On the Oil Rollercoaster

The oil price has been on a rollercoaster for the past five years. From the depths of US$28 per barrel in early 2016 the price rose to US$85 per barrel last October. Things seemed to be going well for oil producers and service providers. But it was short lived. Oil is now trading closer to US$54 per barrel, down more than a third in a few months. It’s also been a wild ride for the Fund’s oil exposed investments. So where to now?

There has been plenty of oil related news to keep track of over the past year: Iran sanctions, OPEC and Russia turning on the taps (then getting ready to turn them off again), Trump’s many tweets, rising US interest rates, trade disputes, and even more tweets. Throw it all together and you get plenty of oil price volatility.

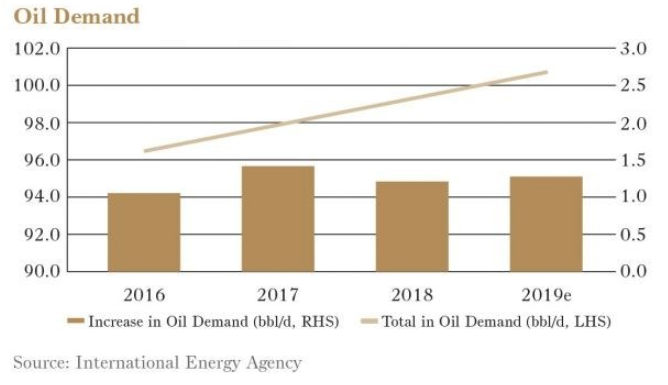

World oil consumption is still set to increase by 1.4 million barrels per day in 2019. The US, now the world’s largest oil producer, is pumping furiously but an agreement by the Organization of the Petroleum Exporting Countries (OPEC), plus Russia and others, will remove 1.2 million barrels per day of supply from the market. All told, expectations are now for oversupply to switch to undersupply by the second quarter of 2019.

Price stability critical

This should help the oil price. But the Fund’s oil investments are not oil producers.

Instead our investments are in two offshore oil service providers. They need a steady supply of offshore oil exploration and development spending, not another couple of dollars on the oil price.

A steady supply of spending is more likely to come when prices are reasonable and, importantly, stable. Price stability would lead to confidence. Confidence would lead to spending. And spending would lead to more work for Matrix Engineering (MCE) and MMA Offshore (MRM).

Before the recent fall in oil price we were starting to see some confidence returning.

Matrix, the oil and gas equipment provider, announced its first large new contract win in three years. The company will provide its main riser buoyancy product to two drillships, replacing aging buoyancy. The company also noted an increase in quotation activity for other jobs.

Many offshore rigs have been parked on the sidelines and riser buoyancy replacement has been low on the list of capital expenditure priorities for rig operators. With rigs returning to work though, there should be plenty of replacement buoyancy needed after years of underspending. New rig orders, while still slow, may also increase. The revenue potential is substantial if orders resume. And the costs are largely fixed.

Alongside the contract win Matrix raised $3m in new equity. The Fund participated, raising our ownership in Matrix to 15% of the company.

MMA Offshore was also showing some signs of making better use of its fleet of offshore support vessels. The company told its annual general meeting in November that the utilisation of its fleet had been 79% during the year. More work would mean MMA would be able to put even more vessels to use and, eventually, raise the rates it charges.

The company is on track to be cash flow neutral for the current financial year, which would be a good achievement for a business that has struggled with losses for years. It last traded at $0.15 per share, a 61% discount to the $0.38 per share value of its vessels.

Neither company had seen the benefit of the high oil prices in mid-2018—mostly because they weren’t high long enough to encourage more offshore oil spending. So lower oil prices now are unlikely to impact shorter-term performance much.

Longer term, stabilisation of oil prices, even at levels a little above today’s prices, would mean offshore oil producers could stop worrying about prices and start worrying about spending capital to grow oil production.

Further Insight

If you are interested in receiving the here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

.jpg)

2 stocks mentioned

.jpg)

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

Expertise

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management