock and Greed is Back

Resources equities have outperformed the rest of the market by a wide margin in the time since January 2016, when the long bust ended. This period has been marked by increasing investor interest in miners, and consequent increase in liquidity - investor funds flowing toward the sector.

In many small companies, exploration budgets need to be raised from the market, and are first to be cut when times get tough - so expenditure maps the availability of risk dollars to the industry. The strong rebound in investor interest in the sector has facilitated capital raising across the junior end, and a commensurate reinvigoration of exploration by all sizes of companies. Growth investment by the mining sector has re-started, and investors are rewarding growth and ascribing value to upside again. We have not seen conditions so supportive of highly speculative exploration concepts for many years.

Despite a supportive investor market, there are impediments that are likely to make for slow progress toward growth opportunities. Whole teams were lost and exploration ground dropped as work programs were ceased, so internal capabilities have to be rebuilt. A number of larger companies have supplemented internal growth options with investment into junior companies – sewing the seeds of future M&A.

Recent capital raising success positions the sector well to fund continued work, and furthermore, investors’ supportive response to positive exploration results indicates that the positive trend of expenditure is more likely to continue than not.

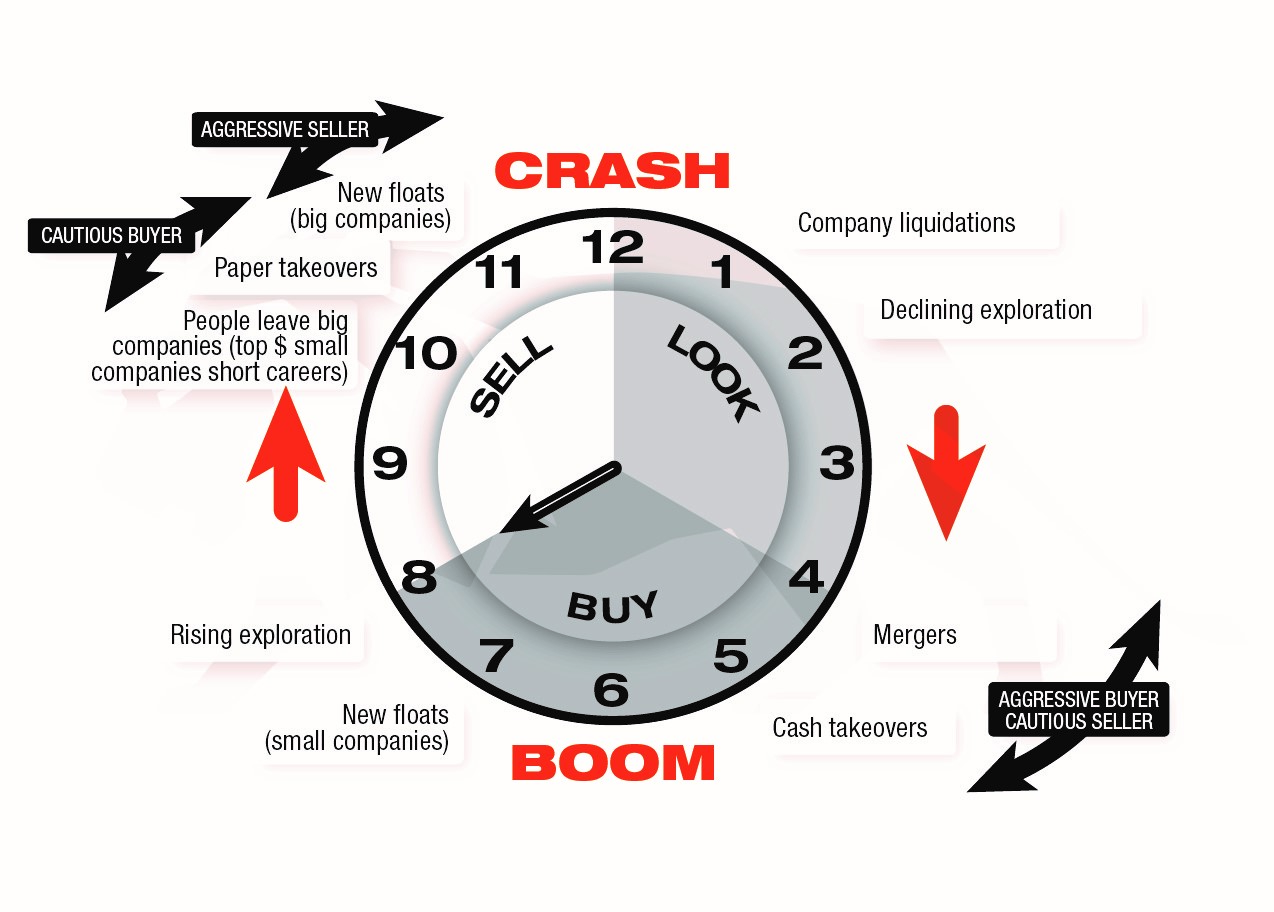

This is a clear signal of progressed sentiment in the sector – and so the time on the Lion Clock is now 8 o’clock.

Access the full report from Lion Selection here: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

3 topics

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

Expertise

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

Expertise

Comments

Comments

Sign In or Join Free to comment