Six problems with the equity bull thesis

The 2008 financial crisis was, at least in part, due to a fundamental flaw in the pricing of Credit Default Swaps on housing lending. Analysts who justify the current rise in markets on falling interest rates are making a similar error.

A (very) brief history of credit default swap pricing

I won't go too deeply into the models, but you do need some background.

There is nothing intrinsically wrong with a credit default swap, or CDS.

The problem in the early 2000s was pricing models for credit default swaps assumed housing defaults were independent. i.e. that someone defaulting on a loan in Miami was unrelated to someone defaulting on a loan in San Francisco. In essence, the pricing models ignored the possibility of a housing market downturn that spanned the US.

Armed with this fallacy, banks could then "safely" lend far more than was reasonable and embarked on a massive lending spree.

Spoiler alert: the loans were not safe. The bankruptcies and the unwind of this lending was a significant cause of the financial crisis.

A (very) brief history of the lower interest rate argument

Falling interest rates have been credited by many with the rise in the stock market.

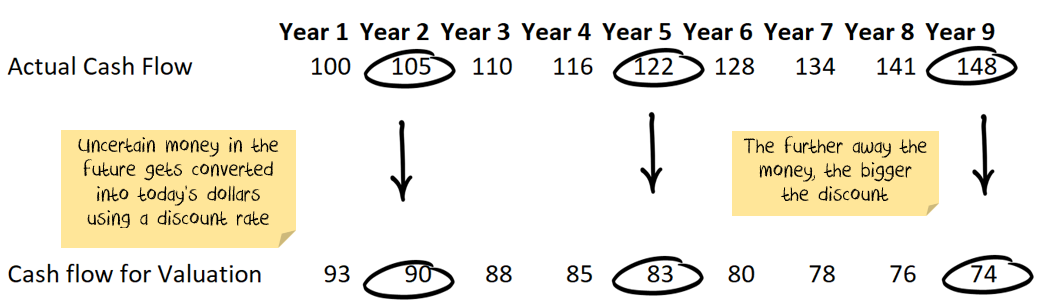

The operation is relatively mechanical, a discounted cash flow model takes future expected cash flows and then discounts them to give a current market value:

The mathematical effect of lower interest rates is that it increases the current market value.

We saw the effect Wednesday in Australia when lower interest expectations led to a broad market bounce.

Problem #1 with interest rate argument: Inflation

The most obvious problem with this analysis is that there is no context.

The only reason interest rates are low is because inflation is so low. i.e. declines in the growth rate of the cashflows simply due to lower inflation offset part of the benefit of lower interest rates.

Central banks simply cannot generate inflation, despite a dozen years of trying since the financial crisis.

Net effect: If inflation is going to be lower, then cash flows are also going to be lower, offsetting some of the valuation impact of lower interest rates.

Problem #2 with interest rate argument: Real growth

The same logic extends to the real (i.e. inflation-adjusted) growth rate of companies.

Not only is inflation low, but rock bottom interest rates reflect poor economic growth across the economy.

Net effect: If real economic growth is going to be lower, then cash flows are also going to be lower, offsetting some of the valuation impact of lower interest rates.

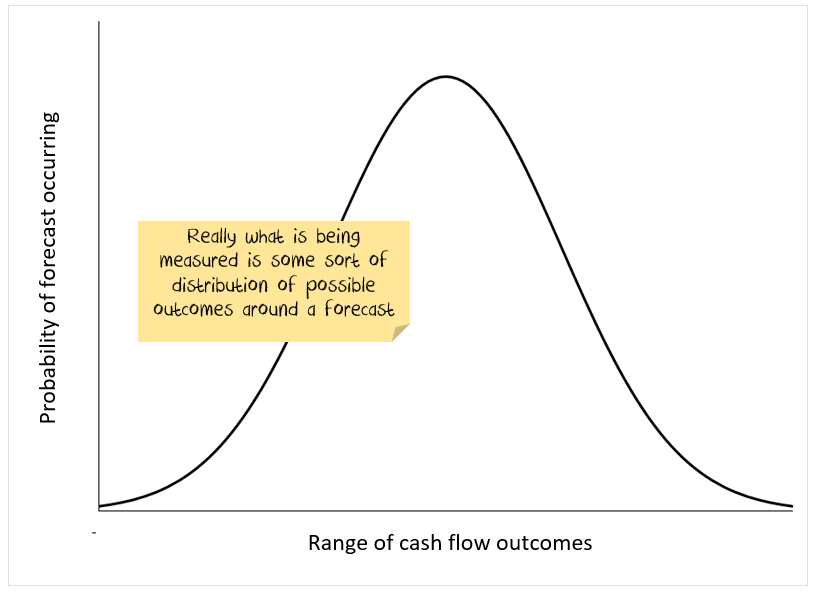

Problem #3 with interest rate argument: Distribution

In my view, discounted cash flow analysis is an excellent tool for evaluating bonds where the cashflows are known in advance.

That is not the case for shares.

With shares, each cash flow is uncertain. For a single period, we can express this as a distribution of likely outcomes:

And then multiply this effect for every year where there is a forecast.

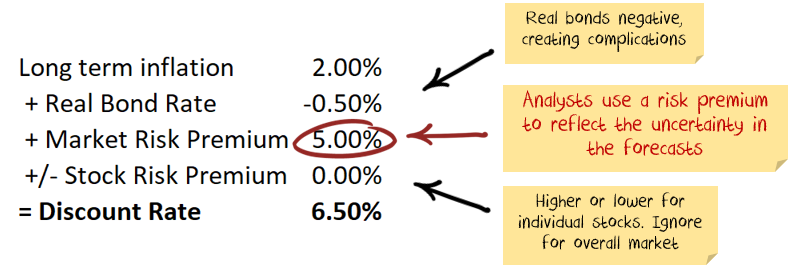

How do practitioners get around this uncertainty?

Poorly. To reflect the uncertainty of the earnings, analysts add a risk premium to the discount rate to drag the future value lower:

So, facing increased uncertainty, there should be some increase in the risk premium to offset the fall in interest rates.

Net effect: If economic uncertainty is higher, then the market risk premium should also be higher, offsetting some of the valuation impact of lower interest rates.

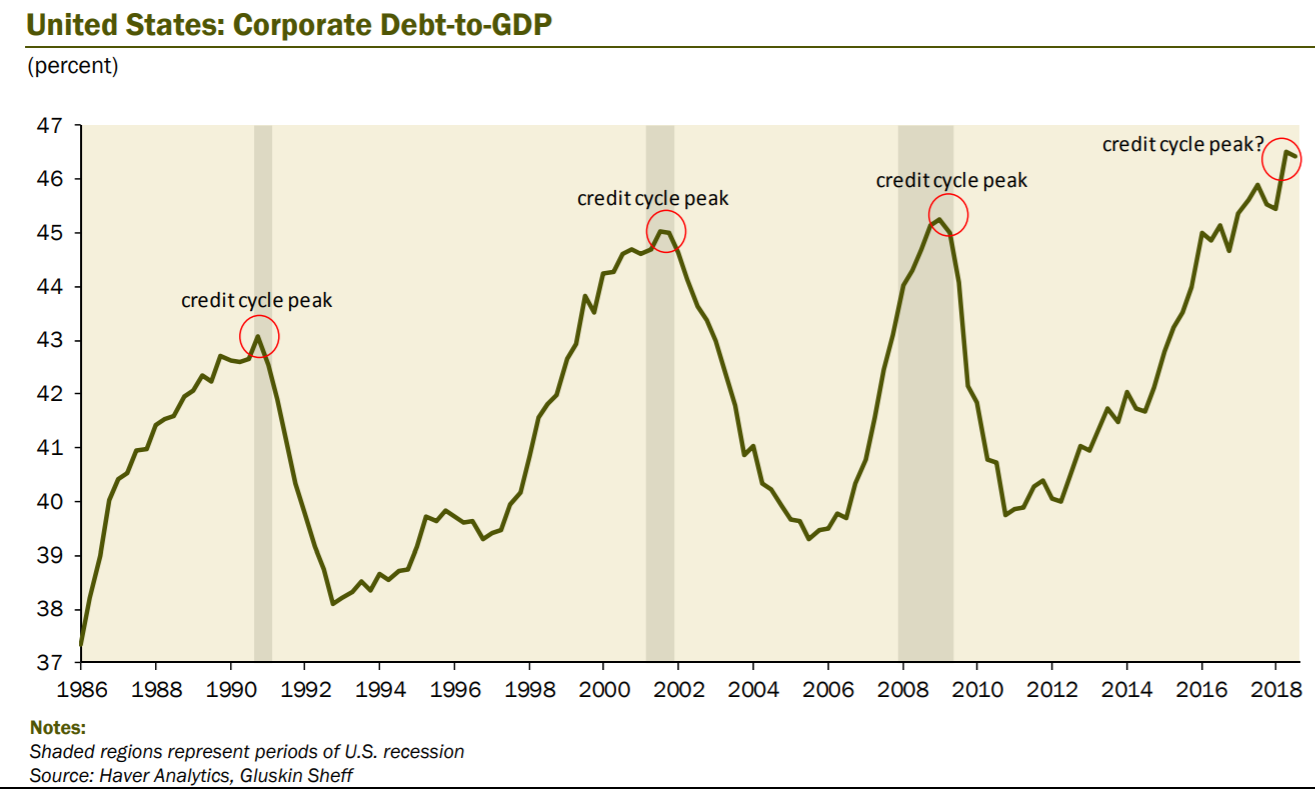

Problem #4 with interest rate argument: Corporate debt

I won't go into the specifics, but the way most analyst's discounted valuation models work, a higher debt rate serves to decrease the discount rate and make the valuation higher.

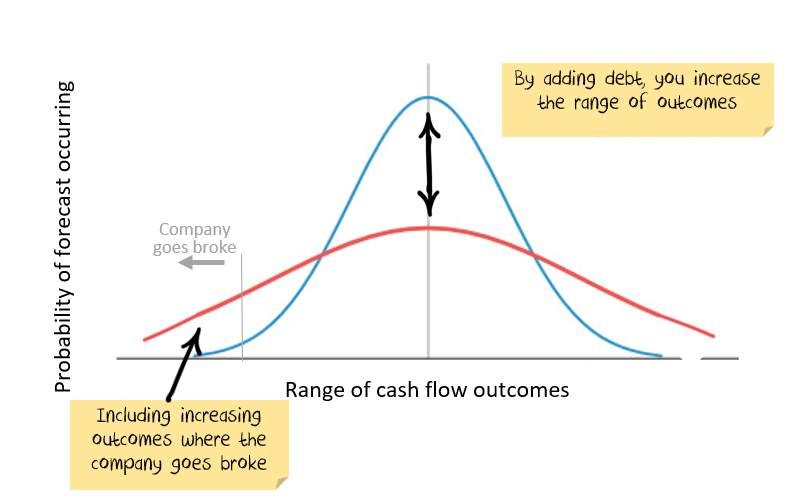

There is a reasonable basis for this with low or average debt levels. Corporate debt is not low or average; it is high:

More debt changes the likely distribution of cash flows. It turns the distribution from a more even set of outcomes to give both a wider range and a higher likelihood that companies go broke:

So, when there is a lot of debt and the growth rate falls, then the chance of companies going broke increases. i.e. the effect of lower growth on likely outcomes is different depending upon how much debt is in the system.

Net effect: If corporate debt is too high, then the market risk premium should also be higher, offsetting some of the valuation impact of lower interest rates.

Problem #5 with interest rate argument: Negative outcomes

People don't like to lose money. Numerous studies show the psychological pain of loss is higher than the pleasure of gains.

In a big picture sense, you will be prepared to pay a certain price for a volatile investment where you expect a return of 7%, but can reasonably expect the outcome to be between (say) 0% and 14%.

If you now lower the expected return to be 4%, the range is -3% to 11%. Arguably you should weight the greater risk of negative outcomes more heavily, and so increase the market risk premium.

Net effect: If expected returns are low, then the market risk premium should be higher, offsetting some of the valuation impact of lower interest rates.

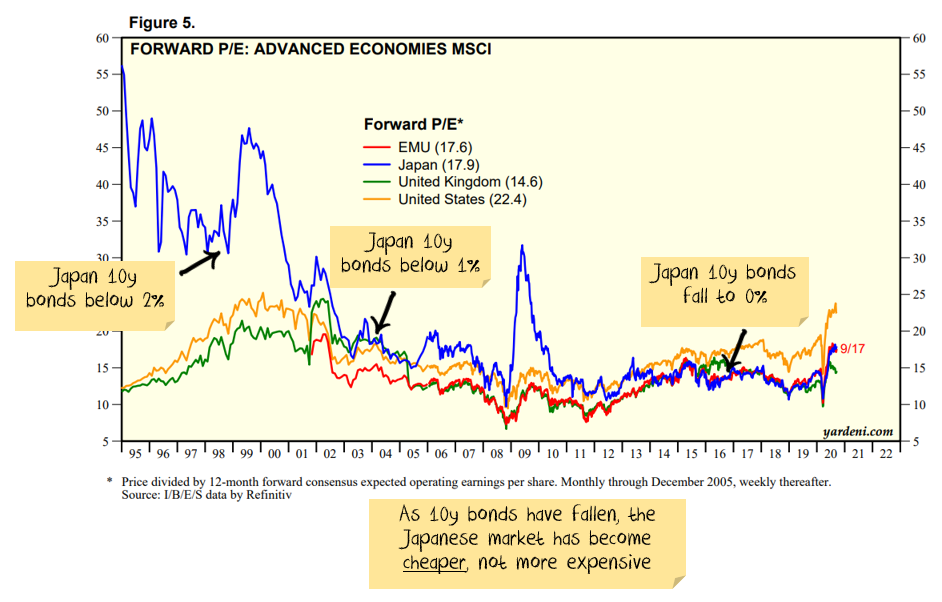

Problem #6 with interest rate argument: Japan

This is complicated by the fact that Japan was in a stock market bubble as interest rates started fall.

But, if anything, the experience in Japan was that lower interest rates led to lower share market valuations, not higher.

Net effect: Lower interest rates in Japan have led to lower valuations.

Exceptions to the rule

Every rule has an exception. In this case, if interest rates are to remain lower for longer but you can find a company with stable earnings, little debt and a decent growth rate, then there is an argument for higher prices driven by lower interest rates.

There are a reasonable number of stocks in the tech sector where this logic applies. There are also a large number of stocks in the tech sector trading as if it were true even though it isn't.

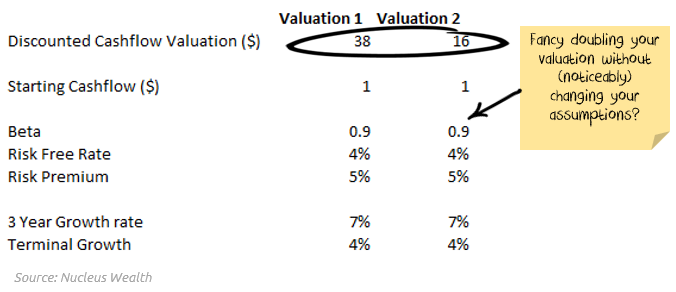

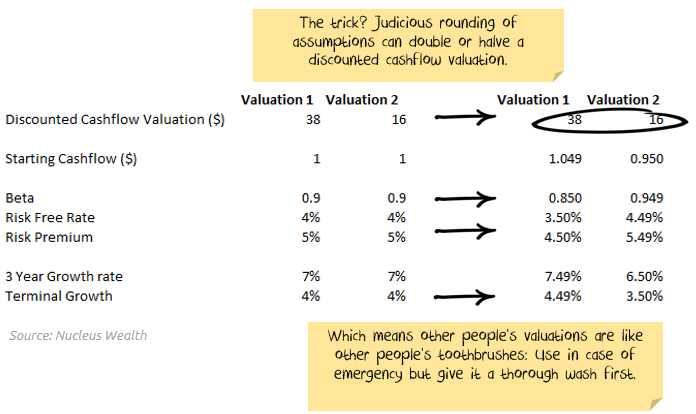

One more aside on discounted cash flow valuations

From an earlier post, a reminder that discounted cash flow (DCF) valuations are really, really easy to manipulate to get just about any answer you want:

Final word on lower interest rates

To the surprise of some, more bad economic news does not mean that stocks should go up.

I disagree with, but can at least understand the arguments that say markets should be higher because either:

- governments and central banks have overstimulated in the short term and there is too much money in the system

- there will be a sudden recovery in the economy

But, I can't understand those who justify rising stock markets solely on the back of a worse outlook for long term interest rates.

Like this wire? Let us know by hitting the 'like' button to the left.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

........

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd - AFSL 515796.

4 topics

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Damien runs asset allocation and global stock portfolios for Nucleus Super, Nucleus Ethical and Nucleus Wealth. His 25 year+ career includes Global Quant at Schroders, Strategy at Wilson HTM & co-founder of Aegis.

Expertise

Comments

Comments

Sign In or Join Free to comment