Significant pipeline of IPO opportunities coming?

Despite the prevailing conditions, it is our view that the Australian small business landscape is adapting to the rationing of bank capital. Remarkably, last year there were more than 250,000 new Australian businesses formed, and there are now over 2.5 million Australian registered companies.

Accordingly, we would argue that this integral component of the Australian economy has mustered ‘the courage to grow’. By being forced to adjust to prevailing trading conditions, it is apparent to us that Australian small businesses are adopting business models that are less capital intense and more technologically flexible and enabled than their larger established peers.

Given that small businesses have also been stress-tested by adverse economic conditions and restrictive costs of doing business, we believe that economic tailwinds could be a powerful force that drives Australia’s fortunes in the years ahead.

We believe that as economic strength broadens, ambitious small businesses may look to the listed equity market to fund their next phase of capital growth.

We therefore envisage that our Australian funds will be presented with a significant number of IPO opportunities over the coming years.

Mustering the courage to grow

The start of February saw RBA Governor of the Reserve Bank of Australia (RBA), Mr Philip Lowe, give his first speech for 2018 at the A50 Australian Economic Forum. Among other things, Governor Lowe addressed frequently asked queries from global investors affecting the Australian economy. The most pressing issue seemed to be the duration of Australia’s economic expansion relative to other more mature developed economies. On this issue, Governor Lowe stated that:

“One of the facts that visitors to Australia most frequently remark upon is that Australia has experienced 26 years of economic growth. Over those 26 years we have certainly experienced some slowdowns and periods of rising unemployment but this long record of economic expansion and stability is not matched elsewhere among the advanced economies”

The collective view of global investors at the forum appeared to be that Australia’s economic momentum is fatally challenged.

Specifically, should Australia’s economic growth subside, Australia’s high level of household debt would cause an irreversible negative feedback loop. While we share some sympathy for this view, we prefer to believe that Australia is not “ex-growth”.

It is our view that Australia’s economic potential has been stifled somewhat by a misconception that Australian banks (ADI) should be “unquestionably strong”, which has led to an inefficient allocation of risk capital. We believe that business leaders can liberate Australia’s economic potential by mustering the courage to grow.

Less lending to riskier businesses and its effect on the economy

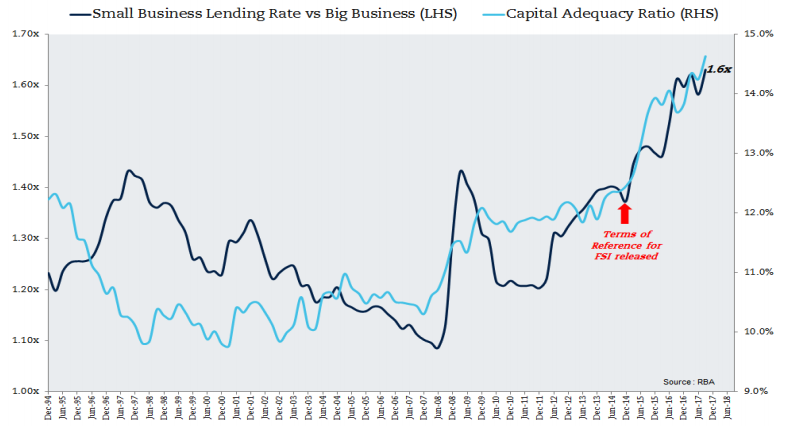

Since the Australian Treasurer announced the final terms of reference for the Financial System Inquiry in December 2013,3 ADIs collectively inflated their capital base by 45%, prompting the curtailment of lending activities. As a consequence, total bank lending growth slowed to 6.0% p.a. and Australia’s nominal GDP growth dropped to 3.4% p.a.

As a comparator, in the 25 years before the Financial System Inquiry, bank loans grew 9.2% p.a. and nominal GDP growth reached 5.9% p.a.

Interestingly, since December 2013, the rate of lending growth in the housing and commercial sectors slowed by 35%. However, there has been a significant change in the composition of commercial lending. Lending growth to big businesses is growing more than three times faster than lending to small businesses.

To us, this outcome suggests that lending capital has been deployed in risk minimisation strategies, instead of the pursuit of entrepreneurship and risktaking activities, which we believe are enablers to further economic growth

Over the past 25 years, Australian businesses with credit outstanding below AU$2 million have endured an average cost of debt 1.3 times greater than the interest rate for business with borrowings above AU$2 million.

According to RBA data, the current interest rate for businesses with debt less than AU$2 million is 5.30%, which is 1.6 times the prevailing rate for businesses with borrowings above AU$2 million. We believe that this preferential interest rate has given Australian big business an unprecedented cost of capital advantage, which predates the Financial System Inquiry.

It is our view that this interest rate differential cannot expand any further. We believe that ADIs have now inflated their capital base to levels that significantly reduce moral hazard risks.

There is little doubt in our mind that our financial system is “unquestionably strong”, however we do express some doubt as to whether Australia’s economic trajectory has been supported by this unquestionably strong financial system.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

David is the CIO for the K2 investment funds. In conjunction with his responsibilities as CIO, David dedicates his time managing an allocation of the Australian and Asian equity strategies.

David is the CIO for the K2 investment funds. In conjunction with his responsibilities as CIO, David dedicates his time managing an allocation of the Australian and Asian equity strategies.

Expertise

David is the CIO for the K2 investment funds. In conjunction with his responsibilities as CIO, David dedicates his time managing an allocation of the Australian and Asian equity strategies.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

How to choose excellent fund managers

Livewire Markets

Macro

The RBA should warn that it could raise rates again

Coolabah Capital