The bear case on ecommerce stocks

2020 was a once-in-a-generation opportunity for pure-play ecommerce businesses, and there was a lot of money to be made by investors. However, as we move into 2021, is the ecommerce sector still an attractive investment on a risk/reward basis? While the bull-case for the sector is well understood by most, below we put forward the bear-case so investors can make up their minds.

In this Wire we discuss, Valuation, Active Customer (AC) growth, gross margins and Customer Acquisition Cost (CAC). The bear-case would see all these metrics deteriorate over the next 6-months.

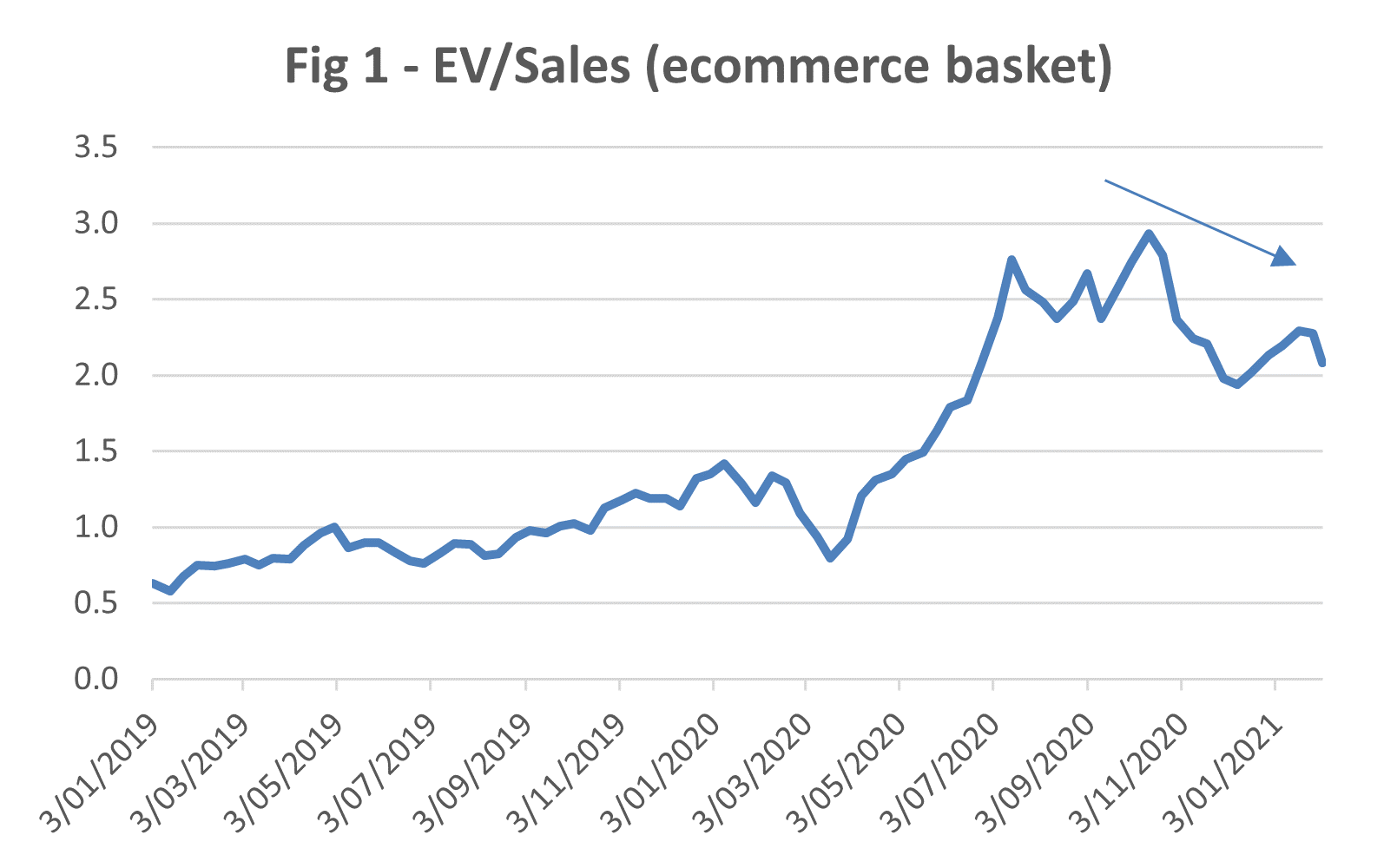

Valuations are high

The valuations of ecommerce businesses have taken a material step-up over the last 12-months as we all know. However, not only have share prices increased to factor in the higher revenues printed during lock-down periods (which are arguably unsustainable), they are also factoring in a continuation of above-trend revenue growth in coming years, as evidenced by the sales multiple in Figure 1 below. A new investor at today’s share price has to believe that this extraordinary growth is going to continue at a level well above that in the past.

The high number of IPOs and capital raisings in recent months potentially give an indication of what vendors of these assets think about current market valuations.

Active Customer (AC) growth may have peaked

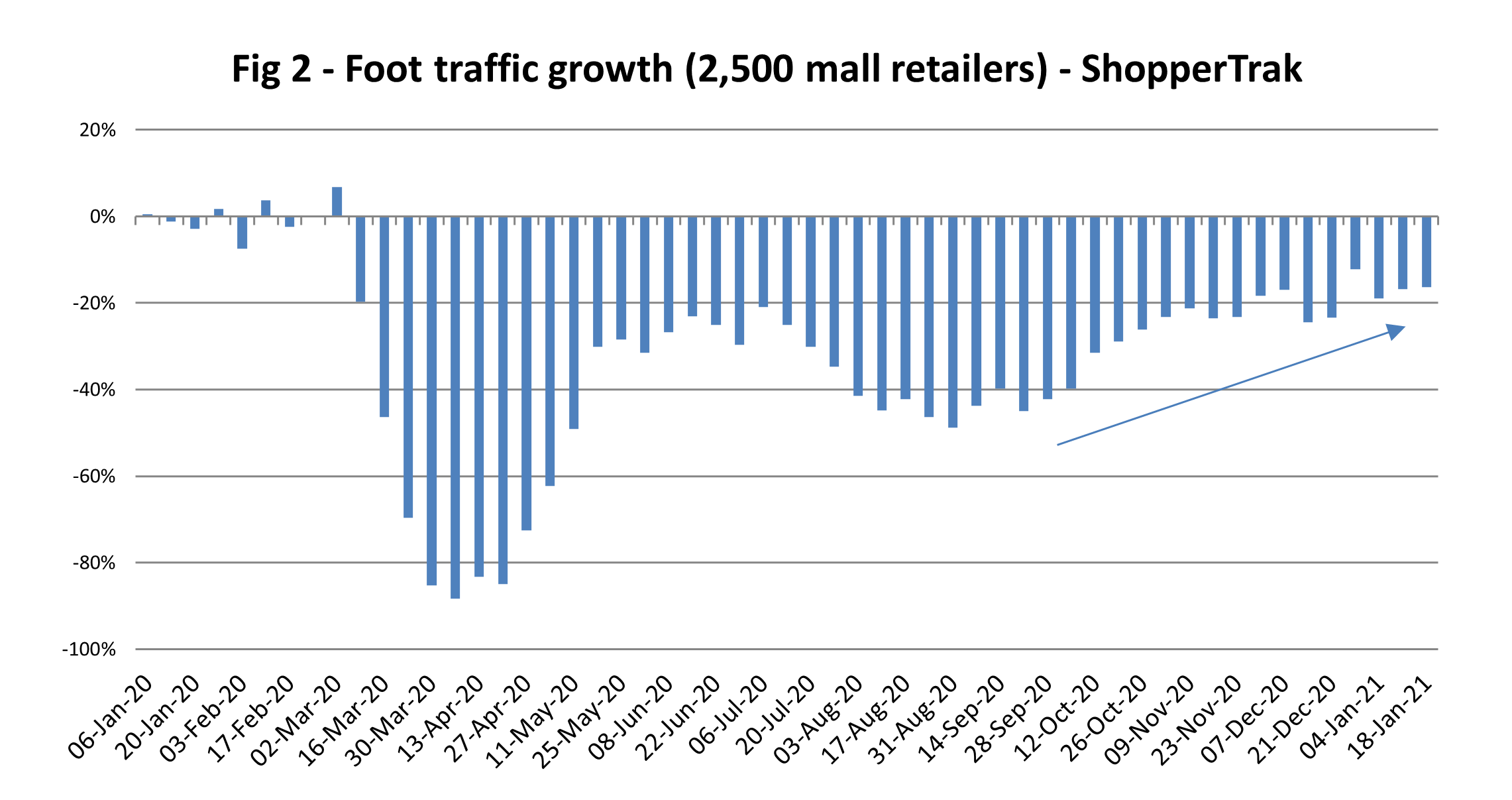

The pandemic has created an extraordinary opportunity for ecommerce companies to transact with many more customers than in the past. While many have done well to add aggressively to their customer counts, the question now is whether they can keep all of them? As seen in Figure 2 below, footfall in major shopping centers was materially down for many months of the last year as physical retail stores were closed. The data also shows that consumers are now returning to stores. As a target, industry members we have spoken to suggest footfall may settle 10% below pre-Covid levels. So, while shopping centre foot traffic has been a tailwind for ecommerce since march 2020, it is soon to become a headwind. In addition, there has been much discussion about a ‘structural shift’ in ecommerce penetration, which is no doubt a fact. However, how much of this is ‘structural shift’, and how much has been accentuated by fiscal stimulus tailwinds that have benefited all retailers?

Finally, on the assessment of active customers, for some ecommerce retailers their consumer ratings (see Trust Pilot) are actually quite poor, suggesting some consumers have been shopping with them out of need rather than desire.

Looking forward, if a company’s ‘active customer’ growth starts to tail-off (or decline in some cases), what revenue multiple would an investor expect to pay for that stock?

CAC (Customer Acquisition Costs) are rising

The pandemic has exposed many bricks-&-mortar retailers that had not invested sufficiently in the digital channel. This has resulted in a rush of activity by well-funded traditional retailers to up-skill in that space. This has therefore lifted the level of competition for all pure-play retailers, in part resulting in higher costs to acquire new customer. For example, Catch, a pure-play ecommerce business wholly owned by Wesfarmers ($62bn market cap), has stated publicly that it intends to run the business at break-even for the foreseeable future in an attempt to grow its market share. This effectively drives up the CAC for any pure-play ecommerce competitors that compete in those categories.

Gross Margins may have peaked

Gross margins in the ecommerce sector have been rising significantly in 2020, aided by unexpected demand, a lack of competition and shortages of inventory. Competitive dynamics are likely to dictate that this is not sustainable as inventory availability and brick-&-mortar supply normalises.

In the meantime however, it is not all that bearish. Ecommerce retailers are still printing money and using that to fortify their businesses through brand building and acquisitive growth. There is no doubt that these are much stronger businesses than they were 12-months ago. It will be fascinating to see what the market thinks of this sector in 6-months’ time.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Daniel has over 20 years of financial markets experience, and is Portfolio Manager of the Blackwattle Small Cap Quality Fund and Blackwattle Small Cap Long-Short Quality Fund.

.jpg)

5 topics

4 stocks mentioned

.jpg)

Daniel has over 20 years of financial markets experience, and is Portfolio Manager of the Blackwattle Small Cap Quality Fund and Blackwattle Small Cap Long-Short Quality Fund.

Daniel has over 20 years of financial markets experience, and is Portfolio Manager of the Blackwattle Small Cap Quality Fund and Blackwattle Small Cap Long-Short Quality Fund.

Comments

Comments

Sign In or Join Free to comment