Speedy return to economic normalcy?

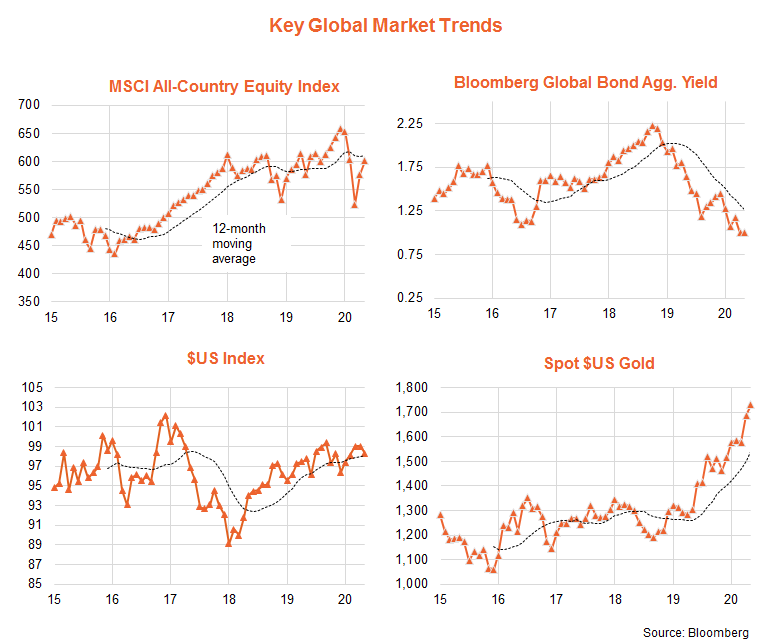

Global equities pushed higher in May, continuing the rebound of the previous month, reflecting ongoing hopes of a speedy return to economic normalcy as both new COVID-19 cases and social distancing restrictions eased further in most advanced economies. Risk-on sentiment contributed to an easing in the U.S. Dollar, though bond yields held steady and gold prices rose further.

The MSCI All-Country World Equity Return Index rose by 4.3% in local currency terms, after a gain of 10.4% in April. As seen in the chart set below, global bond yields remain in a strong downtrend*, and gold prices in a strong uptrend. The previous uptrend in $US has levelled off into a choppy range over recent months. Global equities have effectively been in an extended choppy range since early 2018.

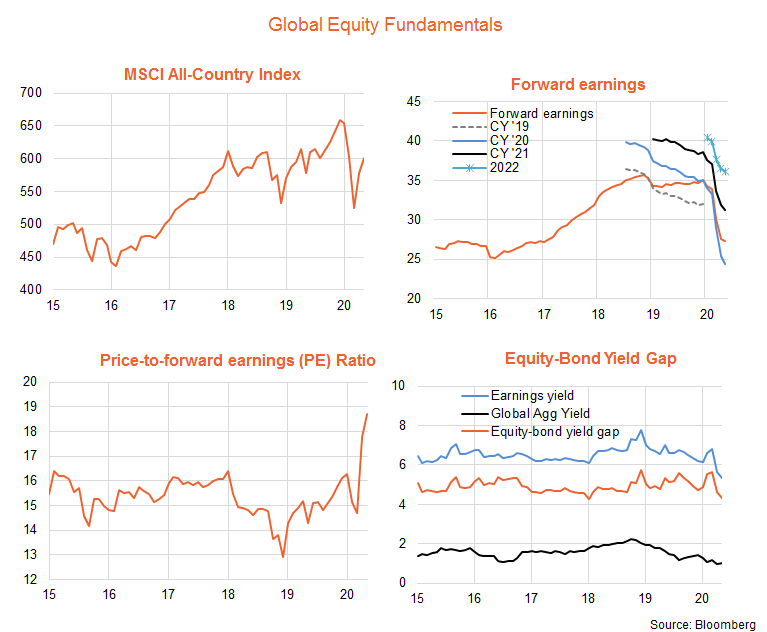

Global equity fundamentals – bond yields support high valuations

As seen in the chart pack below, the rebound in global equities – at the same time as earnings expectations having fallen sharply – has pushed the price-to-forward earnings ratio to a relatively high 18.7 (compared to a longer-run average of 14.0). As yet there appears little sign of a levelling out in earnings expectations. According to Bloomberg consensus analyst estimates, global earnings are now expected to decline by 24% in CY’20, following by a strong 28% rebound in CY’21.

That said, with the yield on the Bloomberg Global Aggregate Bond Index holding steady last month at around 1%, the equity-to-bond yield gap (EBYG) (a measure of relative valuations) narrowed to 4.3%, which remains only modestly below its average of 4.9% since 2005. In short, while outright PE valuations appear very high and face upward pressure given that earnings will likely be revised down further over the coming months, continued very low bond yields are providing some relative valuation support.

Global equity trends – health care, gold, and technology

Across BetaShares’ currency-hedged global equity sector/thematic funds, Japanese equities enjoyed a strong month, with HJPN‘s Index returning 6.5%. Global gold miners (MNRS) and health care (DRUG), however, remain the strongest relative performers**. Among BetaShares’ unhedged global equity sector/thematic funds, both global cybersecurity (HACK) and robotics and artificial intelligence (RBTZ) had an especially strong month, with their indices returning 11.9% and 10.4% respectively. More broadly, Asian technology (ASIA) and the tech-heavy NASDAQ-100 Index (NDQ) remain the top two strongest relative performers, with RBTZ now in third place.

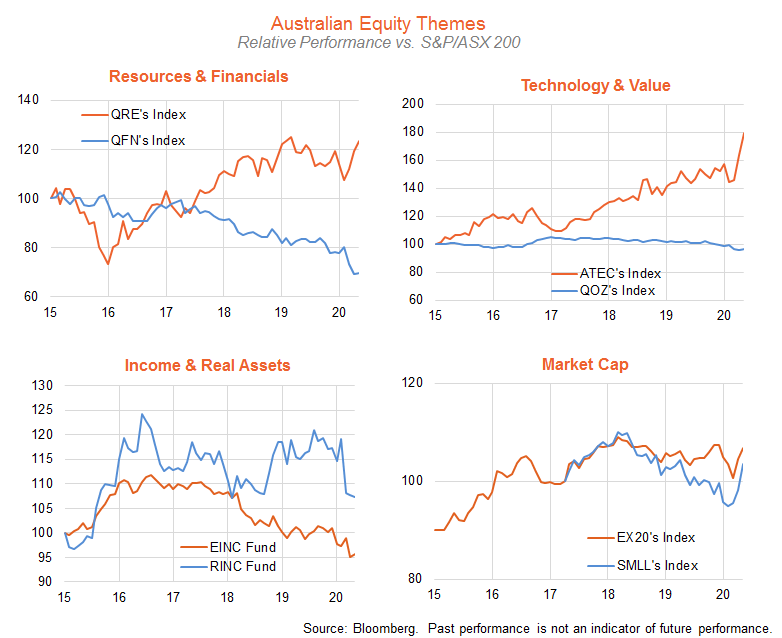

Australian equity trends – technology and resources

Among BetaShares‘ Australian equity sector/thematic funds, technology (ATEC), resources (QRE) and small caps (SMLL) produced further strong gains in the month, and are the top three relative thematic performers. Indeed, ATEC’s Index returned 14.7% in May after a 22.2% return in April. Financials and property-related exposures remain the weakest performers.

Cash and bonds – government yields drop, credit spreads widen

A modest decline in government bond yields, and further narrowing in credit spreads, saw fixed-rate bonds marginally outperform cash (AAA) in the month, especially those with longer duration and credit exposure, such as AGVT and CRED. Narrowing credit spreads also contributed to stronger gains for hybrids (HBRD) and floating-rate bonds (QPON) over cash in the month. Government bond yields remain low compared to their average of recent years, supported by low inflation and very accommodative monetary policy. Credit spreads remain well above their lows of the past two years, though closer to their average over the past five years.

Never miss an insight

Each week I will publish my latest thoughts on the macro events shaping the ETF landscape. To be the first to read my insights, hit the follow button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

4 topics

1 contributor mentioned

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment