The one place where retail sales growth is booming

Patrick O'Reilly

APN Property Group

Retail sales growth is something commercial property investors fervently hope for. When shoppers are buoyant, tenants are doing well, landlords like to raise their rents, leading over the long term to juicier dividends for investors.

In many countries experiencing low wages growth, there are fears this dynamic could operate in the other direction. Globally, retailing landlords have been on the nose as a result. Low retail sales and corresponding wages growth, plus increasing competition from online players, means rental pressure in some markets is trending down rather than up.

Modest retail sales growth does raise an interesting question; where can commercial property investors get exposure to rapidly rising retail spending that should lead to higher dividends down the track? Hong Kong could be at the top of your list, especially if you’re an income investor aware of the dangers of home bias but haven’t yet done anything about it.

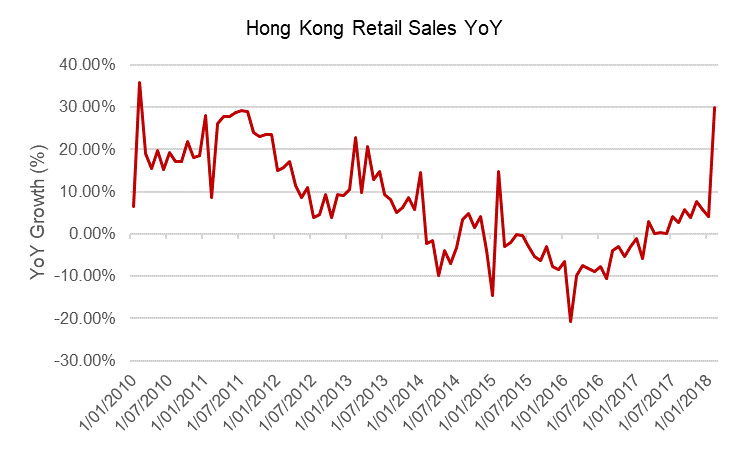

Hong Kong’s retail scene has undergone a stunning transformation. Two years ago, year-on-year retail sales growth was non-existent. In February this year it hit 29.80%. As the following chart shows this is a level not seen since 2010*.

Source: Bloomberg March 2018

There is a mundane explanation for at least some of this growth. The Lunar New Year fell in February this year (last year it was in January) and Hong Kongers are notorious shoppers over the Chinese New Year break. We don’t expect to see similar double-digit numbers in the coming months. Hong Kong retail sales have been steadily rising over the past year (refer to above chart).

Three economic trends explain why.

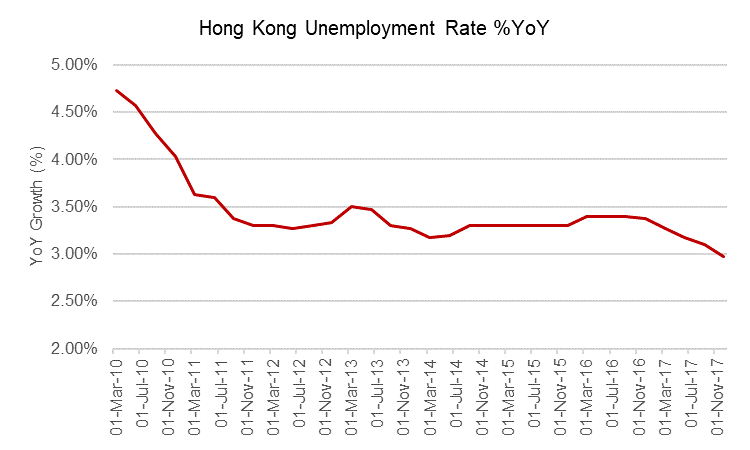

First, Hong Kong’s unemployment has been steadily falling, reaching a 20-year low of 2.97% at the end of 2017. A strengthening economy has led to a tightening labour market, particularly in retail, finance and business services. There’s also a big push from Chinese financial services firms to expand their presence in Hong Kong, which is why the largest gains in employment last year were concentrated in finance, IT and real estate.

Source: Bloomberg March 2018

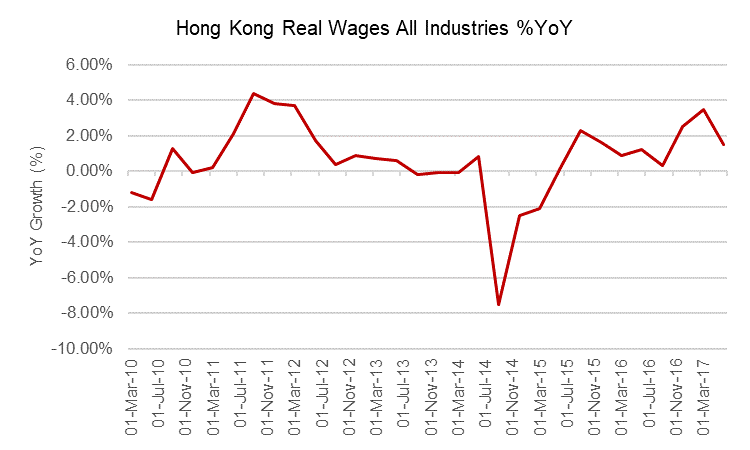

This has led, unsurprisingly, to the second factor – wages growth, which has been on an upward trajectory since July 2014. As Hong Kongers earn more, more of their spending is going on luxury items. Sales of electrical goods, for example, increased 12.1% in 2017, assisted by the release of the iPhone X. Spending on jewellery, watches and other luxury goods, meanwhile, increased 6.30%.

The trend is clear. With lower unemployment leading to tighter labour markets and higher wages, Hong Kongers are getting out into their numerous shopping centres and opening their wallets and purses.

Source: Bloomberg March 2018

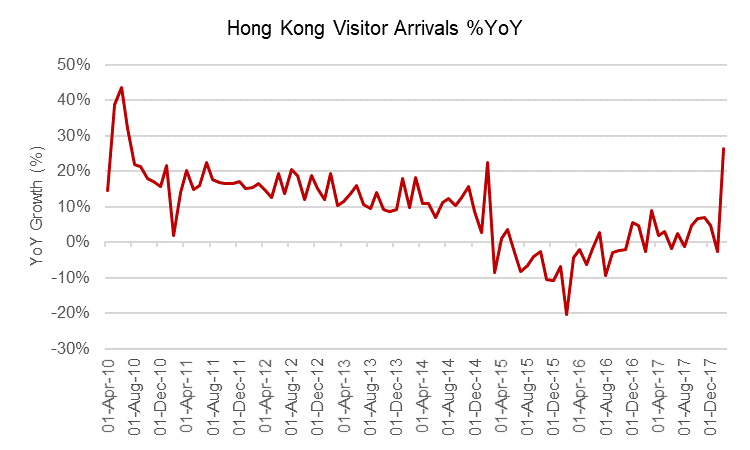

The third, and most important, factor has nothing to do with the locals and everything to do with visitors. Hong Kong has always been the destination of choice for Chinese vacationers, who tend not to shop in half measures.

Wealthy Chinese often conducted their luxury shopping in Hong Kong to avoid paying taxes back home. A Government-led crackdown, however, led to fewer tourists splashing the cash. Visitor arrivals were down 20% year-on-year in February 2016. We explained the retail slump here, saying that:

“High-spending Chinese visitors are finding Hong Kong a far less attractive destination. Mainland tourist numbers are down by about a third on the prior year. New visa restrictions and negative sentiment caused by a series of high-profile anti-mainlander protests in Hong Kong are contributing to the drop, as well as growing competition from destinations like Japan, South Korea and Europe, which, with weakening currencies, are becoming more affordable.”

In response, Hong Kong’s Tourism Board launched advertising campaigns aimed at showcasing the city’s various culinary, kid-friendly and outdoor attractions to Chinese travellers.

The strategy appears to be working. After two straight years of decline, the number of mainland Chinese visitors increased by 7.2% last year. The impact of increasing tourism was particularly pronounced last February with arrivals surging 26.3% over the Lunar New Year, fitting in neatly with the increase in retail sales over the same period.

The bump can also be attributed to the Guangzhou-Shenzhen-Hong Kong Express Rail Link, a new high-speed railway that will connect mainland China to Hong Kong. With some stages already open, the final link to downtown Kowloon is expected to open at the end of this year. The new infrastructure will make it easier for huge numbers of Chinese shoppers to access Hong Kong’s retail precincts.

Source: Bloomberg March 2018

The big question though, is whether lower unemployment, more visitors and increased spending on luxury items is making its way to landlords and their investors via higher rents. Preliminary results from Hong Kong landlords suggests that, if it isn’t already, it soon will be.

Fortune REIT, the owner of a portfolio of shopping centres throughout Hong Kong, reported that tenants whose leases ended in 2017 were re-signing their leases, on average, at a rent 12.8% higher than what they were paying previously.

The average rent across Fortune REITs portfolio increased from $41.8 HKD per square foot (psf) to $43.2 HKD psf over the year as a result. Given that 40% of Fortune REIT leases are expiring in 2018, we’d expect a further jump in their average rent as tenants re-sign at higher rates.

More evidence comes from Swire Properties, the owner of Pacific Place in Central Hong Kong. Although not a holding in our portfolio, we did note that it reported tenant retail sales increasing 7.2% in 2017, an impressive turnaround on 2016 when the corresponding figure was down 12.8%. Retailers with expiring leases were re-signing at rental rates 15% higher, on average, than previously. Hong Kong retail tenants seem content to pay up for a building and location delivering strong retail sales growth.

A few more quarters like this and the major Hong Kong property trusts will surely be enjoying the benefits of higher rents. In anticipation, we’ve been recently increasing our exposure to the Hong Kong-based retail property trusts in our portfolio.

All of which is to say that investors looking to diversify their commercial property income stream away from Australia and towards a region of higher economic growth and burgeoning retail spending might want to take a look at Asia. We’ve been going shopping in Hong Kong lately; maybe income investors that want a truly diversified income stream from a high-growth region should, too?

Interested in real estate?

Check out our blog to access analysis and insights from the experienced team at APN Property Group

*Past performance is not an indicator of future performance.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Before APN, Patrick worked for Pitcher Partners Investment Services as an associate Research Analyst. Patrick undertook research on the AREIT, Transportation & Infrastructure sectors to give investment recommendations to a team of financial advisors.

Patrick O'Reilly

Analyst, Asian Real Estate Securities

APN Property Group

Before APN, Patrick worked for Pitcher Partners Investment Services as an associate Research Analyst. Patrick undertook research on the AREIT, Transportation & Infrastructure sectors to give investment recommendations to a team of financial advisors.

Expertise

Patrick O'Reilly

Analyst, Asian Real Estate Securities

APN Property Group

Before APN, Patrick worked for Pitcher Partners Investment Services as an associate Research Analyst. Patrick undertook research on the AREIT, Transportation & Infrastructure sectors to give investment recommendations to a team of financial advisors.

Expertise

Comments

Comments

Sign In or Join Free to comment