Sunset Strip > Trading Day Wrap From Blue Ocean 20170802

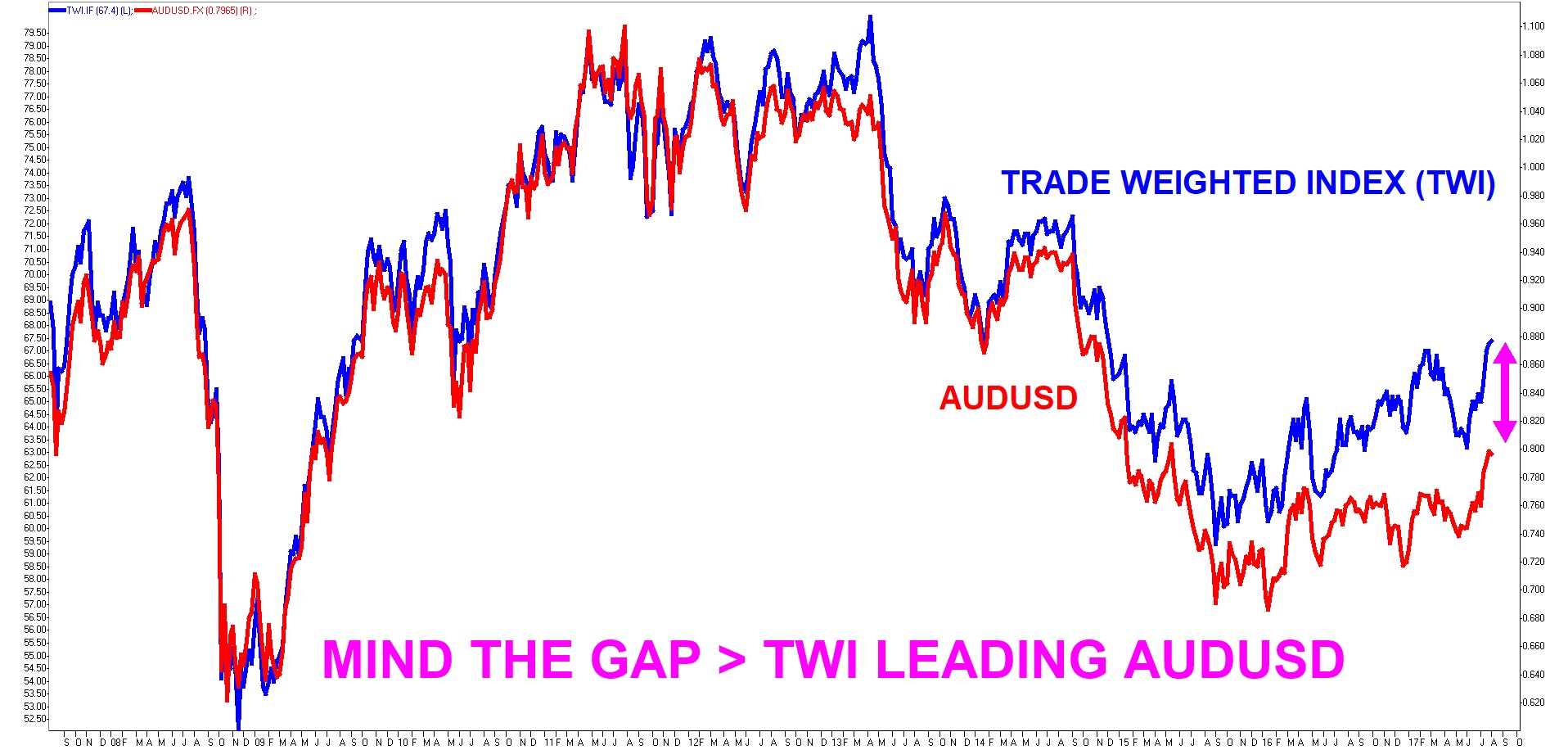

Local market was smacked down on weaker commodities and then flip-flopped at the bottom despite solid bounce in building approval. US ADP employment data will be key tonight for sentiment while US Fed jawboning will be on full flight. RIO result out after market shows slight miss with upgraded buy back and debt reduction and waning cost out. Apple result after US market close was positive and should help the global sentiment. The best performing sectors were Industrials, Retail and Health Care while the worst performers were Miners, Property Trust and Telecom Services. Consensus bet is for AUDUSD to go down but we think the risk is that AUDUSD heads up to 87-94 trading range. We remain negative short term on the industrial global businesses…Health Care and other large cap global industrials are on the firing line. Rising commodities and weak USD outlook in the short term supports higher AUDUSD. On the sector/stock front….(1) LYC on a rip higher as they pay off debt and market interest in rare earth is back (2) AJA jumps on the cross currency moves (3) DRM is the turnaround gold play (4) CYB third quarter update showed the cost cutting cycle is delivering (5) GMA result shows the risk in the property market and the banks (6) RMD result was weaker than expected and took a hit from lofty valuations (7) NVT taking more hits after the result update.

Click here for the full report.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and CEO at Deep Data Analytics (www.deepdataanalytics.com.au) which is an integrated data analytics driven investment strategy service provider.

5 topics

9 stocks mentioned

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Over 30 years’ experience in the finance/tech industry. Mathan has worked extensively in all parts of the finance sector (i.e. County NatWest, Citi, LIM, Southern Cross, Bell Potter, Baillieu Holst and Blue Ocean Equities). Currently Founder and...

Expertise

Comments

Comments

Sign In or Join Free to comment