Sunset Strip > Trading Day Wrap From Blue Ocean 20170531

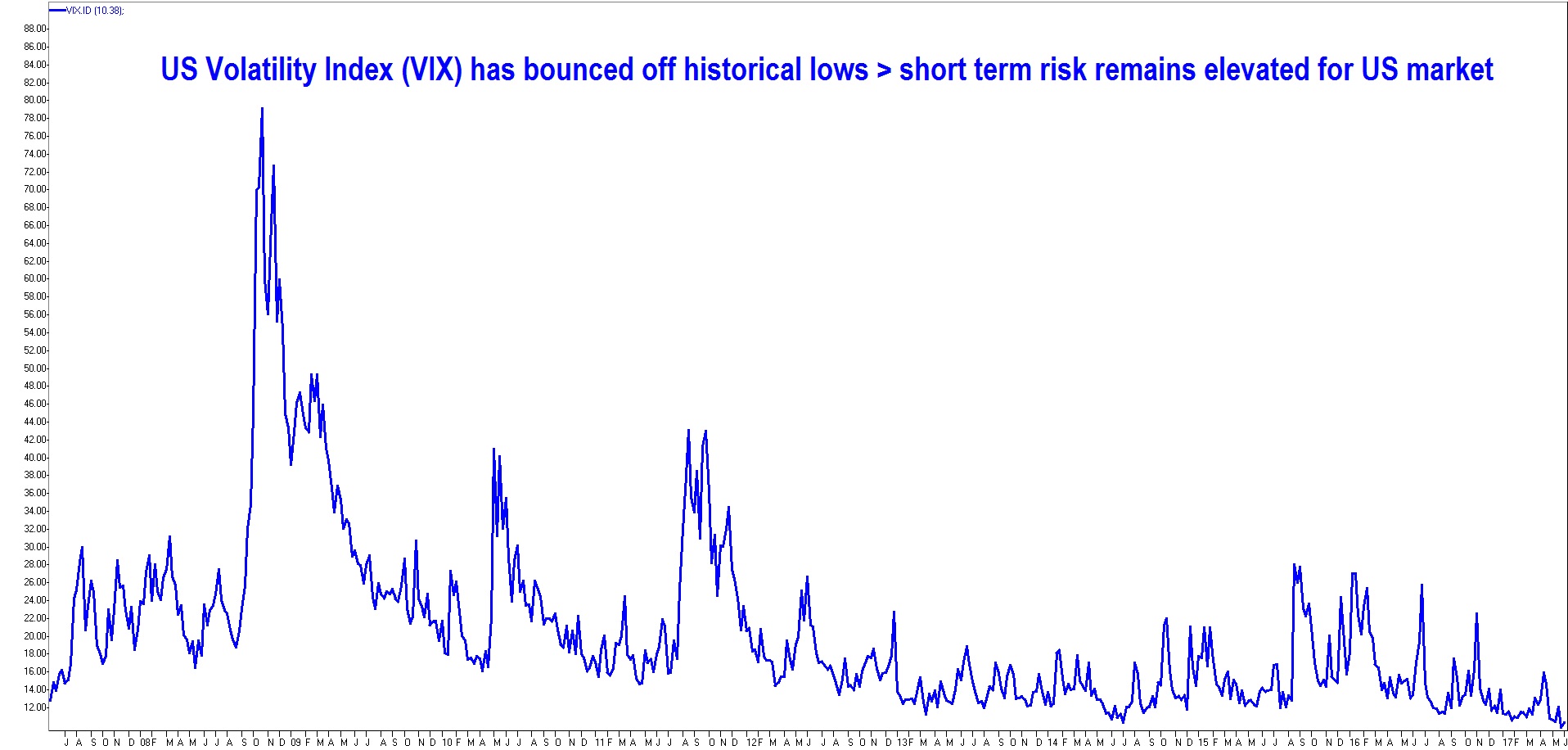

Local market ran up on China data before fading to a slight positive day for the end of month. Tax loss selling in May/June will add to the seasonal weakness while geopolitical risks and US fiscal delays are overshadowing global growth story. We had strong manufacturing and non-manufacturing PMI data from China while Japanese Industrial Production was another solid data. Wages remain weak globally…Singapore was another casualty of historical weak wages growth. Big turnover day with QUB raising needed funding, MSCI changes and month end funk added to the usual tax loss selling traffic around this time of the year. Markets are completely ignoring the UK election risks…like Aussie elections recently, UK went to an early quick election to take advantage of a weaker opposition but now it looks like it will be closer than expected…no election is a dead rubber anymore!!! Market Outlook likely to remain volatile in the short term with macro risks while medium to long term view remains positive. Big macro week…(1) WEDNESDAY > CANADA GDP (2) THURSDAY > AUS Private Capex, AUS Retail Sales, CHINA Caxin Manufacturing, EU Markit Manufacturing, US ISM/Markit Manufacturing, US ADP Employment (3) FRIDAY > AUS New Home Sales, US Non-Farm Payrolls, US Trade Balance. The best performers were Property, Staples and Retail while Energy, Health Care and Miners were the worst performers..

Click here for the full report...

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and CEO at Deep Data Analytics (www.deepdataanalytics.com.au) which is an integrated data analytics driven investment strategy service provider.

6 topics

8 stocks mentioned

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Comments

Comments

Sign In or Join Free to comment