Rethinking Income: Where to find higher yields with stability

Mitchell Goldstein

Ares Wealth Management Solutions

Coming into 2020, income investors had been on a “hunt for yield” due to low interest rates globally. Fast forward to the present and the search for income has only intensified as the COVID-19 pandemic has shaped investor sentiment and pushed government and traditional fixed income yields below one percent, and in some cases into negative territory.(1) Additionally, traditional sources of income, such as dividend-paying equities, have become a less reliable source of income during this period.

Against this backdrop, we believe investors should think outside the box and look beyond traditional asset classes for income. We believe the credit markets provide multiple sources of alternative income for investors due to their historically attractive yields, defensive structures and historical risk-return profile. In this piece, we will examine alternative income solutions in today’s credit markets and their role in an investor’s portfolio.

Sources of Alternative Income

There are various opportunities within the credit markets that we view as alternative sources of income. They span the liquidity spectrum, and total returns are typically driven by income. The yields on these asset classes are generally priced at a premium to traditional fixed income due to factors such as credit risk and liquidity. These alternative asset classes can be viewed as a more reliable source of income compared to traditional public equities as the current income component is contractual.

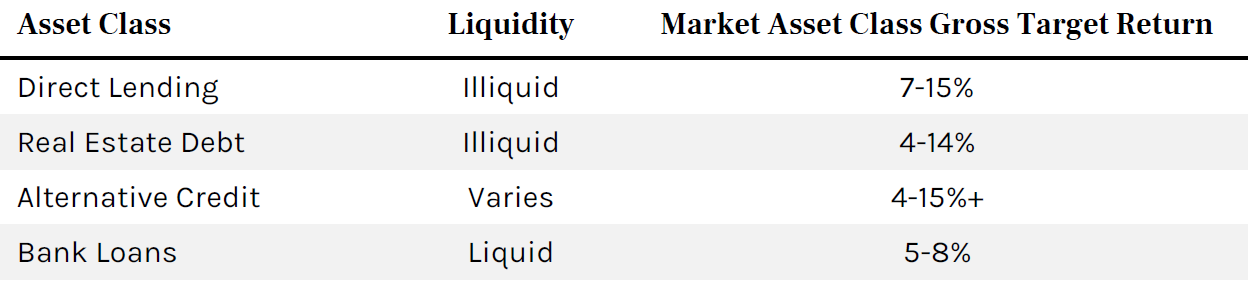

Alternative Income Universe

Corporate Direct Lending (“Direct Lending”): A transaction where a lending source directly provides a loan to the borrower without the use of an intermediary. This is accomplished by directly engaging with private equity sponsors or owner/operators of middle market companies (generally $10 - $150 million of EBITDA or greater) to originate loans. As the asset class has evolved, select managers have been able to execute larger transactions which overlap with the broadly syndicated market.

Illustrative Example: Direct Lending

A private equity firm seeks financing to support their buyout of a market leading software company. The target company provides mission-critical products and has a global, diversified customer base with strong retention rates. The acquisition occurs during a period of elevated market volatility, and sentiment across public and private markets is risk averse. To finance the transaction, the private equity firm approaches an alternative investment manager (the “manager”) with a scaled, experienced direct lending business. The manager has supported the target company historically and has in-depth knowledge of their business model. Additionally, the manager has sufficient assets under management such that it is able to underwrite risk during a period of elevated volatility. Due to market conditions, the manager can negotiate enhanced pricing and tighter documentation as compared to its prior deals with the target company. As such, the private equity firm can execute on its buyout of the software company while the manager is able to finance the company and provide its investors with an attractive, defensively structured source of current income.

Commercial Real Estate First Mortgage Lending (“Real Estate Debt”): Transactions secured by first lien loans on commercial properties, such as offices, multifamily or industrial properties and located in top markets with strong real estate fundamentals. First mortgage loans are senior in the capital structure, with additional protection from the borrower’s equity and can be structured to provide further principal and yield protection through loan covenants.

Illustrative Example: Real Estate Debt

An institutional investor seeks capital to invest in a commercial real estate property. The property is an office complex located in a large metropolitan city in the U.S., and has financially stable, investment grade companies as tenants. The institutional investor reaches out to an alternative investment manager (the “manager”), typically one they have borrowed from previously, to secure financing. The financing is efficiently priced and structured directly with the institutional investor, resulting in favorable pricing and terms. The result is a high-quality loan negotiated by the manager that generates an attractive and stable coupon with principal protection. The manager negotiates a LIBOR floor, or a minimum rate, which allows the manager to protect against potential decreases in LIBOR.

Alternative Credit: Alternative Credit transactions span public and private markets and are secured by specialty, financial or real assets that generate cash flows upon which the investment relies for repayment. These investments can offer downside protection given ample levels of credit enhancement and robust covenant packages.

Illustrative Example: Alternative Credit

An institutional investor (the “investor”) has existing financing against their diversified portfolio of securities. A bout of market volatility shakes investor sentiment and the traditional lending markets. As a result, the asset manager faces significant liquidity pressures. Through a wide network of relationships, an alternative investment manager (the “manager”) approaches the institutional investor with a refinancing solution. The manager uses their vast resources to underwrite the underlying securities in the investor’s portfolio. The ultimate transaction is a term loan backed by the underlying pool of securities. The loan requires portfolio cash flows be used to repay principal and interest on the loan, has a limited three-year term, and is covenant heavy.

Syndicated Bank Loans (“Bank Loans”): These are transactions where a below investment grade company obtains a loan from an arranger who then syndicates the loan to investors, such as pension funds and collateralized loan obligations (“CLOs”). Bank loans are traded instruments in the liquid portion of the nontraditional credit market, are typically senior secured, and pay a floating rate coupon.

Illustrative Example: Bank Loans

A private equity owned collision repair company seeks financing to fund their merger with an industry peer. The companies are market leaders in the U.S. and look to the capital markets and direct lenders to finance the merger. The company and its private equity owner have an existing relationship with a direct lender which also has a dedicated liquid credit business and multi-billion-dollar bank loan portfolio. The company is able to secure part of their financing package through a deal with the direct lender and their liquid credit business. The remaining portion of the package is arranged and syndicated by a bank. The bank approaches various firms regarding the bank loan and assigns a tight deadline for demand. The manager is able to leverage their multi-year relationship with the company for enhanced diligence and is able to quickly convey demand to the arranger bank. As a result, the manager is able to receive a favorable allocation of the syndicated bank loan.

These asset classes span the liquidity and return spectrum and are typically defensive structures which sit senior in the capital structure. Covenant packages are typical for the illiquid asset classes, though can exist in the liquid markets as well.

Targeted Market Asset Class Returns

Based on Ares current market observations as of June 30, 2020.

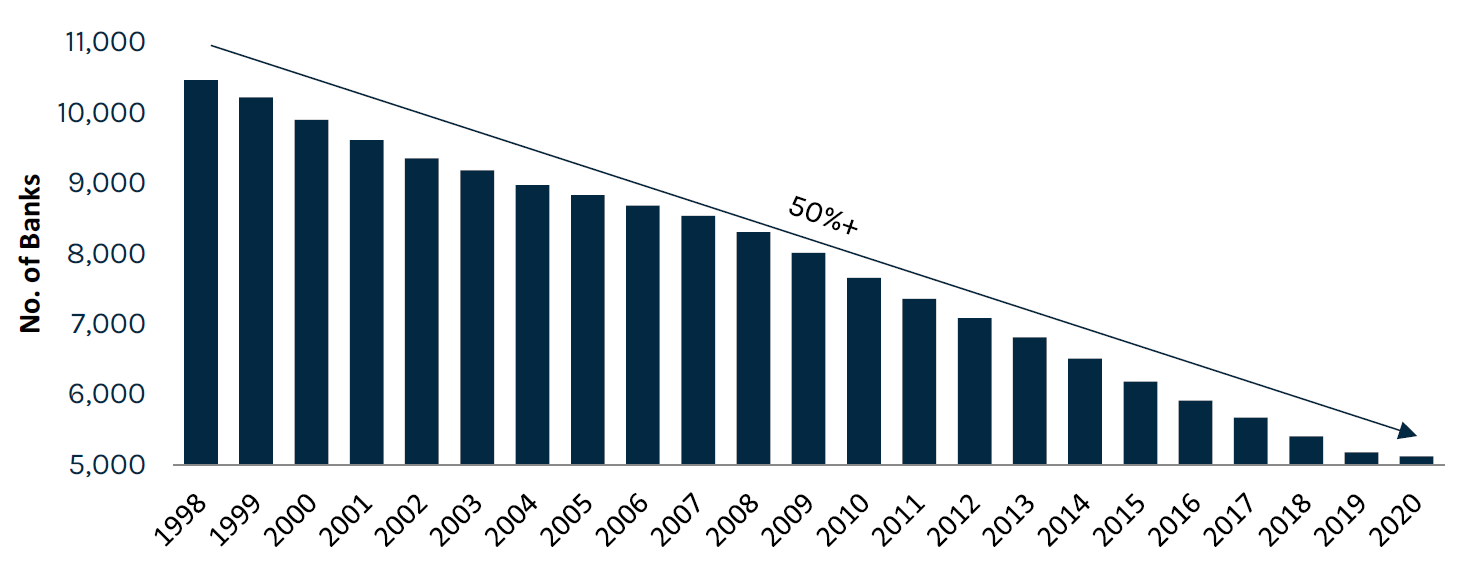

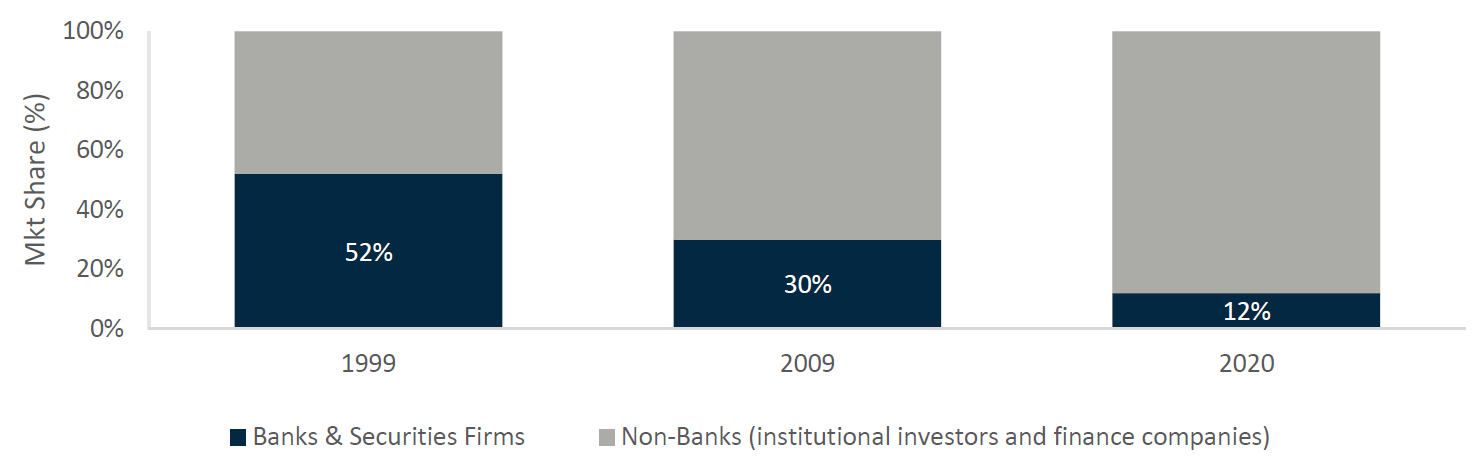

Together, these sources of alternative income represent a vast, multi-trillion-dollar opportunity set. The market opportunity has benefitted from secular trends in the banking industry, notably consolidation and regulatory changes, which has decreased the number of banks as well as their appetite to hold leveraged credit assets. Alternative investment managers have stepped in to fill the void.

Decline of U.S. Banks

Source: Federal Deposit Insurance Corporation (FDIC), “Statistics at a Glance: Latest Industry Trends,” March 31, 2020. For illustrative purposes only

Holders of Bank Loans

Source: LCD. As of March 31, 2020. For illustrative purposes only. Calendar year 2020 data Is for the twelve months ending March 31, 2020.

Where does this fit in my portfolio?

Even though each market has its own unique traits and nuances, the asset classes within the alternative income universe can generally enhance traditional fixed income and equity portfolios in the following ways:

From an income and yield perspective, these assets offer varying premiums relative to traditional fixed income. The below chart provides a tangible example of the current opportunity set in the liquid alternative markets. In the illiquid space additional excess income can also be generated.

Relative Value in Liquid Markets

As of May 31, 2020. For illustrative purposes only Please refer to pages 7-8 for Index Definitions. (1) Credit Suisse Leveraged Loan Index. (2) Credit Suisse Western European Leveraged Loan Index. (3) JPM CLOIE BBB Post-Crisis. (4) ICE BofA US Corporate Index. (5) ICE BofA Euro Corporate Index. (6) ICE BofA US Treasury & Agency Index (7) ICE BofA European Union Government Bond Index.

Risk and Reward

The benefits of alternative income are not free, and their attractive yields typically come with additional credit risk when compared to traditional fixed income. That said, active managers can mitigate this risk through forensic due diligence and by taking a selective approach to credit allocation. Some managers have been able to successfully execute over time, with low default and loss rates over multiple cycles.

Alternative income assets have demonstrated limited volatility over time. For more liquid markets like bank loans, the attractive income component has contributed to stability and downside protection relative to traditional asset classes. For example, the bank loan market has been a dependable source of positive returns with only two years of negative returns since 2000 (2). The illiquid nature of direct lending, real estate debt and certain forms of alternative credit enhances the already muted asset level volatility exhibited by the liquid assets. An investor’s experience can vary depending on the vehicle used to access these asset classes and the asset allocation mix of the portfolio.

These assets offer limited duration relative to their traditional counterparts as well. Currently, the bank loan market has a duration of 0.91 years compared to 7.27 years for the global fixed income market,(2) and the weighted average life of illiquid alternative assets are typically 3 years.

The combination of attractive yields, low duration and defensive structures have contributed to an attractive risk/return profile over time.

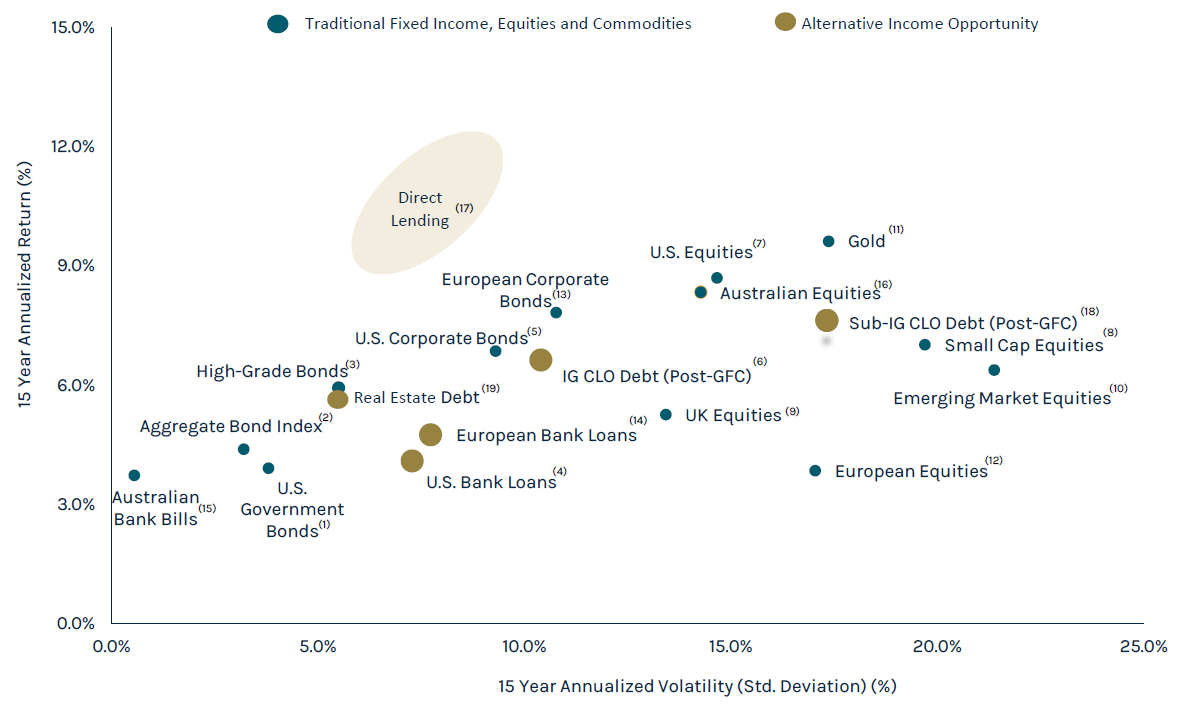

We believe these alternative income assets sit in the “sweet spot” relative to traditional asset classes, offering enhanced yields and total returns when compared to traditional fixed income, and limited volatility when compared to public equities. Returns in these alternative asset classes are primarily driven by coupon, but total return opportunities exist in the more liquid markets as trading volatility year-to-date has increased convexity in these markets. The increased volatility has created opportunities where active managers are able to acquire assets at a discount to their face value, creating an opportunity for capital gains.

Alternative Income: The "Sweet Spot" of the Risk/Reward Spectrum

As of May 31, 2020, unless otherwise noted Please refer to pages 7-8 for Index Definitions For illustrative purposes only. An investor cannot invest directly in an index. Index returns do not reflect the deduction of fees or expenses, and do not represent the performance of any specific investment. (1) 5Y Treasury Bond. (2) Bloomberg Barclays US Aggregate Bond Index. (3) JPM JULI High Grade Index. (4) Credit Suisse Leveraged Loan Index. (5) JPM US HY Index. (6) JPM CLOIE BBB Post-Crisis. Annualized return since 2012. (7) S&P 500 Total Return. (8) Russell 2000. (9) FTSE 100. (10) Dow Jones EM Stock Index. (11) IAU US Equity. (12) EURO STOXX 50. (13) ICE BofA Euro High Yield Index. (14) Credit Suisse Western European Leveraged Loan Index. (15) Bloomberg AusBond Bank Bill Index. (16) S&P/ASX 200. (17) Based on Ares current market observations. (18) JPM CLOIE BB Post-Crisis. Annualized return since 2012. (19) Giliberto-Levy (G-L) Commercial Mortgage Performance Index

Conclusion

Alternative income assets can be a reliable source of current income for investors looking to fill the void created by low interest rates and corporate fundamental uncertainty triggered by the COVID-19 pandemic. Specific to credit, these asset classes span the liquidity and return spectrum, though their structures share similar defensive characteristics. We believe these assets sit in the “sweet spot” of the risk reward spectrum, generating attractive returns compared to traditional fixed income and reduced volatility compared to equities. There are a number of synergies between these alternative assets, and we believe managers who have invested heavily in origination and capital markets capabilities can create significant competitive advantages. Additionally, we believe that managers with flexible capital have significant competitive advantages in developing creative solutions across a broader spectrum of opportunities.

Looking for alternative income?

Ares takes both a bottom-up and top-down approach, with a deep focus on disciplined credit selection and active asset rotation, as well as current, and forward looking global macroeconomic and technical factors impacting each sector. For more information, fill in the contact form below, or visit our website to learn more.

Footnotes

(1) Source: Bloomberg, as of June 19, 2020.

(2) Source: Bloomberg, Credit Suisse. As of May 31, 2020.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Mitchell Goldstein is a Partner and Co-Head of the Ares Credit Group and a member of the Management Committee of Ares Management. He additionally serves as Co-President of ARCC and Vice President and interested trustee of CION Ares Diversified Credit Fund. He is a member of the Ares Credit Group's U.S. Direct Lending and Commercial Finance Investment Committees and the Ivy Hill Asset Management Investment Committee. Prior to joining Ares Management in May 2005, Mr. Goldstein worked at Credit Suisse First Boston, where he was a Managing Director in the Financial Sponsors Group.

Featuring

Mitchell Goldstein,

Ares Wealth Management Solutions

Mitchell Goldstein is a Partner and Co-Head of the Ares Credit Group and a member of the Management Committee of Ares Management. He additionally serves as Co-President of ARCC and Vice President and interested trustee of CION Ares Diversified Credit Fund. He is a member of the Ares Credit Group's U.S. Direct Lending and Commercial Finance Investment Committees and the Ivy Hill Asset Management Investment Committee. Prior to joining Ares Management in May 2005, Mr. Goldstein worked at Credit Suisse First Boston, where he was a Managing Director in the Financial Sponsors Group.

........

The information in this publication is current as at the date of publication and is provided solely by Ares Management LLC (Ares). Ares is exempt from the requirement to hold an Australian Financial Services Licence. Ares is subject to regulation by the Securities & Exchange Commission of the United States of America under US laws, which differ from Australian laws. None of Ares Australia Management Pty Limited, Fidante Partners Limited, nor any of their associates, has prepared the information in this publication and accept no liability whatsoever in relation to it.

This publication is only made available to 'wholesale clients' or 'sophisticated investors' under the Corporations Act 2001 (Cth) in Australia.

This publication has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this publication should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting on the advice. Persons receiving this information should obtain and read any disclosure document relating to any financial product to which the information relates before making any decision about whether to acquire that product.

No reliance: This publication is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The publication has not been independently verified. None of Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd, nor any of their respective related bodies corporates, associates and employees, make any republications, warranty or undertaking (express or implied) and accepts no responsibility for the adequacy, accuracy, completeness or reasonableness of the publication or as to the performance of any product. The information contained in the publication does not purport to be complete and is subject to change. No reliance may be placed for any purpose on the publication or its accuracy, fairness, correctness or completeness. None of Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd, nor any of their respective related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the publication or otherwise in connection with the publication. Any forward-looking statements in this publication: are made as of the date of such statements; are not guarantees of future performance; and are subject to numerous assumptions, risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Ares undertakes no obligation to update such statements. Past performance is not a reliable indicator of future performance.

Confidentiality and intellectual property: This publication is confidential and may not be copied, reproduced or redistributed, directly or indirectly, in whole or in part, to any other person in any manner.

Risk: no person guarantees the performance of, or rate of return from, any product or strategy relating to this publication, nor the repayment of capital in relation to an investment in such product or strategy. An investment in any such product or strategy is not a deposit with, nor another liability of, Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd nor any of their respective related bodies corporates, associates or employees. Investment in any product or strategy relating to this publication is subject to investment risks, including possible delays in repayment and loss of income and capital invested.

This may contain information sourced from Bank of America, used with permission. BANK OF AMERICA IS LICENSING THE ICE BOFA INDICES AND RELATED DATA “AS IS,” MAKES NO WARRANTIES REGARDING SAME, DOES NOT GUARANTEE THE SUITABILITY, QUALITY, ACCURACY, TIMELINESS, AND/OR COMPLETENESS OF THE ICE BOFA INDICES OR ANY DATA INCLUDED IN, RELATED TO, OR DERIVED THEREFROM, ASSUMES NO LIABILITY IN CONNECTION WITH THEIR USE, AND DOES NOT SPONSOR, ENDORSE, OR RECOMMEND ARES MANAGEMENT, OR ANY OF ITS PRODUCTS OR SERVICES.

This may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard & Poor’s. Reproduction and distribution of third-party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes and should not be relied on as investment advice.

REF: CP-00514

4 topics

Mitchell Goldstein

Partner, Co-Head of Credit Group

Ares Wealth Management Solutions

Mitchell Goldstein is a Partner and Co-Head of the Ares Credit Group and a member of the Management Committee of Ares Management. He additionally serves as Co-President of ARCC and Vice President and interested trustee of CION Ares Diversified...

Expertise

Comments

Comments

Sign In or Join Free to comment