Stimulus leads the way to a housing recovery

Bella Kidman

Livewire Markets

In our previous collections piece, our trio of residential housing experts explained the state of play for the Australian housing market after the detrimental impact of COVID-19.

To recap their views, it may not be as bad as you think. Housing markets may just be on a road to recovery, and this is the perfect time to capitalise on this.

In part two of this three part collection, our experts will discuss the key drivers behind the housing market's downfall and recovery. Taking into consideration current interest rates, consumer sentiment and recession risks, they will analyse how (or if) the property market could recover. Additionally, observing the extension of government stimulus, border closures and mortgage holidays, our experts will assess the important factors that the market has overlooked.

Responses come from:

-

Pete Wargent, Buyers Buyers

- Shane Oliver, AMP Capital

- Doron Peleg, RiskWise Property Research

If you can't spend your money elsewhere, it's time to spend on a house

Pete Wargent, Buyers Buyers

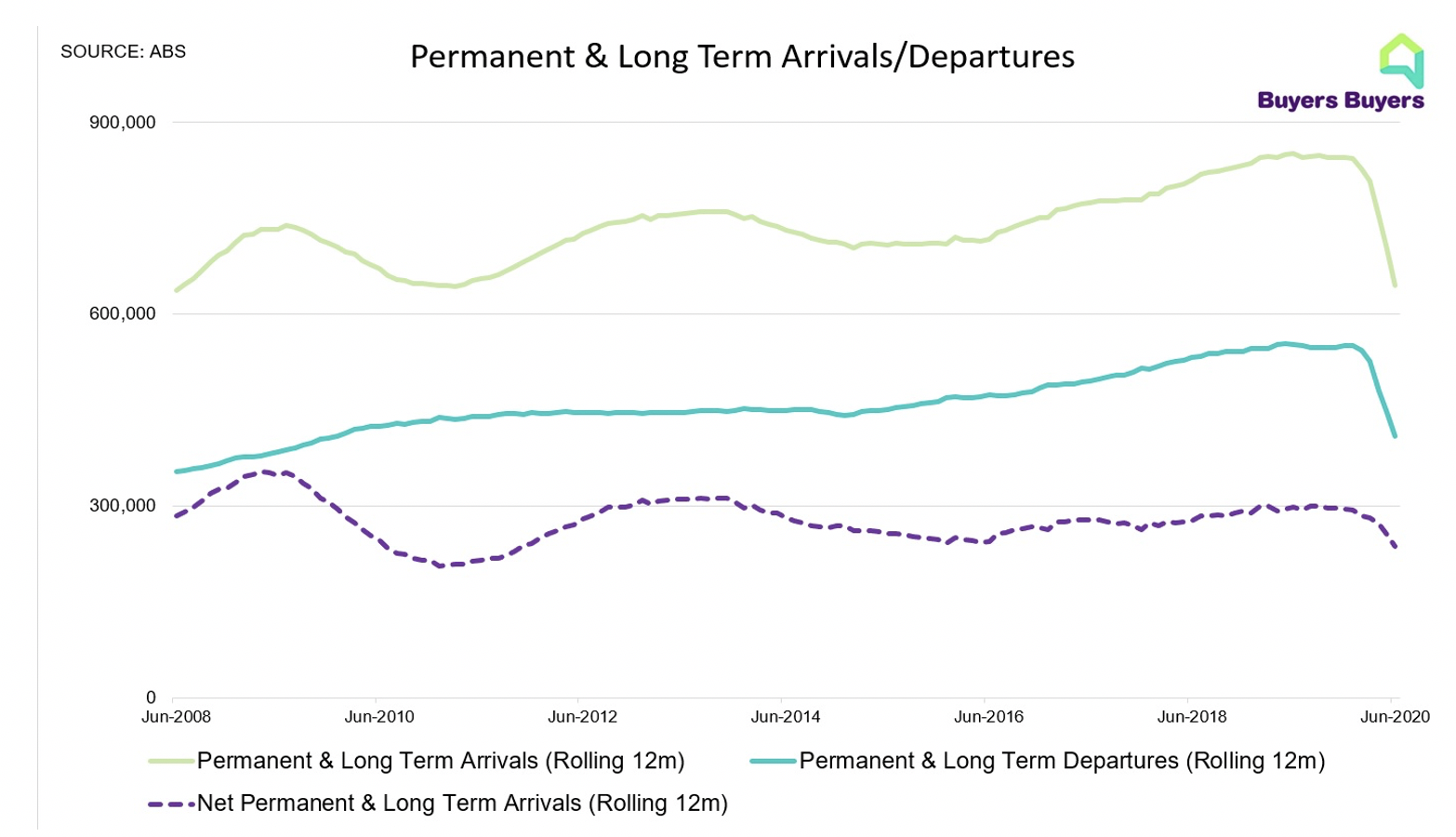

Yield curve control and record low mortgage rates are set to support housing prices, but transaction activity and construction will inevitably sink lower, with border closures having severely limited net overseas migration.

The prevailing demographic trends have been dramatically disrupted in 2020, with few would-be travellers able to either enter or leave the country.

In terms of headcount, annual growth in the estimated resident population will likely slow from around 1½ per cent to about ½ per cent this year, effectively representing the natural growth in the population (i.e. births minus deaths).

Not only are tourists and prospective permanent migrants unable to enter the country, Australians are largely not permitted to leave the country either.

This has led to some extraordinary retail trends, with Australian residents unable to holiday overseas - or spend as much in cafes, restaurants, cinemas, and theatres - and thus becoming inclined to spend 30 per cent more than a year earlier on household goods, including white goods and furniture.

Early access to superannuation and the HomeBuilder incentives have also helped to spark to a mini boom in vacant land sales, especially in south-east Queensland.

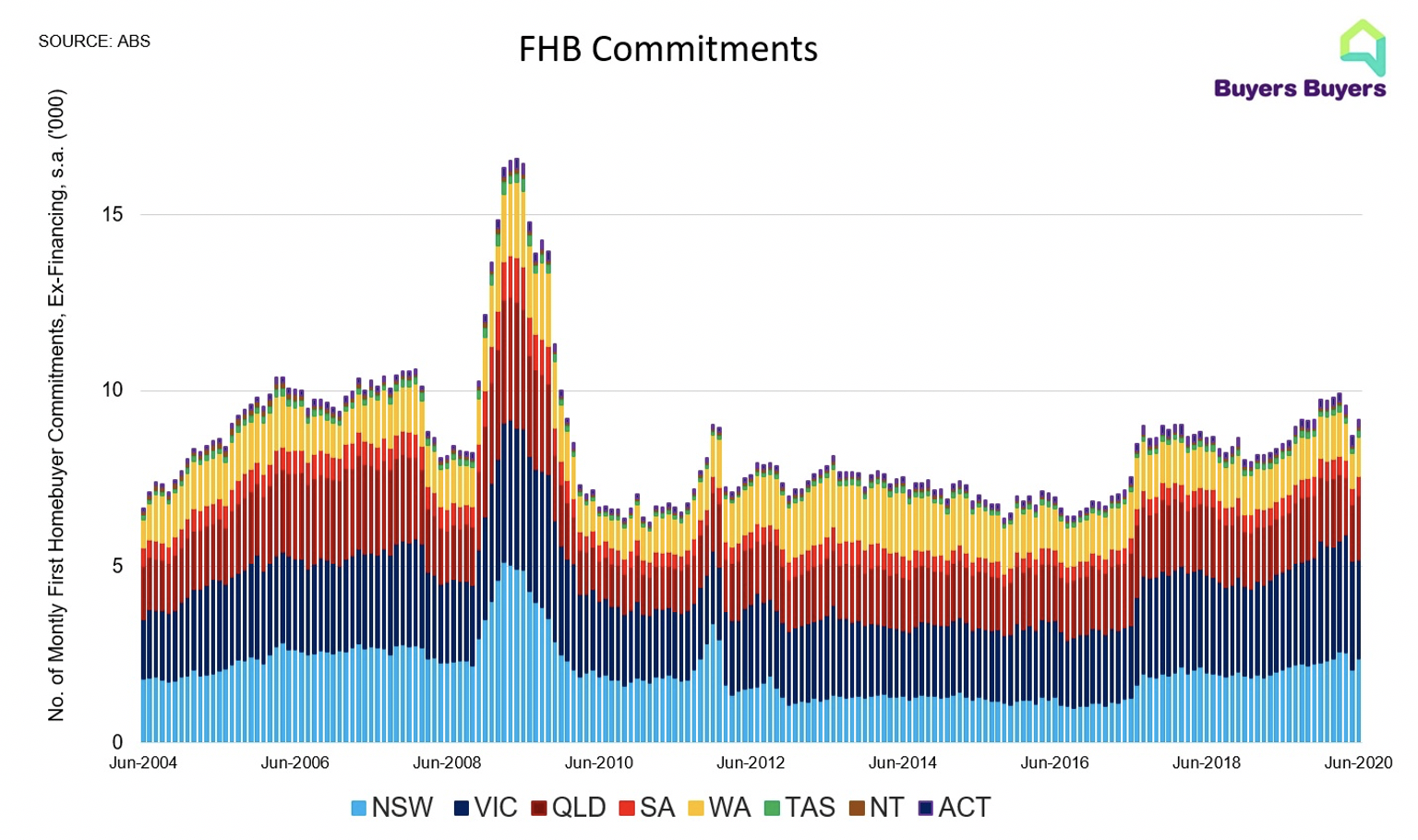

Moreover, incentives such as the latest round of the First Home Loan Deposit Scheme (FHLDS) for low deposit borrowers, which has experienced a rapid application take-up since 1 July 2020, mean that first homebuyer numbers will soon reassert their uptrend in H2 2020 and ascend to the highest levels since the equivalent Rudd stimulus.

Australia has a strong demographic pyramid thanks to immigration patterns through the resources boom years, and about one-third of our enquiries this year have been from first homebuyers.

Government incentives will often encourage many buyers in the 25 to 35 age cohort into the new apartment market, but first-time buyers would be well encouraged to undertake very thorough due diligence and understand the potential for a heightened risk of loss on resale.

Investor activity has also begun to rebound from May’s lows in response to record low mortgage rates – with some mortgage products now being available from rates with a 1-handle for the first time in Australia - but the weakness in rents and in the high-rise unit market more broadly will likely limit investor credit growth in aggregate.

Immigration levels are key

Shane Oliver, AMP Capital

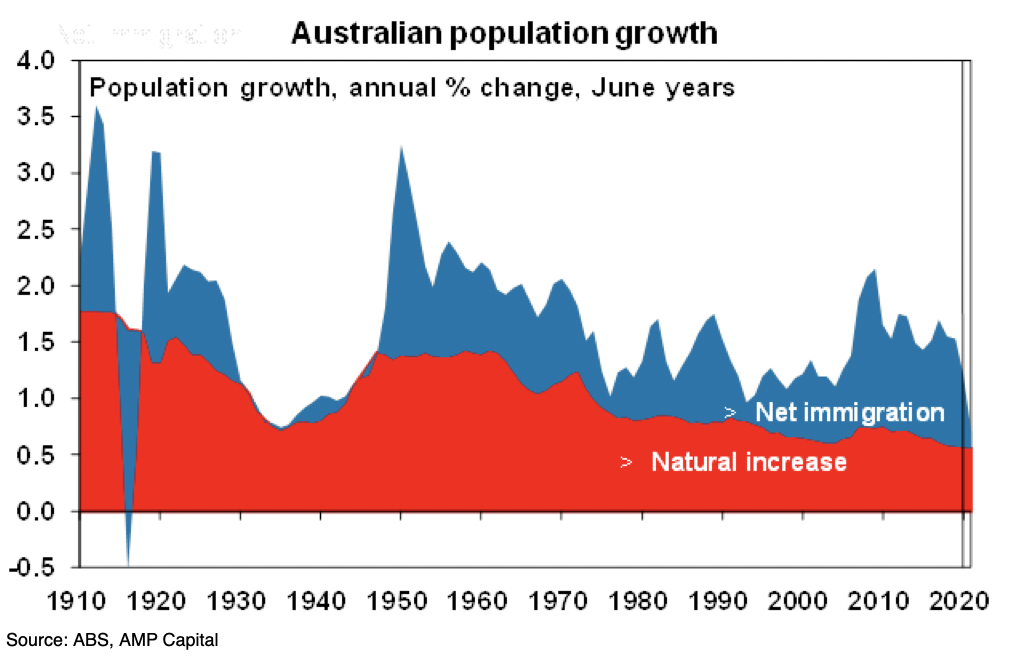

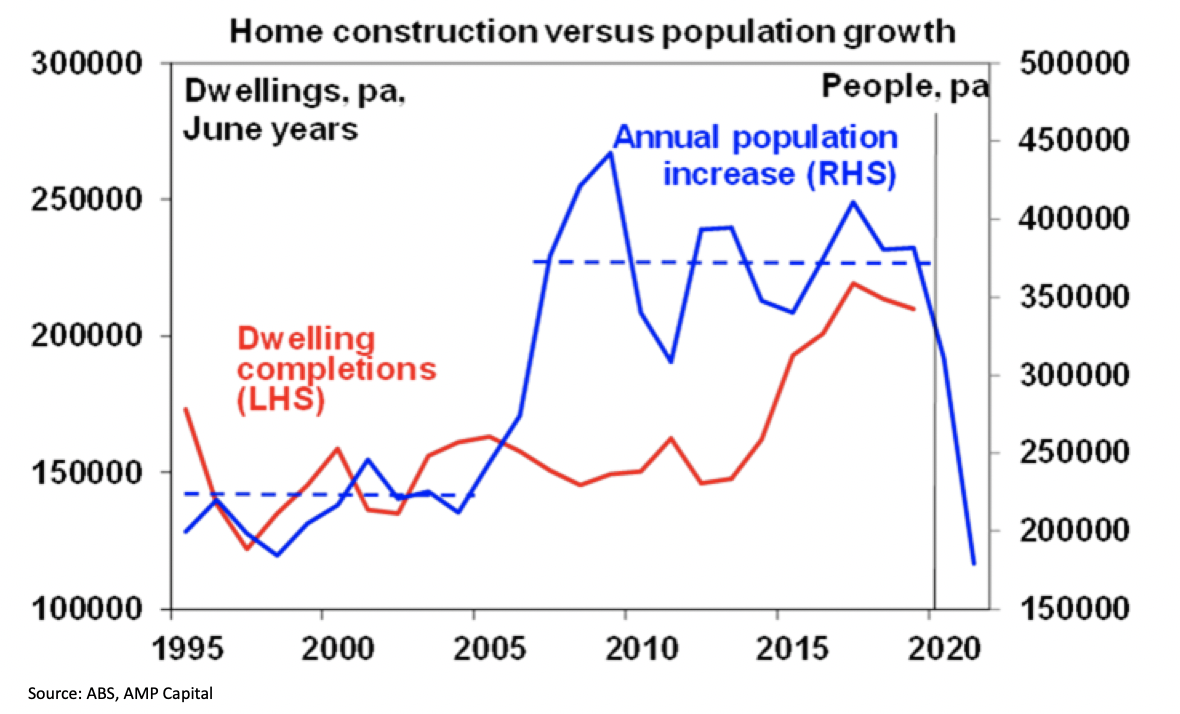

The Australian residential property market is currently in a bit of a twilight zone. Record low mortgage rates are a big positive but they are more than offset by the surge in underlying or effective unemployment to now around 10% on our estimates, the hit to consumer confidence, falling rents, and a reduction in underlying demand of around 80,000 dwelling per annum thanks to the hit to immigration. The latter is critically important and its ramifications are being underestimated by much of the commentary and discussion around the property market. For the last 15 years or so population growth has led to underlying housing demand well in excess of new supply and this has led to chronic poor housing affordability – basically a surge in prices (and household debt) relative to incomes. But due to the hit to immigration, population growth this year is likely to be just 0.7%, which will be its lowest since 1917!

The associated hit to underlying housing demand means that after years of underbuilding relative to population driven demand, we may now be heading into a period of oversupply.

With unemployment likely to remain high for some time to come it is hard to see the Government being able to quickly return immigration to pre coronavirus levels.

Were it not for JobKeeper, the increase in JobSeeker, the bank payment holiday and other support measures protecting heavily indebted households and property investors, prices would be falling more rapidly in response to forced sales. As a result we are still in a bit of a twilight zone as support measures help protect the property market and keep price falls gradual. The support measures will gradually start to be wound down from October a time when high unemployment and reduced immigration will remain. This in turn will mean downwards pressure on property prices into 2021.

Government support measures for the property market directly are all aimed at encouraging new construction – ie the HomeBuilder Scheme and stamp duty concessions for first home buyers of new properties – these may help developers and home builders but they are likely to divert demand away from existing properties and potentially keep supply higher than it otherwise would be or may need to be in the phase of the collapse in immigration.

Now is the time for first time home buyers

Doron Peleg, RiskWise Property Research

Government incentives such as the First Home Buyers Deposit Scheme, the avoidance of Lenders Mortgage Insurance (LMI), as well as stamp duty exemptions all help to put buyers in a good position. Lower interest rates also materially improve housing affordability in terms of serviceability ratio, i.e. the monthly repayments for any price point are simply lower.

What this all means is now is the time to buy if you are a first home buyer or an owner-occupier with a secure job, as this current slowdown in the property market is only temporary, with houses in popular areas likely to experience solid capital growth in the medium to long term.

Once the COVID-19 issue is resolved, most likely in 2021, the traditional connection between low interest rates and increase in dwelling prices is likely to take place. However, investors buying rental apartments unsuitable for families are taking an enormous gamble, with both equity and cash flow risk expected to materially increase. Serviceability is also a major factor for investors who rely on a stable rental income to cover the costs associated with property and particularly the mortgage. This is especially the case in areas of oversupply, Brisbane inner city being a prime example where there are 5,431 units in the pipeline, making up an addition of 5.9 per cent of the current stock.

COVID-19 has only served to increase the risk. Currently, there are a large number of high-rise properties being offered to a smaller number of investors. This is because there are less investors in the market mainly due to the pandemic.

Investors should simply time the market, do nothing and wait for dust to settle before they buy, and they should choose the property they purchase carefully. This simply means that investors should focus on family-suitable properties and if they have limited budget to simply look for more affordable areas that enjoy good ‘fundamental’ demand for houses, such as Geelong. While the rental return is lower, the capital growth is materially higher and, therefore, in the medium to long term, the overall return for houses is higher than units. Houses obviously, carry a significantly lower level of risk, as land scarcity mitigates the potential for oversupply in most areas with good access to the major employment hubs.

It is important to note that even following the 2019 election results, when things had settled down in the property market, it took time for things to get back to normal.

Once the pandemic is finally over, prices will not increase by 10 per cent within a month. It will definitely take some time for buyers to gain confidence and ‘pull the trigger’. Which means investors have time to make the decision whether to buy a property.

However, it should be noted that houses carried significantly lower risk because generally the cohort of renters, especially in the more established suburbs, comprised families and, in many cases, those with permanent full-time jobs. They are also more likely to deliver good medium and long-term capital growth.

Additionally, as rental properties are not fully substitute products with owner-occupied dwellings, there is inherent risk associated with them as they did not appeal to families looking for three bedrooms, with outdoor space, close to schools, transport and employment hubs.

Looking for more on residential property?

Don't forget to read the previous chapter - Buying property during a recession? Not as crazy as it sounds - in this Collections series here. Click follow below to be notified when I publish content in future.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bella is a Content Editor at Livewire Markets.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

1 topic

2 contributors mentioned

Bella Kidman

Content Editor

Livewire Markets

Bella is a Content Editor at Livewire Markets.

Expertise

Bella Kidman

Content Editor

Livewire Markets

Bella is a Content Editor at Livewire Markets.

Expertise

Comments

Comments

Sign In or Join Free to comment