Price is what you pay... Value is what you get

Marcus Tuck

Mason Stevens

As Warren Buffet put it best: “Price is what you pay. Value is what you get”. And just as an individual share price can be disaggregated into earnings per share (EPS) times its PE ratio, the same thing can be done at a market index level - as we discuss here.

Valuing the US market

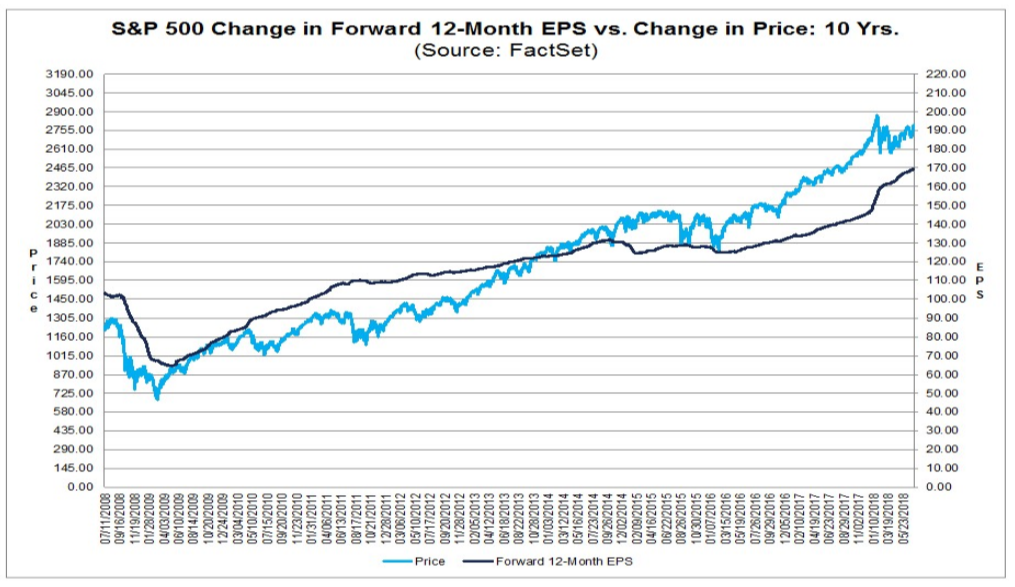

The S&P 500 Index level of around 2,810 can be disaggregated into 12-month forward “index EPS” of around 169 index points times the 12-month forward PE ratio of 16.65. The long-term upward trend in share markets is largely due to the trend growth in EPS over time as the economy grows, as can be seen in the FactSet chart below. Occasionally though, during recessions, index EPS can fall quite sharply.

The PE ratio applied to index EPS rises and falls in response to changes in interest rates and inflation. It is more “mean reverting” than index EPS, but can reflect structural shifts in the event that inflation and interest rates are sustainably lower than in the past.

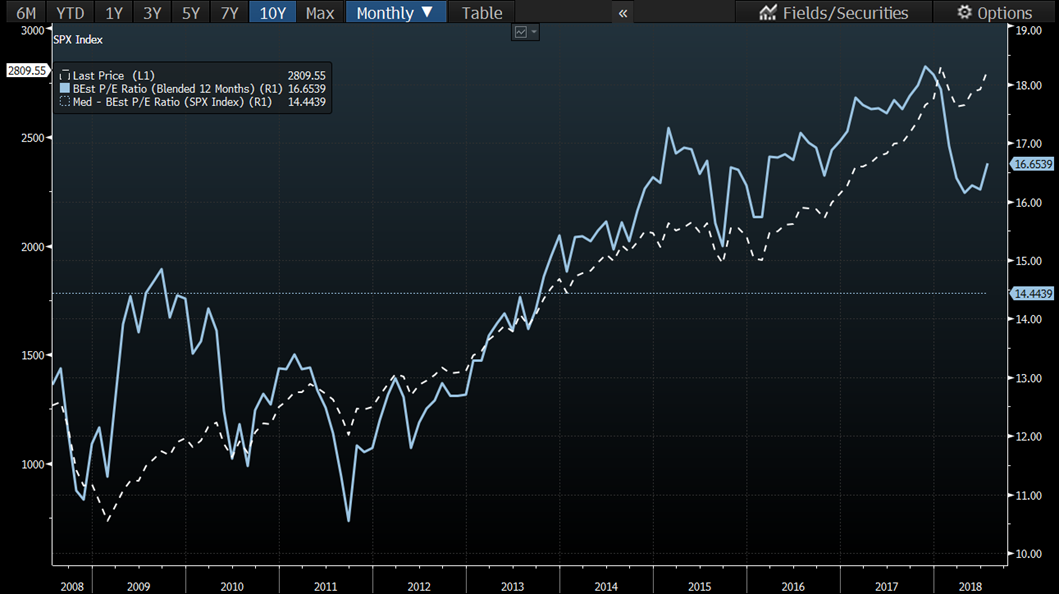

The 10-year history of the 12-month forward PE ratio for the S&P 500 Index can be seen in the chart below. The current reading of 16.65x is above the 10-year median of 14.4x and the 5-year median of 16.2x. However, it has come down from its recent peak of 18.3x in November, even though the S&P 500 Index is almost back to its previous high. That is because earnings are moving higher.

Source: Bloomberg

The absolute level of the PE ratio is still high though, but is it unreasonable? It went much higher during the dot.com era, peaking at over 25x towards the end of 1999.

A high forward PE ratio in isolation conveys some information but not as much as when the risk-free rate is incorporated into the valuation measure. That is because low bond yields help sustain high equity valuations.

The Equity Risk Premium (ERP) is a useful yardstick of equity valuation because it takes into account the prevailing level of interest rates. The ERP is the premium that equity investors require to compensate them for taking on the higher risks inherent in equities compared to bonds.

Historically, when the ERP drops below 2%, as was the case on the eve of the Global Financial Crisis in 2007, it is a sign that equities are expensive relative to bonds, and that a bear market could be imminent. The ERP can be calculated by converting the 12-month forward PE ratio into an earnings yield, and then subtracting the risk-free rate (the 10-year Treasury yield).

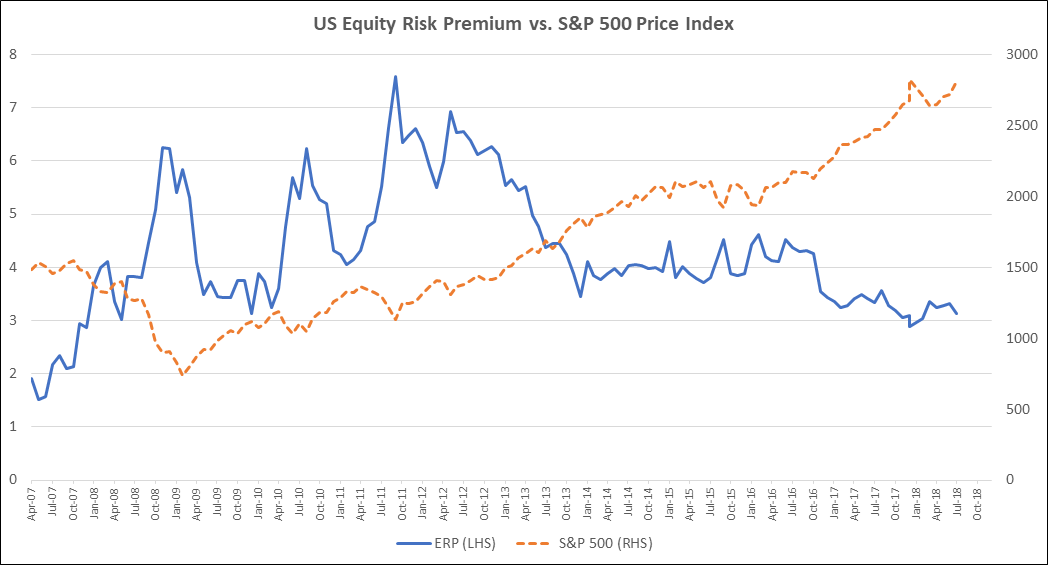

With the 12-month forward PE ratio for the S&P 500 currently at 16.65x, that equates to an earnings yield of 6.01% (i.e. 100/16.65). After subtracting the US 10-year Treasury yield of 2.87%, that gives an ERP of 3.14%. At that level, the ERP is consistent with a fully valued equity market but not a dangerously overvalued one. An ERP in the 2% to 3% range could be considered as flashing an amber signal; under 2% a red danger signal. The US ERP briefly dipped below 3% at the market peak in January (see chart below).

Source: Bloomberg, IRESS, Mason Stevens

With the US 10-year Treasury yield showing signs of stabilizing below 3% recently, that is a positive sign for the ERP and the PE ratio. As long as earnings continue to march higher, and the PE multiple does not contract substantially, the equity market can continue to advance.

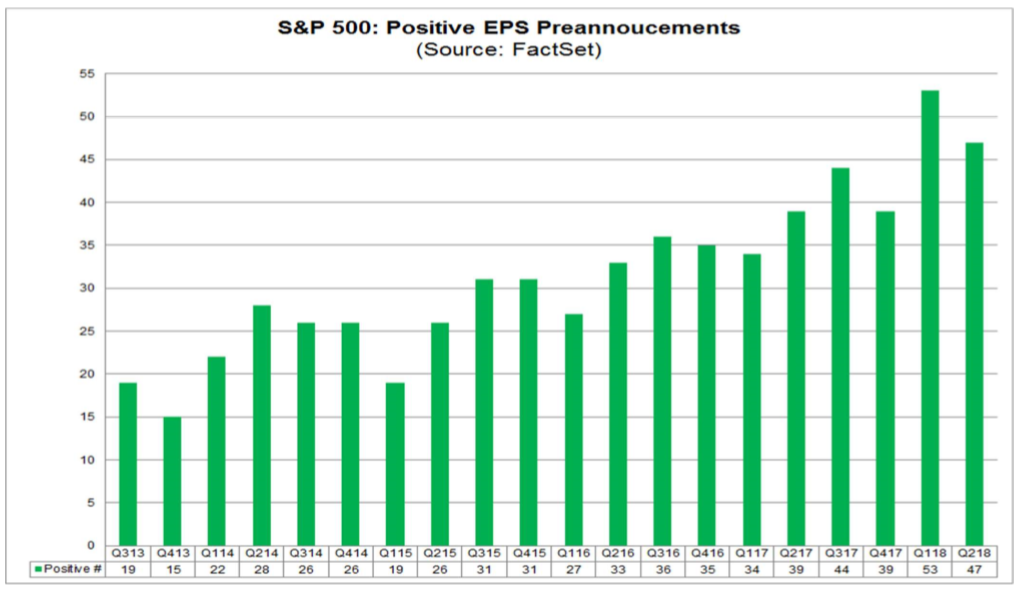

The current US reporting season for the June quarter is expected to deliver somewhere around 20% year-on-year EPS growth, boosted by the US corporate tax cut, healthy global economic growth, and record amounts of share buybacks.

An early positive sign for this reporting season is that we have already seen the second-highest number of S&P 500 companies issue positive EPS guidance since FactSet began tracking this data in 2006 (see chart below). The highest number was recorded in the previous quarter (Q1 2018).

A recession or substantially higher bond yields could derail the equity market’s progress. One or the other will happen at some point, but neither look imminent. For now, the equity market’s “wall of worry” is still there to be climbed.

--

This article is prepared by Mason Stevens Limited (Mason Stevens) ABN 91 141 447 207 AFSL 351578 and is general advice only and does not take into consideration yours or your client’s personal objectives, financial circumstances or needs and should not be relied upon as personal advice. You should consider this information, along with all of your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Securities, by nature, rise and fall and as a result investing in securities including derivatives involves risk. Past performance is not a reliable indicator of future performance and may not be achieved in the future. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.

Mason Stevens ensures that the information provided is accurate and complete but does not warrant its accuracy or reliability. Opinions and or information may change without notice and Mason Stevens is not obliged to update you if the information changes. Mason Stevens and its associated companies, authorised representatives, agents and employees exclude to the full extent by law, liability of whatever kind, including negligence, contract, fiduciary duties or otherwise, to investors or anyone else in respect of any loss or damage, including indirect or consequential loss or damage, foreseeable or not, arising from or in connection with this information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

2 topics

Marcus Tuck

Head of Equities

Mason Stevens

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

Expertise

Marcus Tuck

Head of Equities

Mason Stevens

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

Expertise

Comments

Comments

Sign In or Join Free to comment