NZ tech punching above its weight

Some wonderful examples of entrepreneurial drive and global innovation can be found in the burgeoning New Zealand startup community and emerging listed companies. Here we share our thoughts on the scene following a recent trip, and update on Xero as well as an earlier-stage NZ tech success story.

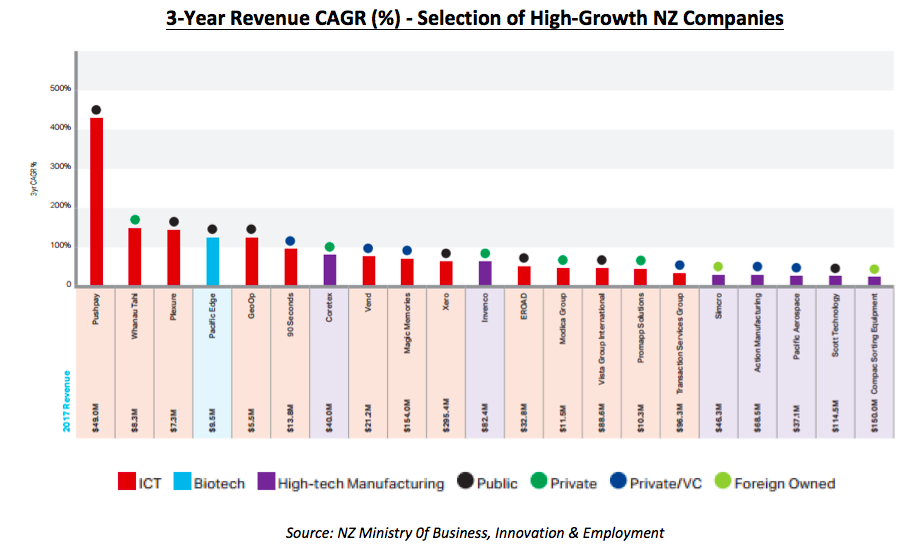

NZ's third largest export: Technology

While we focus on publicly-listed companies on the NZX, we can only be impressed with the speed in which New Zealand’s start-up community has rapidly developed into a globally relevant destination for local and international venture capital.

According to a recent report from the NZ Ministry of Business, Innovation and Employment, more than NZ$875m in capital was raised in 2017 by New Zealand-based businesses across the private equity and venture capital space.

Early stage capital commitments tend to favour higher-growth opportunities and it has been the burgeoning Kiwi tech sector that has proven to be the key attraction for foreign capital in recent years.

From barely rating a mention only a decade ago, technology now sits as the country’s third largest export (behind tourism and the dairy industry) with the NZ tech industry contributing over NZ$10bn in combined revenue in 2017 and employing more than 40,000 people.

Source: NZ Ministry 0f Business, Innovation & Employment

No event could perhaps be more symbolic of the heights to which the emerging and start-up environment in New Zealand has reached than the pending first commercial rocket launch from NZ-based start-up Rocket Labs – expected sometime toward the end of June this year. Started in 2006 by New Zealander Peter Beck as a company focused on developing smaller, lower-cost satellites for the telco, mapping and space research industries.

The business has developed a pilot rocket (in their manufacturing site in Auckland) entirely powered by engines that are constructed by 3D printers that are expected to provide customers with the opportunity to deliver smaller commercial payloads into orbit. With the business already commanding a private valuation in excess of US$1bn prior to achieving first revenues, the potential for the business to meaningfully grow from here is enormous. Keeping true to their New Zealand heritage, the launch of the company’s 17-metre tall ‘Electron’ rocket won’t occur at the more familiar launch pads of Cape Canaveral or Kennedy Space Centre, but from a private launch site in the Hawke’s Bay on New Zealand’s North Island.

From Xero to Hero

We wrote about Xero on Livewire in 'From Xero to Hero' back on August 10th 2017. Livewire reached out to us recently noting the 65% gain in the stock price since the wire, and asking us for an updated view on the company. Our visit has provided us an ideal platform with which to do this.

While no longer NZX-listed, cloud accounting software developer Xero (XRO), for example, has continued to experience a terrific rate of growth as their global sales strategy begins gains momentum.

From humble beginnings in founder Rod Drury’s Wellington apartment in 2006 (the business didn’t operate from a formal office premises until 2007), the company now commands a NZ$6bn market capitalisation with over 2000 staff worldwide and 1.4m subscribers across 180+ countries. In its breakout year in 2008, the firm was thrilled to announce to shareholders annual total revenues of $134,000 – ten years later and the business now generates over $100,000,000 a quarter.

While the business is no longer a ‘small cap gem’ lying undiscovered across the Tasman, the considerable market capitalisation of the business isn’t symbolic of a business that has reached peak growth, in fact far from it. While the initial core markets of Australia and New Zealand are certainly maturing (i.e. they are still experiencing overall growth however the rate of that growth year-on-year will slow from here), the business at a group level will still record overall subscription growth for FY18 in the order of ~30%, with a similar amount of growth expected for the 2019 financial year.

Expansion into global territories will be the primary driver of growth from here, given the business remains in the early stages of market penetration in the much larger US and UK markets. The UK experience, in particular, has been highly encouraging to date with subscriptions to Xero’s product growing +47% on the prior year. We expect to see a continued acceleration in net subscription additions (i.e. growth increasing at an increasing rate) as market share increases and overall brand awareness expands.

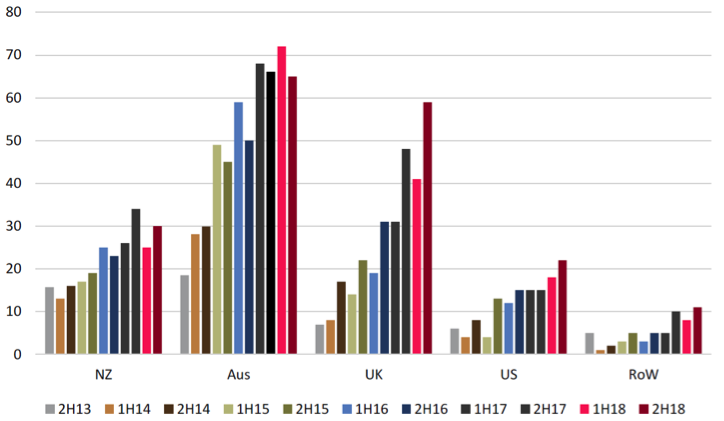

Xero Net Subscriber Additions by Geography (‘000’s)

Source: Evans & Partners

Pleasingly, the business looks set to benefit from some regulatory tailwinds in the UK in FY19 that will require all businesses with revenue >£85,000 to lodge tax returns electronically. While the overall impact at this stage is hard to quantify, we are reminded of the incredible surge in license sales experienced by Australian accounting software provider MYOB through the 1999-2000 period following the announced introduction of the GST in July 2000. Winning the UK, in our view, will be critical for the business on a five-year view as it essentially provides a sound capital base to then attack and grow into more international market opportunities – potentially Canada, Singapore, South Africa and Malaysia.

Perhaps more importantly, the business has now reached the crucial stage of moving from loss making to first profitability, effectively enabling future organic growth to be funded by its own free cash flows. While the journey has taken ten years to reach cash flow breakeven, the subsequent uplift in equity value of the business over the period again provides a wonderful example of the incredible competitive advantage that businesses with a supportive shareholder base enjoy. Sacrificing near term profit or dividends for longer term growth optionality hasn’t historically been an easy sell for Australian or NZ-listed management teams and it is encouraging to see shareholder patience being acutely awarded.

Pushpay: Pushing higher

Fellow listed Kiwi tech player Pushpay Holdings (PPH) has provided us with another fantastic example of entrepreneurial grit and innovation from the Land of the Long White Cloud. The mobile payment technology business (focused primarily on the church-giving and charity sectors) announcing this month a more than doubling of revenues to US$70.2m over the year while average revenue per customer increased +36%.

This is a terrific achievement for a business that had its genesis only in July of 2011, where co-founders Chris Heaslip and Eliot Crowther shifted their own paid work commitments to work nights in order to focus on the development of their mobile payment application idea during the daylight hours. Fast forward seven years and the business stands as a dual-listed public company with market capitalisation in excess of $1bn processing more than US$3bn in annualised payments across the platform they created.

Faith-based giving (i.e. donations from individuals to their respective churches and/or charities) across primarily New age Christian churches' congregations in the United States has provided the bulk of the growth to date, with the Pushpay platform now being utilised across 54 of the top 100 largest churches in the US. Religion is an enormous business in the US, with the faith sector processing well in excess of US$120bn in donations across 340,000+ churches each year - a thematic we expanded on some time ago when we first highlighted the business to investors.

In a similar vein to Xero, the business is shortly approaching its own ‘second act’ of the growth story, with the company expected to reach monthly cash flow breakeven by the end of calendar year 2018. While dual-listed currently on both the New Zealand and Australian stock exchanges, the business has also flagged the likelihood of listing on a North American stock exchange by the end of the calendar year in order to further broaden the capital and shareholder base. With 97% of customers located in North America (in addition to 258 staff), the move seems a logical next step for the business and we look forward to the next stage of growth from Chris and the team.

--

Contributed by Ophir Asset Management from the May Letter to Investors

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

1 topic

2 stocks mentioned

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment