Pricing growth: Why simple doesn't work

In the twelve months to Monday of this week, the S&P500 index is up 15.02%, while Alibaba is up 80%, Google is up 29.3%, Amazon is up 71% and Apple is up 24%. By contrast, Exxon is down 5.6%, Coke is up 7.6% and General Motors is up 11%. To round out the basket, the ASX 200 is up 3.4%.

Does the market have the relative pricing of this investor basket wrong? How can some of the world’s biggest companies also be among those that are the fastest growing? And what is the problem in Australia, where even the best managers are struggling to compete with the US index benchmark?

Investors and readers intuitively know that returns from the companies which are best at running their business will do better over time. They may not know that being the best at their business now involves a whole suite of new, sharper tools, like machine learning, data mining and high speed cloud networks. But it’s over, right? Or getting close to it?

That’s not our view. Stock market investors are cautious folk – in our experience the price at which a company trades is seldom the most it could be valued at. Often it seems to be the least.

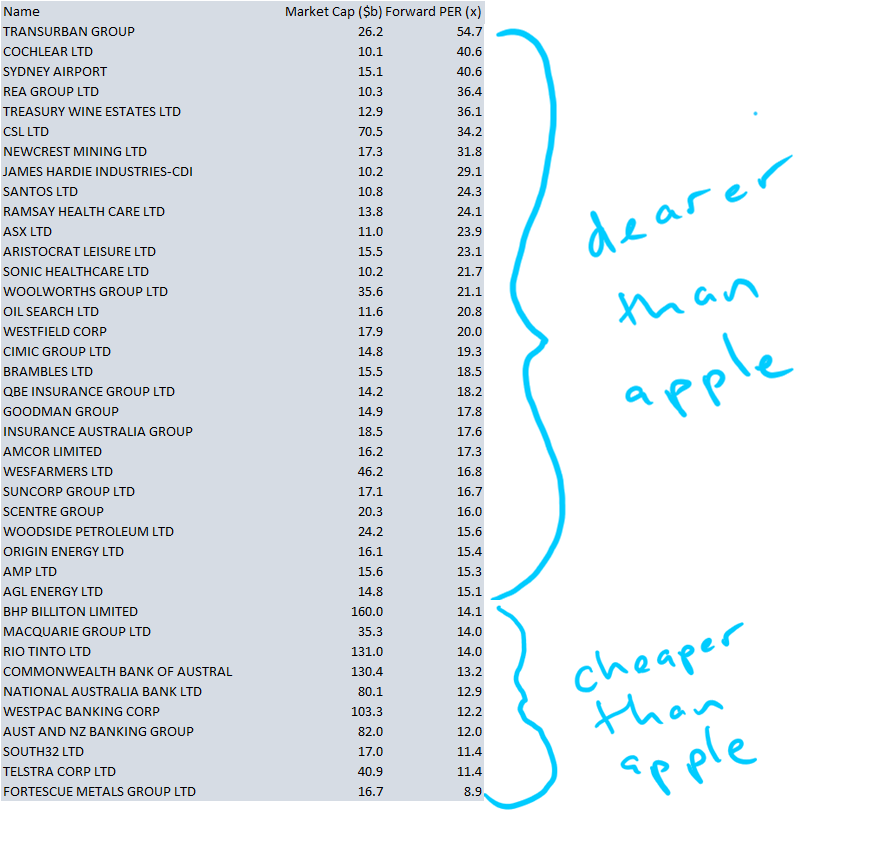

Let’s take Apple. Bloomberg has the company on a forward PER of 14.7x 2018 earnings. How many of Australia’s listed companies with a market value of over $10b trade at a multiple below this? The answer is just ten. They include the banks (because in a deteriorating credit cycle they can take massive hits to the balance sheet) and BHP.

Thirty Australian companies trade above Apple on a projected 2018 price to earnings multiple, as the table above shows. For example, Woolworths trades at 21x and serial underperformer QBE, which trots out a new turnaround story almost annually, is on 18x. AMP and AGL are just higher than Apple at just over 15x. Investors aren’t valuing Apple for its blue sky – its multiple is only 20% higher than Telstra.

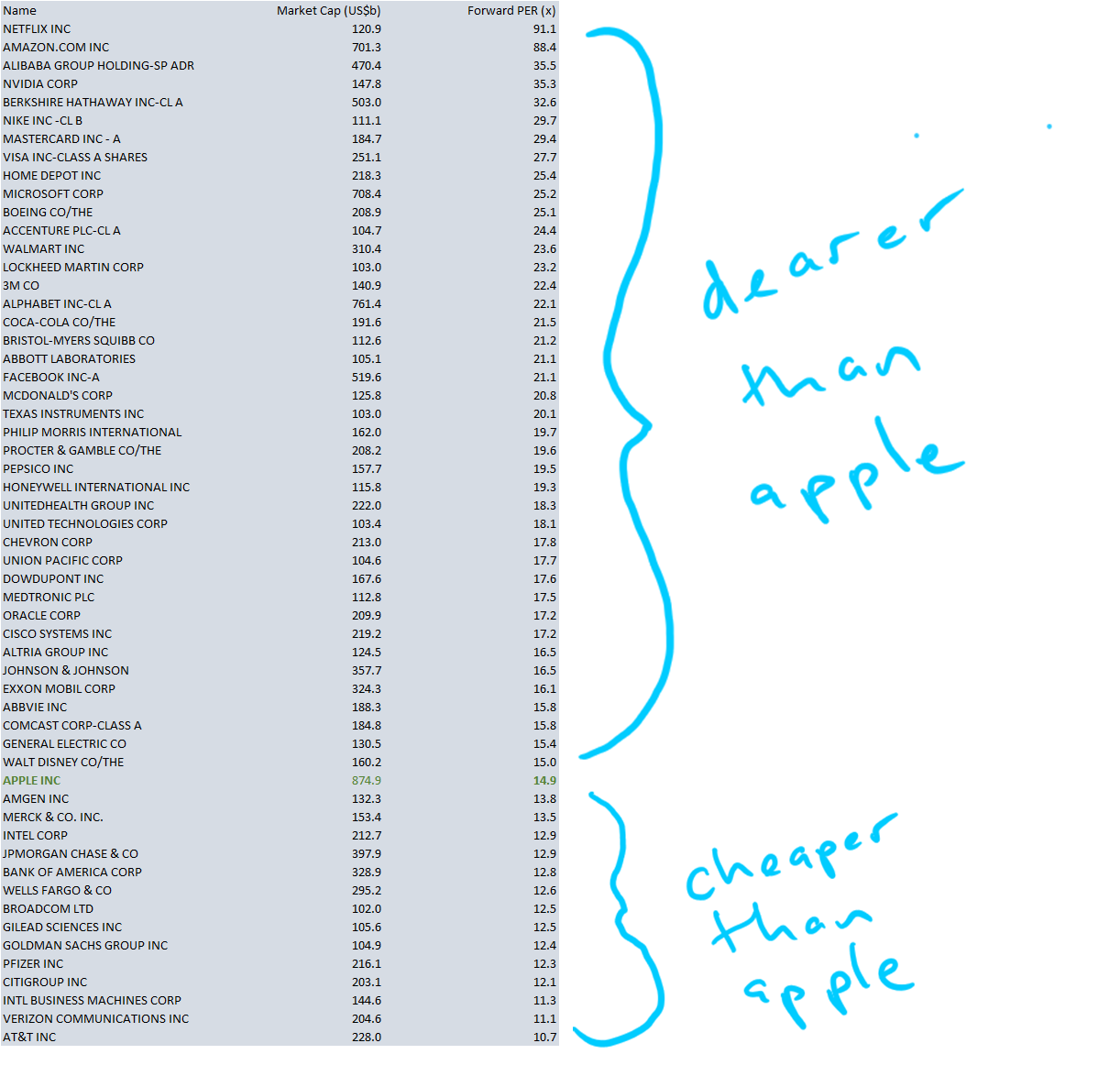

In the US, using a market capitalisation cut-off of US$100b and above, the banks (JP Morgan, Bank of America, Wells Fargo) also trade below Apple, as does pharmaceutical giant Merck, along with IBM and AT&T. But Exxon, the oil company, trades higher with a multiple of 16.1x 2018 earnings. Oddly enough, given Warren Buffett’s focus on value, the multiple for Berkshire Hathaway is higher than that of Google (Alphabet).

One reason may be too much money chasing too few assets. In Australia, because of the colossal success of the super scheme, there are significant assets (almost two trillion dollars) chasing ASX listed assets of just $1.5 trillion. (In the US, the stock market is worth US$30 trillion while the pension pool is US$22.5 trillion.)

Australia has the fourth largest pool of pension assets in the world (after the US, the UK and Japan) but its economy is the ranked 13th in GDP terms. But note this: it has the second highest pool of pension relative to GDP in the world (beaten only by the Netherlands, and ahead of the US, Canada, Switzerland, Japan and the UK). Too much money chasing too few assets, with the resultant skewing of PE multiples?

Of course, PE multiples aren’t that important - but they can be useful in providing a standardised, simplified picture. Where they completely fall apart is in valuing growth companies.

Is Amazon a sell at US$1468/share because of its stratospheric multiple of 88x? Maybe. Or maybe its to do with a round of growth which is simply not all that visible in Australia.

A significant learning from our visit to the Consumer Electronics Show in Las Vegas last month was the extent to which businesses are now focusing on using voice as the interface with the customer. There were dozens of companies pushing services or products which were voice enabled, and by far the majority were doing so using Amazon’s Alexa voice assistant as the primary tool.

Simply by saying “hey Alexa, do x” will result x being done, including physical purchase and delivery of an item. Third party developers and Amazon itself have now built 25k ‘skills’ for Alexa. These are 25000 things that Alexa can now do, including pairing wine with food, suggesting recipes, acting as your personal trainer or providing the notes to tune your guitar, not to mention ordering an Uber, running your music playlists or indeed buying nappies from Amazon. Think of these voice ‘skills’ as apps on an Apple or Google store. Alexa isn’t really here in Australia yet, but it will be, by and by.

Self-interested retailers, and many others, have consistently said that Amazon makes minimal profits, but that’s just to get folk diverted while they spin. Amazon does make less accounting profit because it reinvests all its cashflow into growing its business, and then charges the cost of that growth to following year earnings. The company has only ever had one equity issue, its net debt position is zero yet it has over $80b in depreciated plant and equipment on its balance sheet, paid for through internally generated cashflow.

All of which is too say be careful reading too much into large numbers. There are of course pockets of overvaluation as well as general irregularities, but there are some unusual forces at play pushing some valuations justifiably higher too. You just have to work out what they are.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

CIO of Loftus Peak, a specialist global fund manager with a track record of successful investment in some of the world's fastest-growing listed businesses.

1 topic

7 stocks mentioned

CIO of Loftus Peak, a specialist global fund manager with a track record of successful investment in some of the world's fastest-growing listed businesses.

Expertise

CIO of Loftus Peak, a specialist global fund manager with a track record of successful investment in some of the world's fastest-growing listed businesses.

Expertise

Comments

Comments

Sign In or Join Free to comment