QBE up 4% as housekeeping shows through

In each semi-annual reporting season, there are a few dates in the calendar that a fund manager will have circled either with pleasure or trepidation, either due to the expectation of a very good result or the fear that unpleasant issues will be uncovered. In February 2019 two of those dates marked on the calendar were last Thursday for Wesfarmers (anticipated capital return) and today for QBE Insurance’s annual result.

As a result of a range of recurring issues stemming from acquisitions made before 2010, over the past five years QBE’s results have generally both been complex to analyse and have contained unpleasant surprises.

However, today’s result from QBE was a clean result that reflects the moves management have made over the past few years to simplify QBE’s sprawling insurance empire.

3 key points from today's results

1: Keeping it simple

Decisions made by management to divest QBE's Latin American operations and domestic travel insurance arm has improved the underlying quality of company earnings and reduced volatility. QBE’s Latin American business had been the source of downgrades from exotic insurance products such as Argentinean workers comp (2014), crop losses in Ecuador and fraud in their Columbian third-party motor liability portfolio (2017). Selling these problematic businesses that have both consumed shareholder capital and management attention while delivering minimal returns, looks like a case of addition by subtraction.

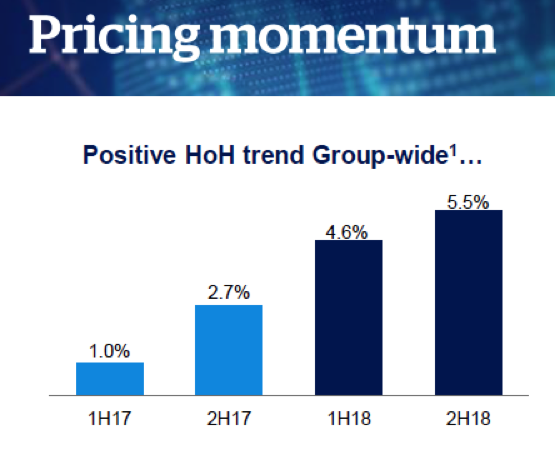

2: Rising premiums across the board

One of the highlights in QBE’s result was seeing the hardening of insurance premiums globally, which will give the company solid momentum going into 2019. While insurance premiums in Australia have been rising over 5% per annum for some years, premium growth in Europe and North America has recently been stagnant. Today QBE reported that achieved rate rises of around 4% in both Europe and the USA in 2018 and at the same time have been retaining around 80% of their existing clients.

3: Climate change and insurance

The simplification process is expected to continue in 2019 with QBE looking to exit businesses in natural catastrophe-prone areas such as Puerto Rico, Indonesia and the Philippines. Additionally, on the analyst call, management commented about their unwillingness to insure beach front hotels going forward. After seeing the beach erosion caused by cyclone Oma in Queensland and New South Wales over the weekend, this would appear to be a recognition of the impact that climate change is having on the insurance business and the pricing of risk based on historical models.

Source: Gold Coast Bulletin

Trading on a PE of 12 times, with a 5% yield

Nothing in this result changes our investment view on the company. QBE has a diverse class of insurance business lines across Australia, Asia, Europe and America and gives the portfolio exposure to both a falling AUD, rising interest rates and a hardening of insurance pricing globally.

QBE has spent some years in investor’s doghouse, but we like the moves current management have made in shrinking the business to greatness, profitability and most importantly greater predictability.

We increased our position in QBE late in 2018 on the anticipation that this result would be well received by the market and provide evidence that management’s simplification strategy was working,

QBE trades on an undemanding PE multiple of 12x with a 5% dividend yield and will enjoy near term tailwinds from hardening premium rates globally and rising interest rates.

Increasing the duration on their bond portfolio

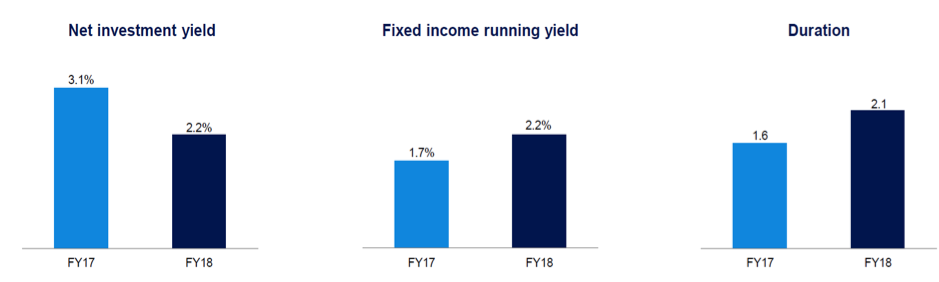

Rising interest rates are viewed as a negative for most businesses, however for insurance companies such as QBE they are a positive as rising rates increase the investment returns on the company’s US$23 billion insurance float, and in particular on the bonds and money market instruments held in the USA, UK and Europe.

Over the past five years, QBE has kept the duration of their fixed interest portfolio between 1 and 1.5 years, to minimise the impact of rising interest rates. Something that stood out in the result was the increase in duration of QBE’s bond portfolio from 1.6 to 2.1 years, which indicates that QBE sees that interest rate increases have plateaued.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

1 topic

1 stock mentioned

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Comments

Comments

Sign In or Join Free to comment