TOL - 18th Jan, 2021

Riding the Australian recovery

When I opened my last letter to investors in June, I said that recovery was certain. The extraordinary fiscal response, and a likely vaccine, would help end the sharp and deep Worldwide Pandemic Recession of 2020.

We expected growth assets, such as equities and property, to begin to price in this recovery. We believed that low bond yields and cash rates, compressed by quantitative easing under the direction of central banks, would lead investors (particularly pension asset managers) to seek out and therefore reprice risk assets.

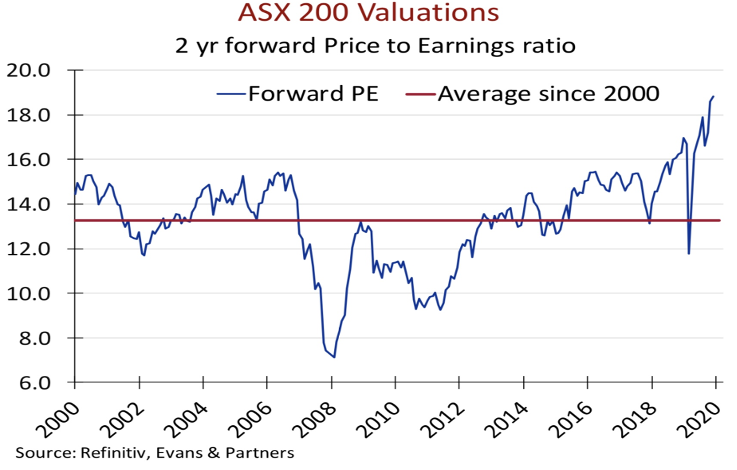

By the end of 2020, we saw this play out, with equities the first to rally hard with a strong price-to-earnings re-rating.

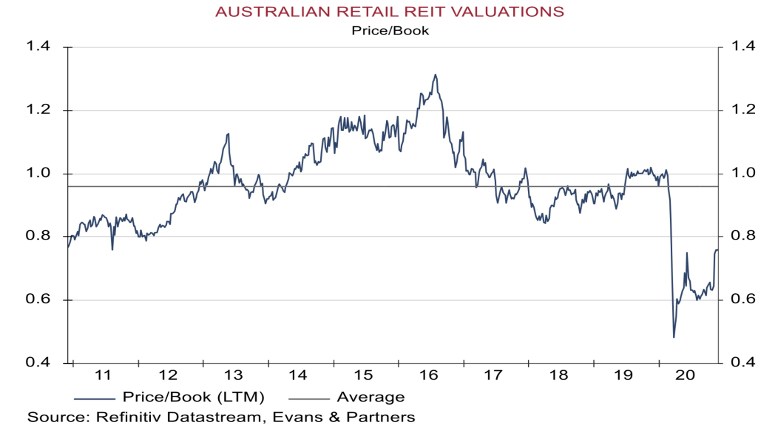

We’ve also seen property show signs of recovery, with listed REITs (for example) beginning a re-pricing as cap rates decline and retail investors begin to target yield away from term deposits.

This time it is true: A new era

While it is always dangerous (and rarely correct) for a commentary to suggest that either a new era has begun or an inflexion point past, it seems that the world has now clearly moved into a new cycle supported by extraordinary economic management.

Progressively, and since the depths of the GFC in late 2008, both governments and central banks have experimented with and implemented a range of unconventional policies.

The following policies have been created over the last decade and are still aggressively pursued today:

- The bailout of significant financial institutions (“too big to fail”)

- the unrelenting support for the funding of governments (massive bond issuance)

- the support of negative-yielding bonds (in most of Europe and Japan)

- unrelenting and rolling QE

- huge fiscal deficits and currency manipulation.

Some were adopted following their introduction into the Japanese economy in the years prior to the GFC. Others were simply invented as a response to extraordinary financial issues. But today, all have been widely adopted across the developed world and are now embedded in economic management.

When we focus on Australia, we have seen the “conservative” Coalition government make a remarkable adjustment (indeed a reversal) in both the economic and monetary policy management as well as it’s stated focus of fiscal management.

In 2019, our government suggested that the balancing of the Australian budget and the long-term reduction in Commonwealth debt was its priority. Further, the RBA stated that QE was a policy that it did not agree with and would not adopt. Similarly, zero bound interest rates, that penalized savers, was a policy that was deemed unlikely to be justifiable.

During 2020 (and now beyond) things have dramatically changed and policies have been adopted that have taken both Australian and world markets into a profoundly new cycle. For the foreseeable future, investors will be burdened with interest rates settings that are either negative or below the real rate of inflation.

This interest rate targeting is necessary to support the servicing of government debts created by extraordinary fiscal deficits. Suddenly, debt is not a problem and no government dares suggest that it should be paid back (at least, not anytime soon).

In this new cycle, in Australia, the RBA’s covert edict is that savers are (regrettably) to be penalised, while borrowers are supported. Indeed, monetary policy settings will be utilised to strongly support the debts at all levels of Australian government.

As this new cycle becomes apparent to investors, first the professionals and then retail or household investors, it will result in the significant and sustained re-pricing of assets. In simple terms, we will see (in order):

- bond yields plummet;

- corporate debt spreads decline;

- PE ratios become further elevated;

- property capitalisation rates fall.

Bond yields and corporate debt yields have already adjusted. So, from now it will be equities and property that become the asset classes that offer the best forward-looking returns.

What can investors expect in 2021?

We believe that the broad recovery in both the global economy and therefore global asset markets will continue into 2021. The tailwinds are simply too compelling.

The combination of unrelenting QE, massive fiscal stimulation, accommodative central banks supporting financial intermediaries and controlled and targeted low interest rates provide powerful tailwinds to economies that are in recovery cycles. These tailwinds will push up and sustain the prices of risk assets that will anticipate the improved outlook for profits and cashflows for both companies and properties alike.

But at some point during the second half of 2021 (if not sooner) prices may well have reached levels that fully reflect the recovery two to three years hence. From this point, the outlook for returns will be lower as markets wait for economies to catch up and justify the high prices that have been set.

For the moment, we are still in the “re-pricing up” mode – and that means investors should either be increasing or maintaining exposure to risk assets such as equities and property (both direct and listed), and to seek out appropriately priced and liquid yield assets (well managed and high yielding LICs may well come back into vogue).

Inside the equity sleeve, which should be increased as a weighting inside a balanced portfolio, a higher allocation to Australian equities should be considered. This reflects our view that while the outlook for world economic recovery is good, the outlook for Australia’s economy and therefore its equity market is superior.

This view reflects three observations:

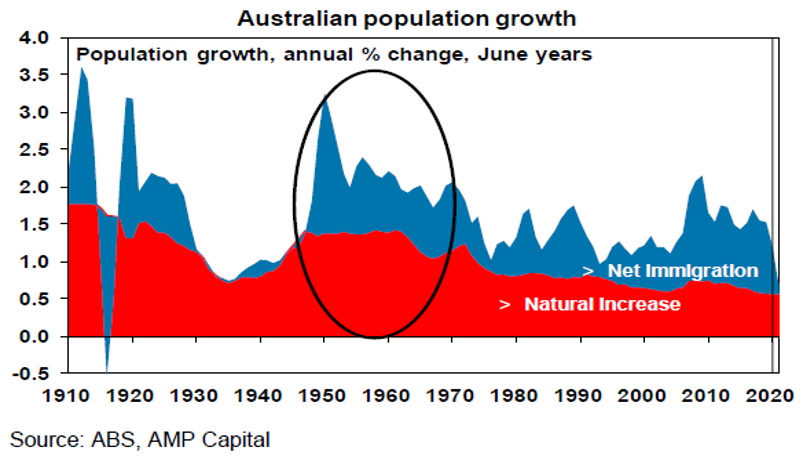

- Australia has a superior growth outlook compared with our western peers due to population growth that will predictably occur once COVID is under control.

- Australia’s sharemarket index has rebalanced over the last decade to better reflect the domestic economy and the growth opportunity.

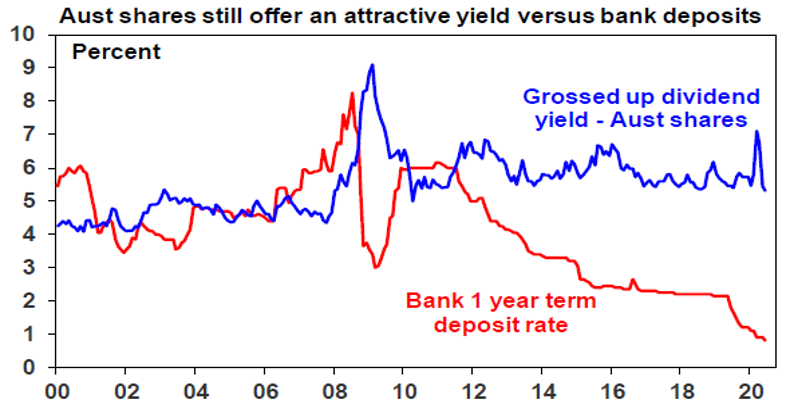

- Australia’s equity market has a superior yield, with franking credits offering an enhanced return to domestic investors.

Source: AMP

Economic tailwinds

We believe there are significantly more positives than negatives lining up for the Australian economy and therefore the equity market. These include:

1. A restart to immigration: We expect Australia’s high immigration levels to start again after 12 to 18 months of very low rates due to closed borders. We suspect the Government will ramp up rates in 2022-23, and that from 2022 to 2025 Australia’s population, including natural increases, will grow by over 1 million people.

That population growth, of around 3.5%, is very positive for the economy. With mild inflation, we believe that Australian GDP could grow by 5% in 2022/23.

Following a sustained focus on infrastructure development and investment during the COVID downturn, we believe that Australia is ready to accelerate immigration, as it has many times in the past – for example, after the Second World War and the GFC.

2. Recovery followed by sustained growth: As noted above, we expect the Australian economy to recover faster than the rest of the world. Therefore, after the initial bounce, and helped by strong population growth, we think it can then grow sustainably by between 4% to 5% pa from 2023 through to 2025. This is above current budget projections, given that Government immigration policy is yet to be reset.

By contrast, from 2022 to 2025, we estimate that Europe and Japan will grow at rates below 3%, and the US will sit at a growth rate of around 3.5%.

We predict that Australia will grow at a rate 1% to 1.5% stronger than the rest of the developed world.

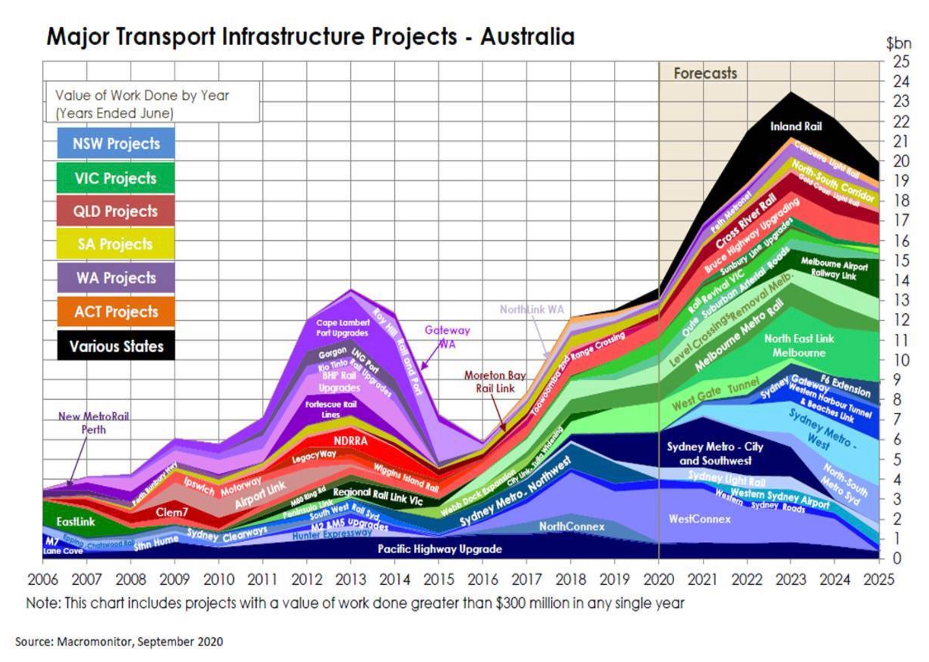

3. Strong government investment: With the shackles of trying to balance the budget and reducing Commonwealth debt undone, the intensive Government investment program (both State and Federal) will be very positive for the economy.

After a period of lower growth (2020/21) and restricted immigration, Australia will move through its infrastructure backlog, meet the growth opportunity, and drive productivity improvements.

We will also be better positioned to take more overseas tourists when borders reopen and push the tourism trade deficit towards or into a surplus.

4. Monetary policy: As noted above, the RBA has given strong guidance that interest rates will remain low for at least the next three years. Further, if Australia’s superior growth outlook feeds into a stronger AUD, it is possible that cash rates may be taken below zero given international settings.

In the short term, zero-bound interest rates will be positive for economic activity as it allows the government to pump the Australian economy at very little cost to the Federal Budget outcomes.

The adoption of QE by the RBA also sets in train a continuing requirement for the RBA to intervene with subsequent QE programs. Overseas experience suggests that QE programs do drive economic activity at their outset.

However, we caution that, based on overseas observations, these policy settings will need to be adjusted as soon as international markets allow.

5. China trade should normalise and Asia beckons: We believe (see below) that current trade tensions with China will substantially rectify themselves in 2021.

Another positive for Australia is the massive potential from Asian trade. We need to push hard into India and other developing countries. If we embrace Asia, there are exciting opportunities for Australia.

The lucky country

The Australian economy is set to significantly outperform in coming years. All the tail breezes for the Australian economy and equity markets are in place – fiscal, monetary, productivity, and trade.

The outlook for Australia is better now – both actual and comparatively – relative to our Western peers than at any time in the last 10 years.

After being wary of Australian equities for many years, we believe our strong relative economic performance will flow through to a better-balanced Australian share market.

In particular, the de-weighting of the financial sector (mainly large banks) in the Australian index and the emergence of a range of growth companies across e-commerce, e-financial, online retail, services-related and materials companies suggests that the Australian market will reach sustainable new index highs. The Australian index now better represents the Australian economy.

A few risks put into context

Having looked at the tailwinds, there are some risks to the outlook, but we regard these as possible rather than probable.

Residential property: This continues to be pushed higher with too much (unregulated) mortgage debt. A return to rates of just 4%, for example, which is certain to occur at some point in the next decade, could bring mortgage stress into play.

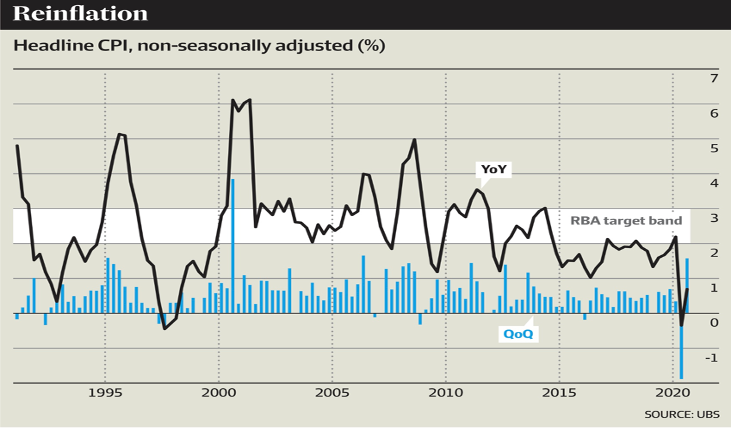

Inflation: While not yet observable on the economic horizon, it is surely a medium-term risk for interest rate settings and thus excessive levels of debt – both household and government.

However, inflation is not a present risk and we restate our often-declared thoughts on why worldwide QE hasn’t stoked inflation.

- We perceive that the US, under Democratic leadership, will push US wages higher and thereby secure the Chinese manufacturing base.

- An energy price shock is very unlikely to occur anytime soon. Short term production controls by OPEC merely support oil prices – they will not drive them sustainably higher.

- The GFC and now the COVID recession have created heightened unemployment levels in the developed world. The “excess” supply of labour suggests that wages will not push the cost of production in developed economies higher.

Our view is that while inflation is a long-term risk, it is not one in the next three or four years. Therefore, interest rates can and will stay low for a sustained and uncomfortably long period.

The other specific risk for Australia is our trade and political relationship with China that has been challenged in recent times.

Our view is that when the new Biden Administration settles in and establishes a working relationship with China, including trade, then Australia’s relationship will mend to our mutual benefit. Australia’s future lies inside the Asia Pacific trade bloc and we will continue to benefit from the world’s fastest-growing regional economy.

A balanced Australian market more reflective of our growth

The balance of economic positives over negatives should flow through to the Australian sharemarket.

Further (as noted earlier) Australian dividend yields are stronger than international equities, and franking benefits, while they remain, are very positive as well.

And after a long period of underperformance, the Australian sharemarket has finally repositioned from an index weight to banks that was historically too high.

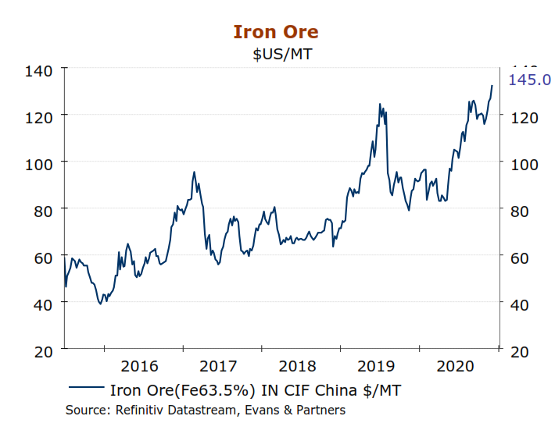

But banks have now declined in relative importance by about 20% in the index. And we have seen the emergence of resource stocks again, but this time they are mostly well managed, generating strong cashflows, high dividends and relatively lowly geared compared with past cycles.

This rebalancing of the local economy has also been fostered by the emergence of a range of new companies in IT, online retail, online credit, e-finance, and e-commerce. Out of that group will be several highly successful companies (some of which will be swept up by larger international peers).

What does this mean for investors?

1. Reduce exposure to government bonds which have become undesirable in a diversified portfolio. The risk is at some point in the next three to five years there will be a devaluation of bonds as yields lift. From such low yields, minor yield lifts will have serious effects on bond values and returns.

2. Appropriately seek out corporate and hybrid yield but retain a focus on liquidity, for this will replace an allocation to cash.

3. Stay long risk and growth assets, particularly equities and direct and listed properties. Review well managed LICs with yields higher than the Australian market index.

4. Develop a broader investment focus with international equities. Given the strong COVID tailwinds, investors should reflect on any over-exposure to US multinationals and FAANGs (Facebook, Apple, Amazon, Netflix, Google). Developing or Emerging markets offer better opportunity.

5. Stay appropriately diversified and stay well invested. Excessive weightings to cash should be checked by a sensible and deliberate investment and re-investment focus.

Stay up to date

I frequently provide insights and commentary on multi-asset investing and macroeconomic topics. If you enjoyed this article click 'like' and hit the 'follow' button below to read my upcoming articles on Livewire.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities.

Clime is a management and advisory business for mainly SMSFs.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

5 topics

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities. Clime is a management and advisory business for mainly SMSFs.

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities. Clime is a management and advisory business for mainly SMSFs.

Comments

Comments

Sign In or Join Free to comment