TOL - 3rd Aug, 2022

Stocks don't always fall when rates rise: 10 reasons why some active funds underperform

Stock markets always dive after interest rates rise, right? Wrong. Global stocks rise by an average of 9.2% in the 12 months after a US Federal Reserve rate hike, according to a recent study conducted by the Bank of America.

The finding is one of several published in the report, authored by Bank of America’s global analyst team, including Nigel Tupper, Girish Nair, Amar Vashi, and Sumuhan Shanmugalingam. It outlines 10 reasons why active funds tend to underperform – as mentioned in a recent Australian Financial Review article.

Inexpensive Quality and Global Earnings Revision Ratio

The 10 reasons are:

- Assumptions about alpha generation. Some investors devise an investment philosophy and process without any evidence it consistently adds alpha.

- Assumptions about how markets react to events. "If rates rise then markets must fall, right?"

- Static allocation. "We buy quality stocks that are inexpensive, and never deviate."

- Focus on bottom-up alone. Many investors ignore the direction of the cycle which is a major determinant of which stocks outperform at any point in time.

- Risk aversion. Many investors are not willing to add enough cyclicality to a portfolio in an upturn. "Low-quality stocks can implode and it's difficult to get out quickly". Investors often prefer to remain in quality and underperform than have exposure to lower quality and outperform in upturns.

- Unintended exposures. Many investors focus on portfolio exposure to stocks, sectors, and countries and ignore exposure to style, the cycle, interest rates, bond yields, currency, oil, beta allocation, sentiment, news, positioning, products, geographic revenue, and more.

- Extrapolating investment lessons from the US. Many investors assume what works in the US works in all markets (even though that's not always the case).

- Basis risk. Funds often avoid some stocks in an index ("not liquid enough", "not green enough"). Funds underperform if what they don't own outperforms.

- Cash. Funds hold cash but an equity index includes 100% stocks. Markets rise more often than not, so cash tends to drag on relative performance.

- Transaction costs. There are no transaction costs associated with an index.

The report is part of Bank of America’s Global Quantitative Strategy research, using the institution’s monthly Quant Panorama report as source material. This looks at how consensus expectations for corporate earnings have changed over the long-term versus the market, and whether earnings revisions are reflected in relative share price performance.

“Keep in mind that every cycle is different and markets may respond differently in future. In a scenario in which it takes central banks longer to control runaway inflation, for example, they may have to raise rates more aggressively and for longer than normal. This could push an economy into an economic downturn and markets could fall as central banks tighten policy,” the report notes.

Quality isn’t a sure thing

The report also compares year-on-year performance relative to the MSCI AC World Index of an investing approach that combines a focus on Quality and Value.

“There are times when a certain approach will not be appropriate for the current investment environment and therefore underperform,” The BoA report says.

Inexpensive Quality and Global Earnings Revision Ratio

Pay attention to the cycle's direction

The report's authors suggest many investors focus solely on where we are in the cycle and ignore the direction it’s travelling.

“Investors can add to their performance by positioning in styles for an upturn when the global cycle is improving, and positioning in styles for a downturn when the cycle is slowing. Investors who ignore the cycle may get caught on the wrong side of style rotation which can be dramatic at times (120% in 2020!),” the report notes.

Unintended exposures

When positioning a portfolio, investors often weigh up exposure to stocks, sectors, and countries but ignore other important factors including:

- style,

- the cycle,

- interest rates,

- bond yields,

- currency,

- oil/commodities,

- beta allocation,

- sentiment,

- news,

- positioning,

- products,

- geographic revenue.

“In our experience presenting to fund managers globally, almost no equity fund managers calculate exposure to equity duration, suggesting many funds have unintended exposures in the portfolio,” the report notes.

The following chart shows the relative exposure of Value and Growth funds to rising bond yields.

Exposure to Short Equity Duration: Value vs Growth Funds

These aren’t purely US phenomena

But that’s not to say everything in US financial markets translates into other markets.

“Market structure, market dynamics, and market characteristics differ by region and hence the implementation of any strategy should take these factors into account,” the report notes.

In the US, this strategy has reasonably consistently added to performance in the last 34 years. But implementing the same strategy in Emerging Markets would have underperformed.

Price Momentum (12m - 1m): Price Reversal Strategy: USA vs Emerging Markets

.jpg,https://www.livewiremarkets.com/rails/active_storage/representations/proxy/eyJfcmFpbHMiOnsibWVzc2FnZSI6IkJBaHBBMHA1QWc9PSIsImV4cCI6bnVsbCwicHVyIjoiYmxvYl9pZCJ9fQ==--3528eeb2912a2ddd3c1c5a8add9673c8ea994604/eyJfcmFpbHMiOnsibWVzc2FnZSI6IkJBaDdCem9MWm05eWJXRjBPZ2wzWldKd09oTnlaWE5wZW1WZmRHOWZabWxzYkZzSGFRSmtBbWtDV0FFPSIsImV4cCI6bnVsbCwicHVyIjoidmFyaWF0aW9uIn19--dbcf8d7b6290376ca515990a95f79dcba96deb5c/The%20best%20performing%20Global%20share%20funds%20of%20FY2022%20(1).jpg)

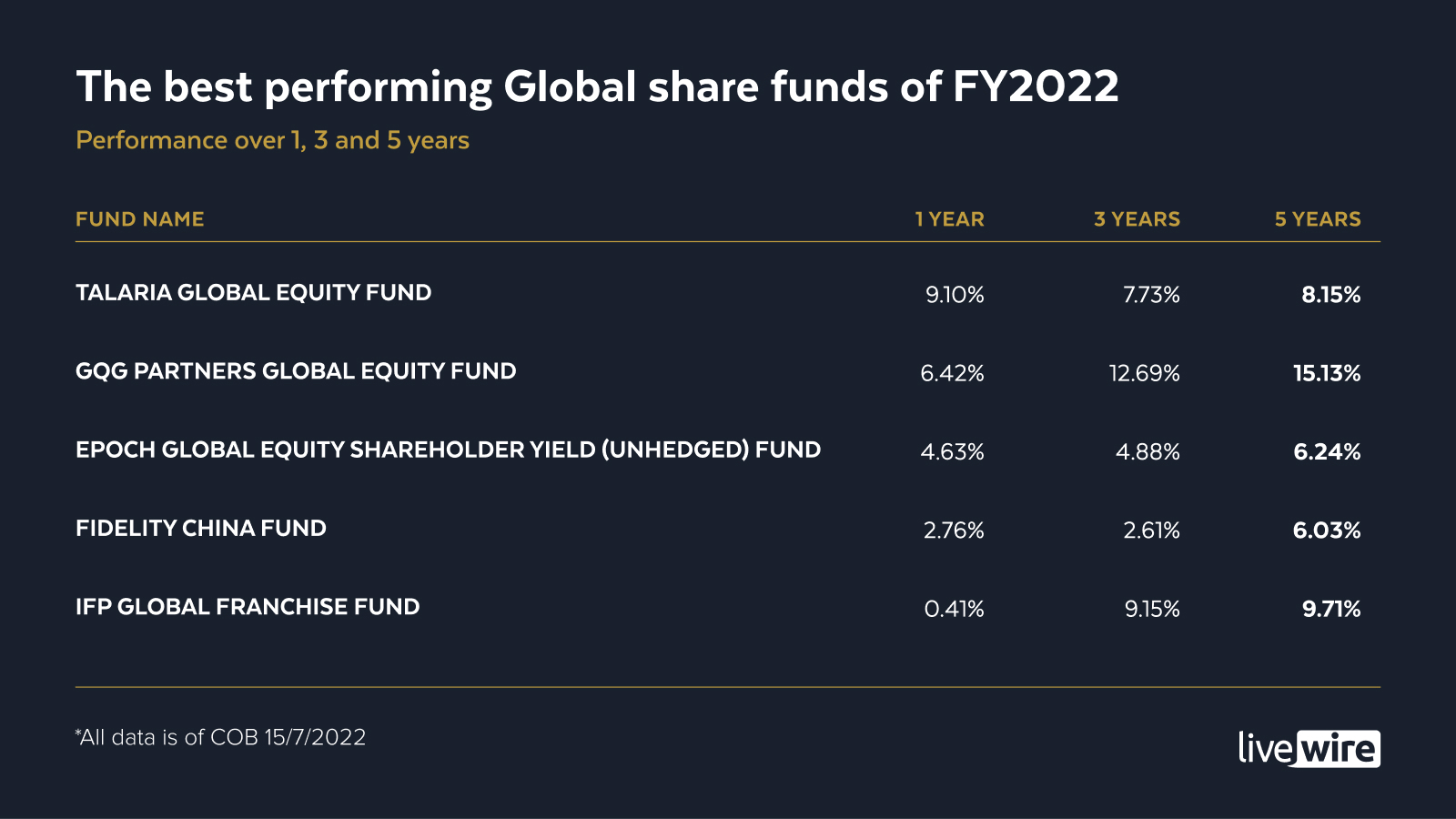

Funds

The top performing global share funds for FY22

View

.jpg)

Funds

The top performing global share funds for FY22

View

NEVER MISS AN INSIGHT

Enjoy this wire? Hit the ‘like’ button to let us know. Stay up to date with content like this by hitting the ‘follow’ button below and you’ll be notified every time we post a wire.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

This is an archived profile. Glenn Freeman was a content editor at Livewire Markets from August 2020 to July 2024.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

3 topics

This is an archived profile. Glenn Freeman was a content editor at Livewire Markets from August 2020 to July 2024.

Expertise

This is an archived profile. Glenn Freeman was a content editor at Livewire Markets from August 2020 to July 2024.

Expertise

Comments

Comments

Sign In or Join Free to comment