Our Top Dividend Pick

So far 2018 has begun just as 2017 finished, with the established ‘more mature’ businesses, as categorised by the ASX top 20, underperforming their smaller cousins. Typically, these larger more mature businesses are synonymous with stable dividends and income, naturally luring those investors whose stage in the investment lifecycle preferences income over growth.

As a general rule we believe the greatest shareholder value is created by those businesses who have high returns on equity and management teams who chose to reinvest the earnings back into the business. Essentially dividend payments can at times be viewed as sacrificing future company growth in favour of immediate gains in the form of income.

We nevertheless understand that some investors require dividend income to live off day-to-day, and the prospects of waiting years for a business’s growth strategy to deliver outcomes simply isn’t a practicable option.

In the present environment of falling share prices for banks, insurers and telecommunications, many of the traditional ‘go-to’ dividend favourites are heaping pressure on many investors portfolio valuations. The fact is the habitual preference for some of these well-known businesses, although familiar and marketable, can be counterproductive to investment performance.

Looking for Alternatives

Scanning across the market and looking deeper into some of the alternatives available to investors, one can identify opportunities that provide a commensurate if not superior dividend yield, in some cases with less risk and lower price volatility.

At Medallion Financial we feel it’s important to ensure we don’t let hubris emerge in our investing. We understand that markets can be unpredictable and investment managers like ourselves can go through periods of great success as well as leaner periods. For that reason, allocating a portion funds towards high quality Listed Investment Companies (LIC’s) with a proven track record can allow our clients to diversify their risk as well as boost income.

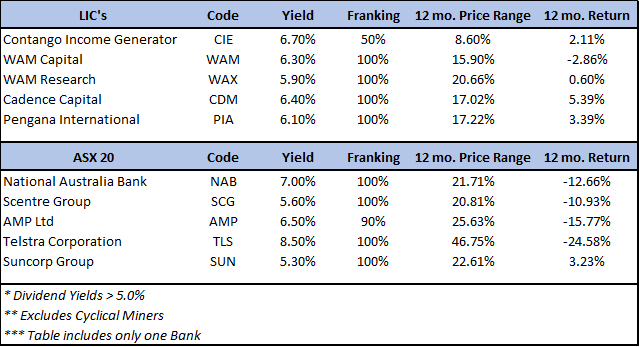

One such LIC that we feel offers an attractive entry point at these levels is the Contango income generator (ASX: CIE). The Contango income generator is a listed investment company that in our opinion offers investors an alternative yield option to the more traditional yield players such as the banks, telecoms and REITS.

The underlying CIE portfolio comprises of investments in high yielding ASX listed securities that fall outside the largest 30 securities in the ASX 300. As such this LIC can provide an attractive counterbalance for those portfolios that have become overexposed to ASX top 20 business over the years, by providing a more diversified income stream while at the same time potentially reducing the overall risk profile of the portfolio.

The current CIE price of 96.5cps represents a discount to the most recently reported pre-tax NTA per CIE share of $1.01 as at 28 February 2018. Based on a CIE share price of $0.965 and maintaining the current distribution policy (assuming 50% franking), the income return to investors is estimated to be 6.7% over a 12-month investment horizon before franking.

The underlying share price has historically traded in a very narrow band with a one year high and low of $1.01 and $0.93 respectively. With relatively low volatility in an otherwise increasingly volatile market, CIE can provide investors with a diversified high yielding exposure without the same price risk associated with individual stock positions. For instance, when you look at the NAB, although the dividend yield is an attractive 6.9% (100% franked) the share price has oscillated within a 21.5% range over the past 12 months. This highlights the point that investors searching primarily for income may be better served identifying LICs that can reduce price fluctuations all whilst maintaining income levels.

Our Top Dividend Pick

For those investors preferring an individual stock exposure, investors in our opinion should be looking to invest in those businesses that are growing dividends overtime to maintain the purchasing power of those dividends. The reality is businesses that are growing earnings and cashflows have the best chance of delivering dividend per share growth, a reality that many of the larger ASX 20 businesses have struggled with in recent years. One small but mature business we think meets the criteria and is worth consideration for a yield hungry investor, is Shriro Holdings (ASX: SHM).

Shriro is involved in the distribution of kitchen appliances, fixtures and consumer products throughout Australia and New Zealand. The company distributes and markets brands including Casio, Omega, and Everdure, among others, for products ranging from stoves and ovens, to watches and calculators.

Shriro has developed relationships with a number of renowned chefs and identities’, such as Neil Perry and Heston Blumenthal to help market their products and drive sales through retailers such as Harvey Norman, Bunnings and Winning Appliances.

As it stands, the domestic business is mature, however the company is pursuing growth as it expands into the US and Europe with positive early signs emerging. The Everdure BBQ brand is targeting a 1% market share in the US and German BBQ markets respectively, which has the potential to increase company earnings as well as dividends significantly.

The company is being priced by the market as a highly mature business with little growth prospects, trading on only 9.0x earnings and paying an 8.1% fully franked dividend. This indicates to Medallion that the market is underappreciating the potential growth profile and investors at these prices are essentially getting a free option on the growth side of the business should the expansion into the US and German BBQ markets deliver as management hope.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets