Outlook 2018: Developed markets looking expensive

The year of 2017 was the year of the structural winner, with the market led higher by the digital platform “FAAMNGS” (the acronym keeps extending as the list of perceived winners broadens) and the stylistic domination of Growth. Disruption was never more topical with nothing appearing more disruptive than crypto-currency euphoria. 2018 may be the year when central banks finally reconsider the wisdom of “inflation targeting” and savers revolt.

Globally, central banks have accumulated approximately US$20 trillion of sovereign bond assets via quantitative easing programs against total global GDP of US$90 trillion. If central bank targeting of low long dated real yields has been the lever lifting long duration assets, then the lever is now slowly reversing.

Over the quarter, the European Central Bank announced a reduction in its bond purchase program, the Bank of England hiked interest rates and the Federal Reserve hiked in December. Furthermore, Asian central banks are on the move with Bank of Korea hiking interest rates and robust economic growth in Malaysia, Thailand, and India pushing those central banks towards normalisation.

By kicking the proverbial can down the road, central banks have somewhat cornered themselves. Increasingly, political and economic pressure to normalise interest rates or withdraw stimulus is likely to trigger volatility and widen credit spreads. Our analysis suggests that U.S. high yield, or junk bond issuers are most vulnerable to this risk. While the low-volatility regime may endure, investors have grown too comfortable with the central bank reaction function, extending the illusion of stability.

Regional & Sector Return Expectations

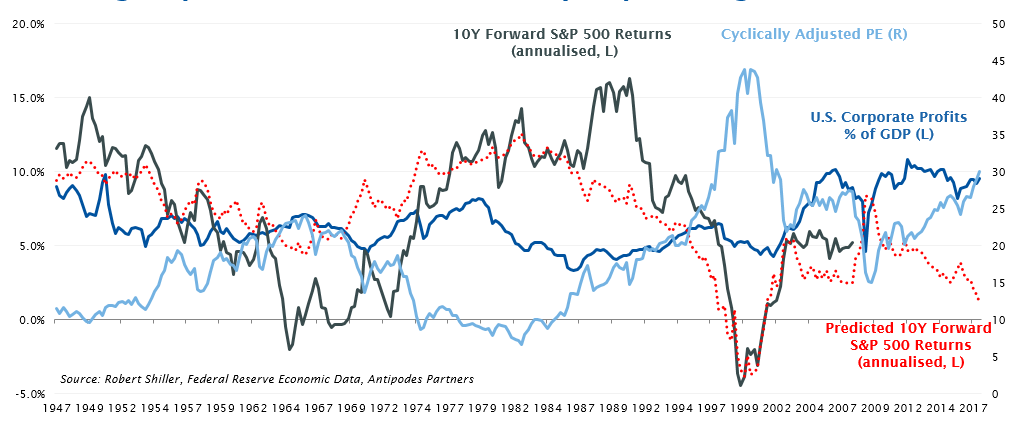

We find it useful to examine the long-term empirical data in terms of what starting multiples imply for expected future returns. Given broad differences in the timing of earnings cycles across both regions and sectors, we prefer to measure broader expectations for future returns based on “Cyclically Adjusted PE” (CAPE) valuations.

Antipodes’ structures its analytical efforts to get the most out of BOTH industry sector (globally oriented businesses) and geographic (domestically oriented businesses) context.

For the purposes of assessing the valuation of equities more broadly versus other assets, the best data set is country based, as the pricing of cash and bonds will be heavily driven by domestic considerations. With data back to 1947 and the greatest longevity of record, we can observe a strong relationship between the S&P 500 CAPE, U.S. corporate profit share as a % of GDP as a proxy for U.S. profit margins (which effectively applies a “structural” adjustment to the CAE) and ten year forward S&P 500 returns. A high CAPE is typically associated with lower forward returns, though this relationship is tempered when profit margins are low and the probability of the market growing into its multiple increases.

CHART 1: Relationship between the S&P 500 C.A.P.E., U.S. Corporate profit share and 10-year foward returns

Chart 1 captures this thought process. Given the timeframe of the forecast, it has little relevance to timing shorter-term market moves. However, taking a long-term view, with U.S. corporate profit share at a near peak of ~9.5%, and the CAPE approaching a 15 year high of 30x, the historical pattern implies relatively modest ~1.5% p.a. forward returns, significantly lower than the long-term average.

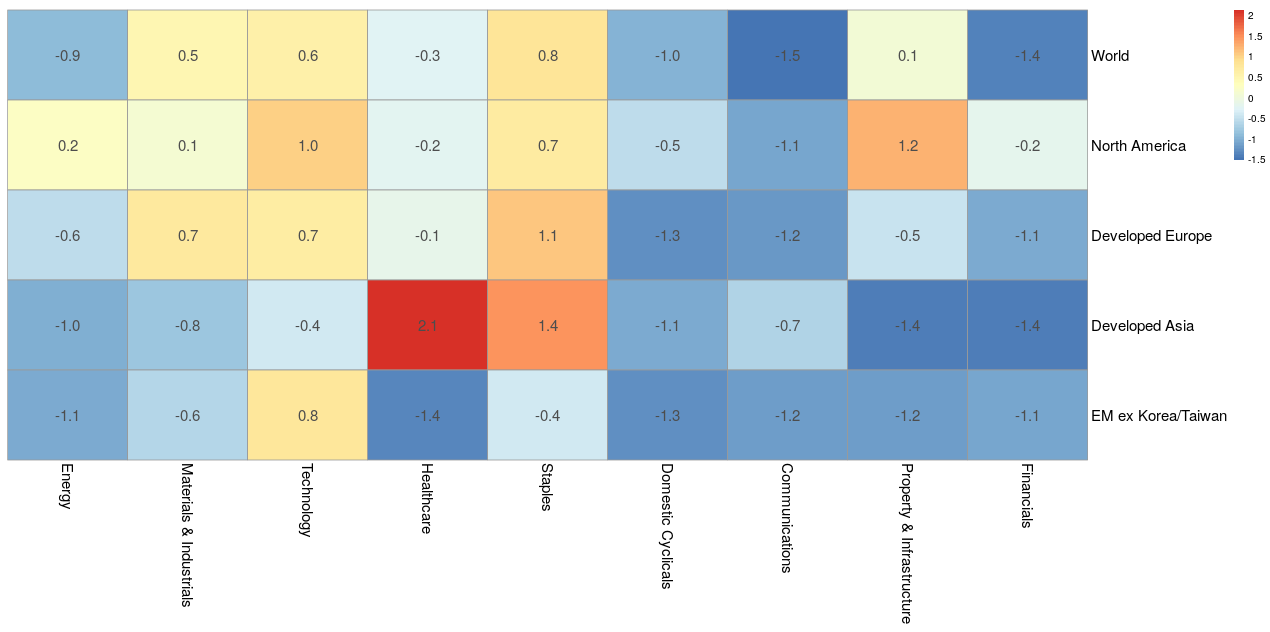

The question then becomes, if U.S. equities empirically appear expensive, what does the global, regional and sector picture look like? We refer to our valuation heat map (Chart 2), by adopting the U.S. as our benchmark for absolute return expectations, broadly both North American and Developed European equities look expensive (shaded yellow to red). Given these regions represent ~76% of the MSCI ACWI, based on our analysis, investing in the global index is unlikely to lead to a great long-term return outcome, rather both Developed Asia (Japan, Korea and Taiwan) and the Emerging Markets (EM) stand-out as the regions with the greatest return potential (shaded light to dark blue).

CHART 2: Region-sector valuation heat-map - EV/Sales relative to World – Z-Score (1995-2017)

Source: Antipodes Partners

We would stress that much of the difference in regional return expectations is driven by compositional differences in industry exposures. From an industry perspective, despite growing nationalism/populism, globalisation has resulted in valuation multiples that are relatively similar within industry sectors across regions. In this sense, we broadly observe:

- As the broad relief rally in China growth sensitive equities has played out over the past two years, Materials and Industrials outperformed and, though Energy rallied late in the year, it remains very cheap by historical standards.

- Though Financials significantly outperformed in the first half of last year, the sector remains cheap by historical standards with sentiment and profitability expectations weighed down by macro-concerns, low rates and yield curve compression.

- Domestic Cyclicals are also cheap by historical standards, especially strong incumbent retailers where the market is potentially underappreciating the brand equity and/or overlooking a successful adaptation to an online reality.

- Interestingly, in a market that until recently was paying-up for yield exposures, most intensely reflected in the Infrastructure sector, traditional yield sectors such as Telecommunications have experienced a significant de-rating.

- While Technology appears expensive on a more structural view of valuations, we guard against comparisons to the 1999/2000 tech bubble – Growth as a style is currently pervasively expensive across the global market, not just in Technology. While real structural change (cloud, social, virtual reality, media streaming, big data, autonomous driving, etc.) has underwritten the outperformance of the sector, conversely, certain risks are building for the Titans of Tech, including:

- Tax and regulation as increased scrutiny from governments around the world due to their size, influence and role in society, particularly around managing sensitive information.

- Intensifying competition whether it’s Amazon and Netflix competing on content streaming, or Amazon’s Alexa threatening Google’s core search business with its voice search capabilities, the titans are bumping heads. Likewise, Google is encroaching on Apple by focusing on its own smartphones and Microsoft is attacking Amazon’s AWS cloud business with its successful Azure platform. Related to this is the growing capital intensity of many of these businesses as the move towards cloud and video streaming requires heavy infrastructure investments.

- Style/Macro risk represented by excessive crowding by investors that have paid-up for structural growth where the current cyclical rebound in global growth forces long-term global interest rates higher triggering a rotation out of expensive longer-duration growth exposures into out of favour cyclical stocks.

- Consumer Staples were the expensive defensives, once enamored for their perceived profitability and growth characteristics, have now underperformed since the beginning of 2016. However, they remain one of the most expensive Developed Market sectors and in many cases structural pressures, such as substitution by private label, are intensifying.

- Healthcare has underperformed to the point that relative value has appeared. However, broadly healthcare related businesses will continue to be pressured by the public and governments grappling with affordability given decades of high industry cost inflation.

Conclusion

At the core of our investment philosophy we seek in our long investments both attractively priced businesses (margin of safety) and investment resilience (characterised by multiple ways of winning), with the opposite logic applying to our shorts, i.e. no margin of safety and multiple ways of losing. While the investment case will always be predicated on idiosyncratic stock factors such as competitive dynamics, product cycles, management and regulatory outcomes, we seek to amplify the investment case by taking advantage of style biases and macroeconomic risks/opportunities.

The general uptrend in the broader equity market seems set to continue given economic data globally remains robust and central banks very accommodating. However, the blind assumption of unendingly low rates is a dangerous one. We’re seeing interesting opportunities in businesses that would be characterised as more cyclical rather than structural/longer duration growers and are avoiding/shorting the expensive low-quality versions of the bond proxies and growth stocks. Furthermore, we’re encouraged by the growing valuation dispersion within and across markets (region/sector/factor) as we think this is indicative of broadening pragmatic value opportunities, both long and short.

For further insights from Antipodes, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Jacob Mitchell is Antipodes’ chief investment officer. He is an award-winning fund manager, with more than 25 years' experience investing in equity markets. Jacob founded Antipodes in 2015 after deciding to leave Platinum Asset Management where he spent 14 years and worked as deputy chief investment officer and a portfolio manager of the flagship Platinum International Fund.

Jacob holds a Bachelor of Commerce from the University of Western Sydney.

4 topics

Jacob Mitchell is Antipodes’ chief investment officer. He is an award-winning fund manager, with more than 25 years' experience investing in equity markets. Jacob founded Antipodes in 2015 after deciding to leave Platinum Asset Management where he...

Expertise

Jacob Mitchell is Antipodes’ chief investment officer. He is an award-winning fund manager, with more than 25 years' experience investing in equity markets. Jacob founded Antipodes in 2015 after deciding to leave Platinum Asset Management where he...

Expertise

Comments

Comments

Sign In or Join Free to comment