Some Thoughts on Asset Prices

This time last year we outlined some thoughts on Australian house prices and noted the premium at which dwellings in this country traded relative to historical averages. In this paper we position this analysis within the context of global asset prices.

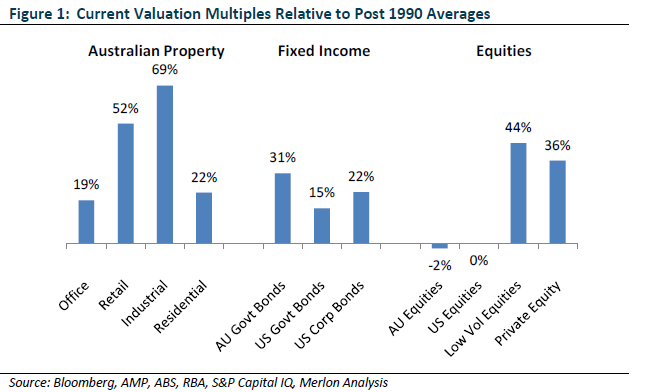

The issue of high asset prices is not isolated to Sydney houses. Other global cities have experienced similar price appreciation and most asset classes – with the notable exception of listed equities – are trading well above historic norms.

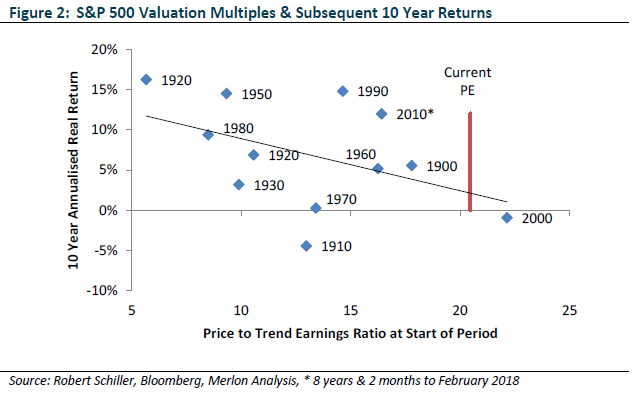

Forecasting a widespread correction in asset prices is highly speculative in our view. Similarly, while there is a loose correlation between market wide valuation multiples and subsequent returns, we think forecasting long term returns is equally futile.

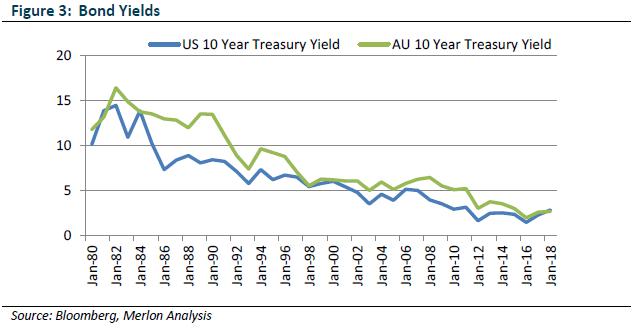

That said, it is clear to us that assets prices have benefitted from low interest rates and that asset prices are vulnerable if expectations of low and stable inflation turn out to be wrong.

Of course, we could be worrying about nothing in which case listed equity valuations will probably catch up to other assets. Either way, we think a portfolio tilt towards listed equities is sensible in the current environment.

Interest Rates & Inflation – A Long Term Perspective

A key driver of currently high valuation multiples appears to be the complacency among many investors that interest rates will remain low for an extended period of time. The corollary of this is that inflation expectations will remain low and stable for an extended period of time. This is because perceived certainty about inflation creates perceived certainty about a bond’s real return, making the bond a less risky investment.

Much of our value investing philosophy at a stock level is premised on the behavioural tendency of investors to over-extrapolate short term trends too far into the future and ignore the lessons of longer term historical periods. Investors come up with new rules for the new world and are quick to dismiss tried and tested valuation frameworks.

This is an example of what psychologists call the “availability heuristic”, or our tendency to heavily weigh our judgements towards more recent information, making new opinions biased toward that latest news.

When we discuss and consider individual company investments at Merlon we always view current conditions within the context of the long term. This is always at least 10 years but preferably longer, particularly when it comes to macroeconomic conditions. This helps us avoid falling into the trap of placing too much weight on current conditions.

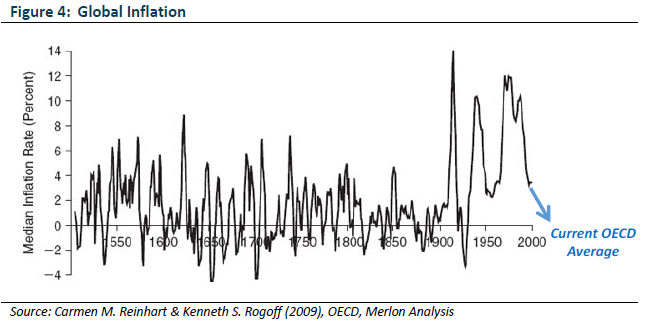

In the case of inflation, there are centuries of data to consider. What we would note is that high and volatile inflation is the norm and the current environment is highly unusual.

There have been many reasons postulated as to why such conditions might prove sustainable:

- Dr Philip Lowe, Governor of the RBA recently commented that officials were still trying to figure out what the new “normal” level of interest rates might be, because wages growth and inflation were not behaving as they have in the past.”;

- Central banks have postulated that increased life expectancy and an aging population put downward pressure on real interest rates as people build up higher savings;

- Others have suggested that technology means most economies would struggle at times to achieve sustainable inflation rates of 2% or more over the medium run.

Stepping back from some of the miniature, history shows how difficult it is for the world to escape periods of high and volatile inflation. The underlying cause is debatable and arguably academic. Having said that, weak institutional structures and a problematic political system, have always made monetary stimulus and external borrowing tempting devices for governments to employ to avoid hard decisions about spending and taxing.

Current Inflationary Pressures

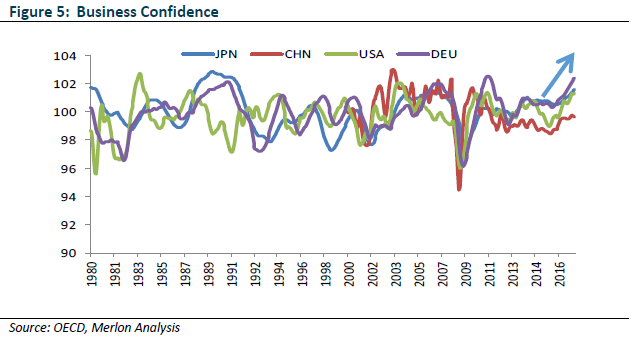

Turning to the current environment, it is worth noting that a number of factors that have served to depress inflation in recent years appear to be receding. First, global economic growth is synchronised and accelerating. In particular, business confidence is improving which would typically be associated with higher demand for labour and capital goods. This lift in demand may well flow through to higher prices.

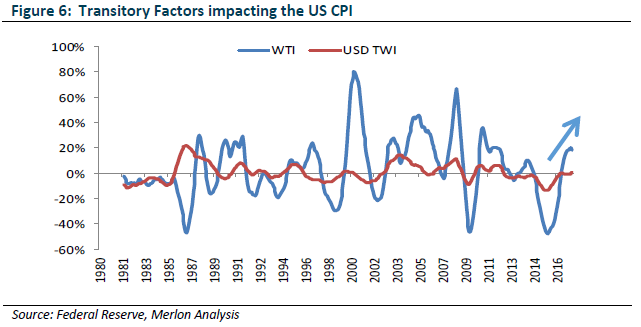

Second, there have two critical cyclical factors that have dulled CPI growth in the US in recent periods being the falling oil price and the strong US dollar. Both these trends have reversed. Additional deflationary impacts have also been felt from owners equivalent rent, health and communications. Again, a normalisation of these components will lead to a notable pick up in the rate of growth of the CPI.

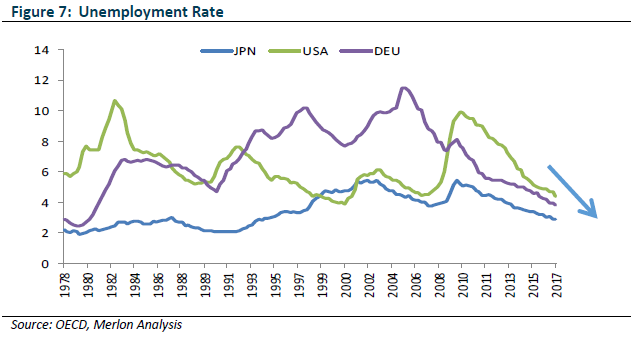

Third, major economies are approaching historically low unemployment. At some point low unemployment will create wage pressures as businesses seek to entice new workers into the labour force.

In addition to these aspects is the significance of Trump’s massive fiscal stimulus in the US. These measures were only just passed, are not reflected in any of the data presented and the quantum of these initiatives at a time when the world economy is growing and where capacity utilisation is tight is unprecedented. Trade barriers will only serve to drive up US wages and inflation.

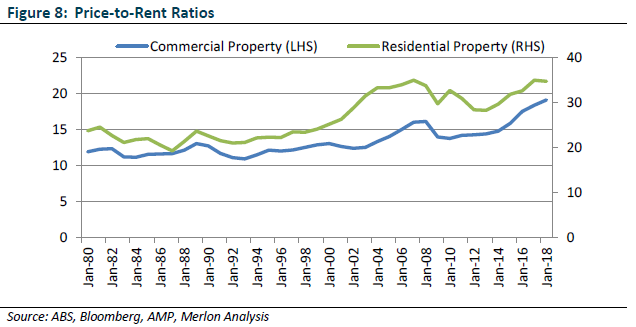

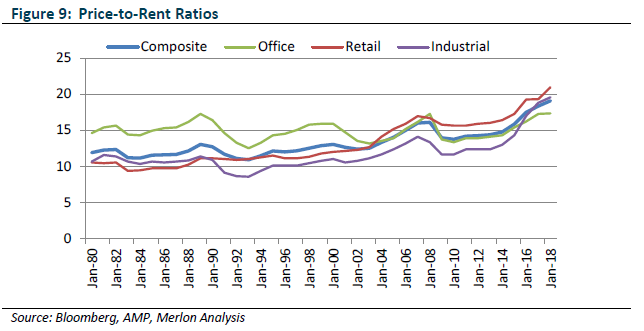

Commercial Property could be More Expensive than Residential

While there has been much focus on residential property in recent years, the rapid increase in commercial property prices has been less well publicised. We note that while residential property is passing hands at a price-to-rent ratio that is approximately 20% above its post 1990 average, commercial property is trading at around a 30% premium.

This commercial property price inflation has been most conspicuous in the “industrial” category. This is particularly concerning to us given the lower lead times in adding supply in this category and the often enormous incentives provided to new tenants, particularly during economic downturns.

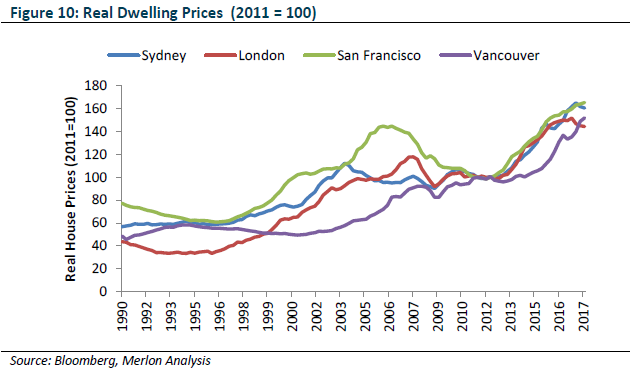

A final point to note about residential house prices is that Australia – and Sydney in particular – is not that unusual when compared to other global cities with geographical constraints to growth. In short, booming asset prices are a global phenomenon. If we go down, we may all go down together.

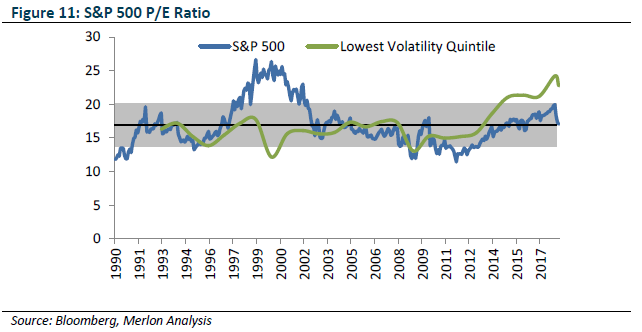

Divergent Equity Valuations

Aggregate equity market valuations are broadly in-line with recent historical averages. However, there are key components that appear very expensive. In particular we observe the recent inflation in “low volatility” stocks. These stocks are often viewed as the least risky option for investors seeking equity market exposure and include a number of REITS which, as we have already discussed, appear expensive relative to historic norms.

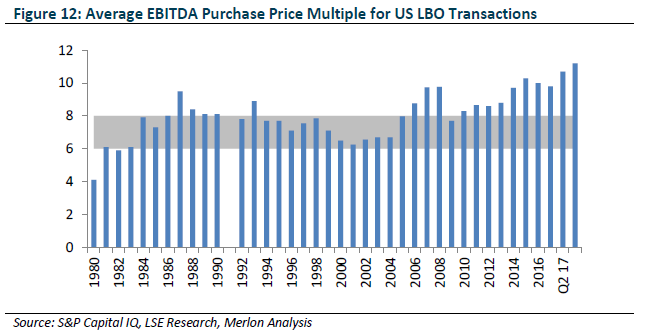

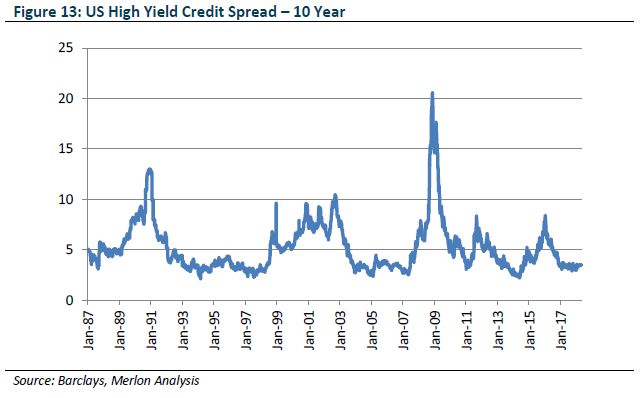

Another trend has been investors seeking exposure to unlisted assets as means to avoid market volatility. This too looks like a crowded trade with private equity multiples excessively high compared to historic averages and compared to listed equities.

This trend is arguably symptomatic of cheap funding with credit spreads at cyclically depressed levels.

Merlon Perspective

Since we founded Merlon in 2010 we have consistently valued businesses on the basis of sustainable cash flows discounted at sustainable interest rates and sustainable risk premiums. We do not subscribe to the view that inflation is permanently lower than it has been in the past but even if we did we would not be positioning the portfolio differently as we think it would imply the parts of the Australian equity market to which our portfolio is exposed are absurdly undervalued compared to bonds, property and so-called “low vol” equities.

Our approach has increasingly positioned us away from many of the sectors that have benefitted from falling interest rates which has created a short-term headwind for our investors. We think this will reverse in time, at least in a relative sense.

For more insights from Merlon Capital Partners please visit our website (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Hamish joined Merlon Capital Partners as a Principal in July 2010. He was previously Head of Research, Asia Pacific Equities at AMP Capital Investors. Hamish holds a MBA with honours from The Wharton School, University of Pennsylvania.

1 topic

Hamish joined Merlon Capital Partners as a Principal in July 2010. He was previously Head of Research, Asia Pacific Equities at AMP Capital Investors. Hamish holds a MBA with honours from The Wharton School, University of Pennsylvania.

Expertise

Hamish joined Merlon Capital Partners as a Principal in July 2010. He was previously Head of Research, Asia Pacific Equities at AMP Capital Investors. Hamish holds a MBA with honours from The Wharton School, University of Pennsylvania.

Expertise

Comments

Comments

Sign In or Join Free to comment