What's the biggest risk to the banks?

Interim reports for the major banks have concluded and the wires are awash with Budget commentary. Sentiment towards the Budget seems largely positive, however, it appears a new risk has emerged for Aussie banks and investors responded accordingly.

I've reached out to a few Livewire contributors to get their assessment of the biggest risk to the banks. It seems overwhelmingly, in the short-term at least, that the banks will come under fresh selling pressure.

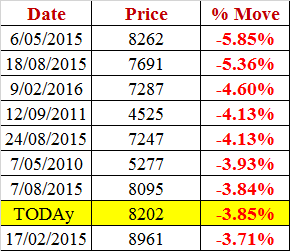

The day CBA stuffed the market - 9th of May, 2017

Data and comments courtesy of Richard 'Coppo' Coppleson from Bell Potter

- It was a big day for volume on the ASX. CBA alone CBA saw volume of 6.4m shares or 88% above their normal volume

- CBA had it's 8th biggest one day fall in 7 years (since 2010) & worst 1 day fall in 15 months

- The fall was so bad that CBA alone took -21.5 points OFF the ASX 200- or in other words today was the day CBA stuffed the market

- They accounted for an incredible 69% of the fall - all by themselves

- It was like the market said... 'You don't deserve to be the most expensive bank in the world any more - you don't deserve to trade at a big premium to the other banks'

"Today it will be interesting to see how many brokers turn on CBA & recommend selling it & switching into the best of the banks - NAB??!! "

The housing cycle is the greatest potential threat

Romano Sala Tenna, Katana Asset Management

The banking sector is facing a range of well documented risks, including the uncertainty surrounding the cost of financing. The ability of the major banks to pass on out of cycle rate rises is crucial to maintaining and/or expanding their interest margin.

Regulatory risk is also ever-present. In the coming 12 months we are likely to see further moves in the areas of capital requirements as well as stricter lending criteria.

However, despite the potential impact of both of these risks, the greatest potential threat to the banks is the housing cycle itself. If the housing cycle has peaked as some early data is indicating, then this materially impacts both bank revenues and costs.

- Revenue is compressed by slower credit growth and thinner margins as banks compete for customers.

- Costs are impacted by rising bad and doubtful debts (BDD) and provisioning for future debts.

Investors have become too gloomy on the banks

Sam Ferraro, Evidente

There is plenty of bad news buffeting the sector and the introduction of a levy on banks’ liabilities will only see sentiment worsen in the near term, with analysts expected to downgrade their earnings forecasts.

"I remain positive on the sector because pricing suggests that investors have become too gloomy on the sector’s prospects"

The sector is trading on a book multiple of 1.9x which represents a 50% discount to the non-bank industrials. In the past two decades, dispersion of this size has only occurred two other times; during the financial crisis and in the early 2000s.

Despite the fact that higher capital requirements have crimped the banks’ ROEs, the sector’s profitability remains higher than non-bank industrials.

Key take outs

- Expect brokers to adjust their earnings forecasts lower, likely to be accompanied by further selling

- The housing cycle remains a key concern with bank profits at risk of being squeezed at the revenue and cost lines

- There is plenty of negative sentiment towards the sector right now, on current book multiple this 'bearish' sentiment doesn't appear to be justified

- The 2017 Budget has delivered a massive 'hospital pass' from Malcolm Turnbull to the Banks with the introduction of a new bank levy...

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions.

Safe investing and thanks for reading Livewire.

4 stocks mentioned

1 contributor mentioned

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions. Safe investing and thanks for reading Livewire.

Expertise

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions. Safe investing and thanks for reading Livewire.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management