Strong outlook for EML in a post-COVID world

EML Payments (“EML”) is a payment processing company with a difference, in that it provides a payment gateway that can be highly customised to the needs of the client. This might be, for example, limiting its use to a specific geographic location (eg a shopping centre), or to specific goods and services, or to a specific delivery method.

The point is that its highly customised payment processing capability means that it can solve the specific problems of each client, and this is naturally highly valued.

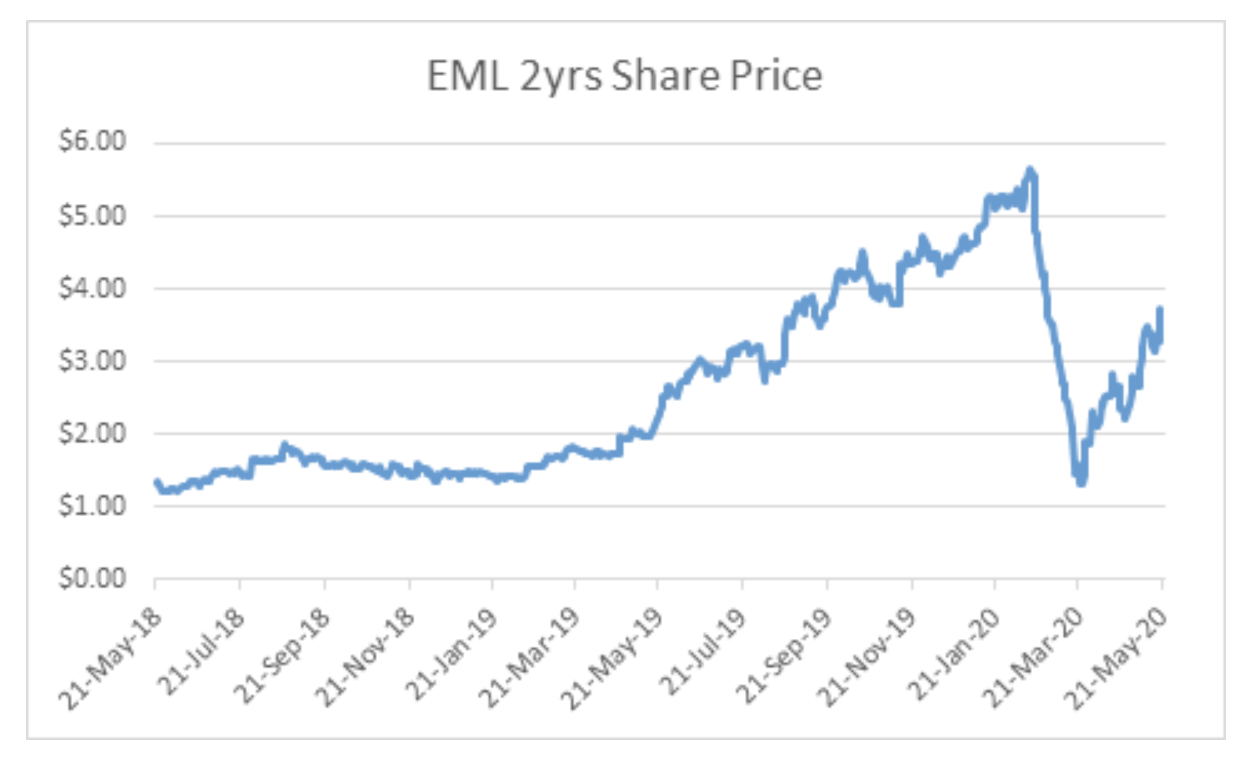

As a result, EML has been able to significantly expand its business both geographically and by the number of customers, leading to strong business momentum. The EML share price has been a strong performer over time, and in particular over the 12 month period leading into COVID-19.

A range of factors drove this performance. EML has demonstrated the value of its business offering with its ability to sign up new customers and launch new programs. This has led to strong organic growth, which has been supplemented by the fact that in many cases the businesses that EML is providing its service to are themselves high growth businesses.

A number of acquisitions have been made over time that have both diversified the business geographically and enhanced its product capability. The most recent and largest acquisition has been PFS Financial, which significantly diversifies the business away from the gift card business that currently dominates EML’s earnings.

Finally, the stock itself has been on a discovery process, off the back of increased broker coverage and EML moving up the market capitalisation scale and coming onto the radar of more investors.

Key events of the last six months

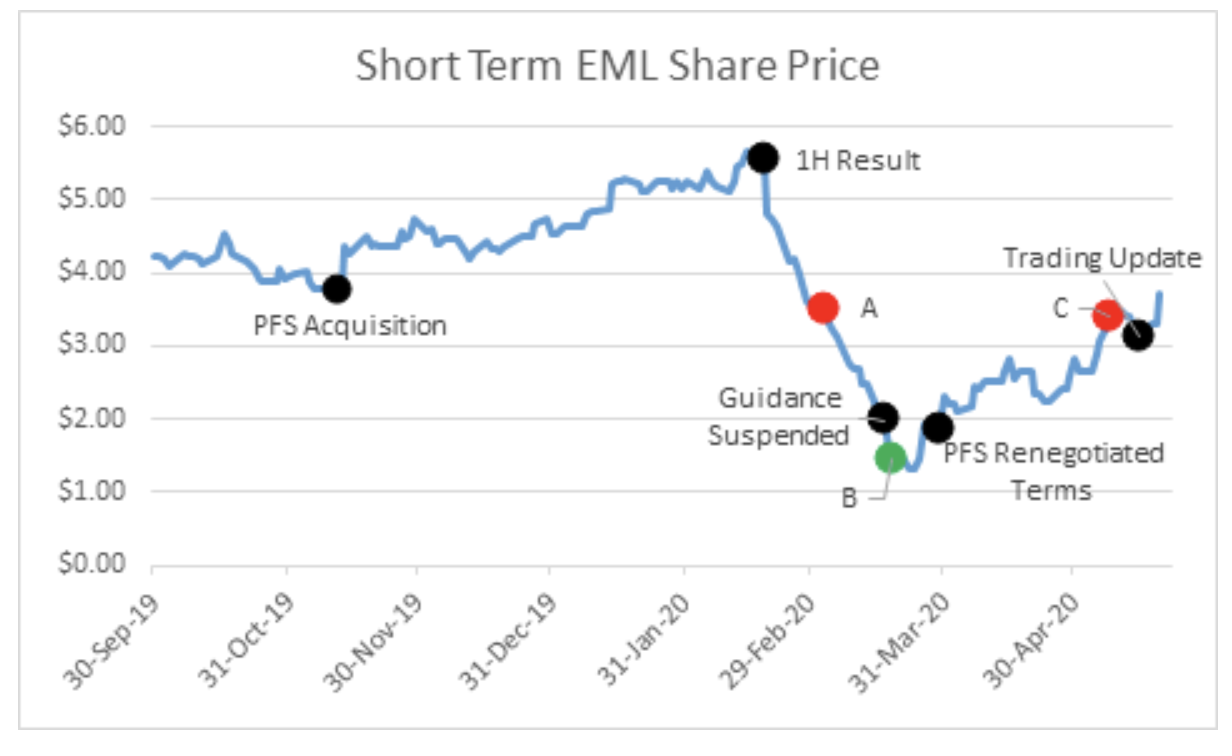

Taking a closer look at the last 6 months, there has been a lot going on. PFS’s acquisition was announced on 11 November 2019, and at the time was well received (although, during the COVID-19-related sell-off, concerns over the debt that would have be taken on would intensify).

PFS itself is a high growth business, growing its volumes by 46% over the last 4 years. Its major business lines are in the high growth areas of Digital Banking and Government disbursements.

The 1H20 result was poorly received, however, as the market was anticipating an upgrade to guidance, which was not fully met. That said, the underlying trends in the result were good, with strong organic growth evident across the business.

As COVID-19 began to play out in late February and into March, the EML share price dropped significantly, just as the share prices of many high PE growth stocks did during this period. Uncertainty during this period was extremely high, and the overall market fell heavily due to concerns over the virus itself and the impact of lockdowns.

EML also had company-specific issues:

1) lockdowns meant that shopping centres around the world closed, impacting EML’s largest business segment, gift cards; and

2) the PFS acquisition was still going through the regulatory approval process, and one of the outcomes of the acquisition was that EML would take on debt, which was a concern, given that earnings from gift cards were dropping off.

We sold some of our position (point A in the chart) due to our concerns about the impact of COVID-19.

On 19 March, EML provided a business update, which showed that up until that date the business trends remained favorable. However, lockdown measures were coming into place, and this would see shopping mall closures, which would directly impact EML’s gift card business. Given the uncertainty, EML withdrew guidance and moved to quarterly-style updates of actual results.

We increased our exposure to EML at point B in the chart, as in our view the share price had fallen to a level where no matter the outcome of COVID-19, it was an absolute bargain.

On 31 March, EML announced the renegotiation of the terms of the PFS transaction. The key point that arose was that the upfront acquisition price was reduced from A$423m to A$252m. Obviously, this was a favorable outcome for EML’s shareholders, but the more important point was that EML would no longer need to take on any debt and, following the capital raising undertaken in November when the PFS acquisition was first announced, would have in excess of $100m cash on its balance sheet. This really began the strong rally in the share price.

Impacts of COVID-19

When COVID-19 first emerged, there was significant uncertainty about the virus itself and the economic implications. In this type of environment, “risk-off” occurs and the market’s time horizon narrows significantly. As a result, long-duration stocks like EML suffer disproportionate falls. Then stocks directly affected by the crisis fall even further, and in the case of EML this occurred due to its exposure to gift cards. As the magnitude of the crisis intensifies, the market begins to focus on liquidity: specifically, does the company have enough cash to ride out the situation? Whenever liquidity is a concern, all other investment considerations are irrelevant and the share price collapses. When the liquidity issue is resolved, the existential threat to the business is removed, and the share price rallies off extremely oversold levels.

Therefore, EML’s statement that it had over $100m in liquidity meant that it could ride out COVID-19. It does not matter how bad earnings are right now, or how bad GDP or unemployment will be in the current quarter. If the liquidity position of a company is resolved then an oversold share price will recover. This is exactly what occurred with EML.

We took some profits in EML at point C in the chart, in order to manage the size of the EML position in our portfolio.

Finally, a couple of days ago, EML provided a trading update. This update showed that the gift card business did suffer significantly in April, as shopping centres around the world were closed, however with economies beginning to reopen around the world the outlook is improving. Importantly, it should be remembered that gift cards are a seasonal business, and that currently we are in the seasonal lows. Notwithstanding the COVID-19 hit to the earnings of the gift card business, EML is still profitable and generating strong free cashflow, and is still onboarding new clients and launching new programs. In fact, management stated that its sales “pipeline is better than it has ever been”

The outlook for EML in a post-COVID-19 world is strong

The need for the digitisation of payment processes has been highlighted during the crisis, and this plays directly into EML’s hands. One of the big drivers of EML’s growth over time has been the desire for its corporates to move away from paper-based systems and towards more efficient card-based systems.

Now there is a desire to move towards fully mobile-based systems where the gift card is loaded directly into an Apple Wallet or Samsung Pay or similar. The fully mobile payment solution that EML offers is now a must-have rather than a nice to have, and explains EML’s strong pipeline.

Benefit at every stage of a cycle

Monash Investors Limited invest in a small number of compelling stocks that offer considerable upside and short expensive stocks that are at risk of falling. Want to learn more? Hit the 'contact' button to get in touch or visit the website for further information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Combining over 25 years’ experience to offer compelling early stage insights on pre-ipo and microcap companies mispriced and misunderstood by the market. We maintain a long/short absolute return focus, with strict stock selection criteria.

1 stock mentioned

1 contributor mentioned

Combining over 25 years’ experience to offer compelling early stage insights on pre-ipo and microcap companies mispriced and misunderstood by the market. We maintain a long/short absolute return focus, with strict stock selection criteria.

Combining over 25 years’ experience to offer compelling early stage insights on pre-ipo and microcap companies mispriced and misunderstood by the market. We maintain a long/short absolute return focus, with strict stock selection criteria.

Comments

Comments

Sign In or Join Free to comment