Mortgage default rates are increasing, not decreasing, as implied by RMBS data

Being able to measure and monitor the true level of mortgage delinquencies across an economy is essential for investors and regulators interested in asset pricing and financial system stability, amongst other things. Prior to the 2008 global financial crisis, rising mortgage default rates in the United States were an important leading indicator of subsequent losses. Changes in arrears rates are also vital for the valuation of asset-backed securities sold via securitisation.

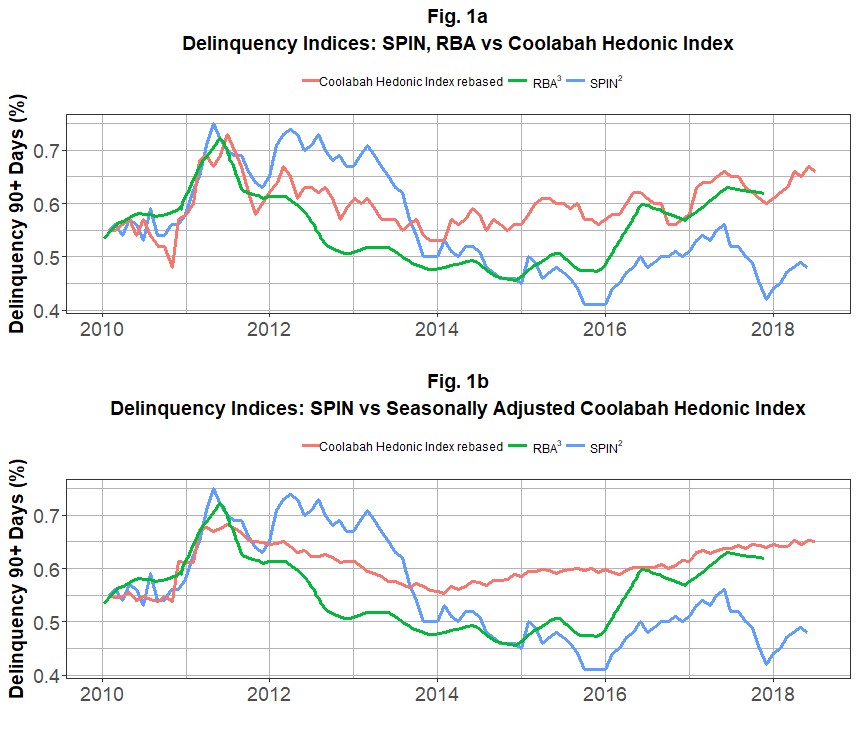

And yet public measures of mortgage default risk almost always use simple averages across pools of individual assets. In Australia, one such example is the Standard & Poor’s Global Ratings Mortgage Performance Index, known as the SPIN Index. These weighted-average or median measures of default rates are, like median house price indices, afflicted by severe compositional biases, which can lead to spurious inferences regarding the direction of default rates.

New residential mortgage-backed securities (RMBS) issues that are, for instance, added to the SPIN Index sample typically have no defaults in them. This is because a new RMBS deal will typically start with only performing home loans. That means that a significant increase in RMBS issuance, such as that which has occurred in Australia in recent years, can artificially reduce the SPIN Index’s reported arrears rate at a time when the true or underlying default rate is actually climbing.

There are other sources of potential bias with simple weighted-average or median default indices. Even if RMBS issuance patterns are constant over time, a change in the composition of the deals, such as a jump in the proportion of transactions with higher loan-to-value ratios (LVRs); less seasoned loan pools (i.e. portfolios with a lower weighted-average loan age); and/or borrower characteristics that have higher probabilities of default (e.g. tilts towards investment borrowers, interest-only borrowers, and/or sub-prime borrowers) can result in a simple weighted-average or median mortgage default index producing misleading results.

To address this problem, we have developed the first known hedonic regression-based indices of mortgage default risk that explicitly control for compositional biases through the models’ characteristic-based independent variables, which include the time since the RMBS transaction was consummated, the weighted-average age of the loans, and the weighted-average LVR, amongst other factors.

Whereas the SPIN Index suggests that default rates across Australian RMBS transactions have declined in recent years, which has been used in many issuers’ marketing materials to promote the security and safety of these deals, our hedonic mortgage default index implies exactly the opposite: that is, compositionally-adjusted default rates on Australian RMBS deals have, in fact, been increasing sharply in recent times (see Figure 1).

While this finding conflicts with the claims of credit rating agencies that monitor RMBS default rates, it reconciles closely with the arrears rates reported by the Reserve Bank of Australia (RBA), which tracks the performance of all bank balance-sheet loans (as opposed to just the sample of RMBS issues), and the higher impairments disclosed by Australia’s biggest banks. Indeed, our hedonic mortgage default index correlates closely with the RBA’s published mortgage default series, which makes sense given that the RBA data is not impacted by biases induced by the frequency of RMBS issuance (see Figure 1).

Another finding is the presence of strong seasonality in mortgage default rates, which we quantitatively address via the application of seasonal-adjustment methodology. To the best of our knowledge, the SPIN Index is not currently seasonally-adjusted.

Going forward, we would encourage researchers to develop and use hedonic techniques when studying mortgage default rates afflicted by compositional biases. And we believe that there are many ways to extend the simple hedonic models outlined in this paper to further enhance the accuracy of the insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha Managers” based on his risk-adjusted performance throughout his career across. He previously worked for Goldman Sachs in London and Sydney, the Reserve Bank of Australia, and founded the award‐winning research/investment group, Rismark. He has regularly advised governments, developing unique policy proposals. Chris graduated with the University Medal (Economics & Finance) from Sydney University. He studied in the PhD program at Cambridge University in 2002/03, leaving to set up his funds business.

4 topics

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Chris co-founded Coolabah in 2011, which today runs over $8 billion with a team of 40 executives focussed on generating credit alpha from mispricings across fixed-income markets. In 2019, Chris was selected as one of FE fundinfo’s Top 10 “Alpha...

Expertise

Comments

Comments

Sign In or Join Free to comment