The sweet spot of credit

Even before the COVID-19 pandemic rocked global financial markets, Australia was on its way to join the lower yield world. Now, Australian investors in search of stable, current income strategies are facing a challenge as strategies of the past are unlikely to generate the returns and levels of income they once provided.

This can be observed across the risk spectrum with the Reserve Bank of Australia’s (the “RBA”) cash rate at 0.25% and Australian government bond yields below 1%, all the way up the risk spectrum to Australian banks’ equity and their now more uncertain dividends.

We believe solutions to generate higher income and diversification for Australian investors’ portfolios exist within certain parts of the global fixed income markets that provide current income and attractive relative yields with downside protection; we call it the “sweet spot” of credit.

To be successful in what we call the “sweet spot,” we believe an arduous focus on capital preservation and the flexibility to select the most attractive relative value are key. We believe this can be achieved via our ability to identify attractive relative value in the more senior, higher quality segments of the bond, loan and structured credit markets and shift allocations among these asset classes as appropriate. In addition to maintaining a well-diversified portfolio of senior debt, a 50% allocation to investment grade credit further strengthens the high-quality nature of the strategy.

The Challenge – Australia Joins the Low Yield World

Until recently, Australian investors didn’t have to look too far for attractive yields and income, but the last 24 months have accelerated Australia’s participation in the low cash rate and bond yield world.

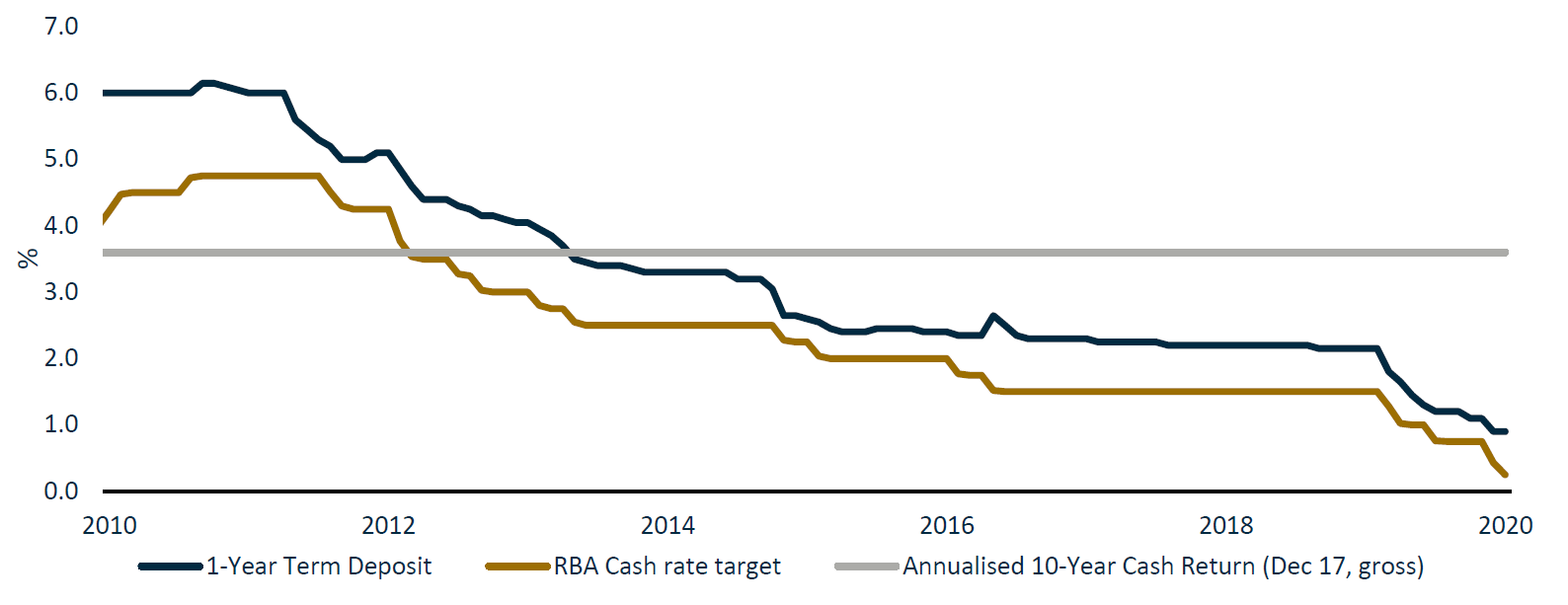

According to a report published by the ASX in 2018, in the last 20 years through December 2017, Australian cash annualised gross return was 4.6% p.a. Interestingly, cash returned 3.6% p.a. in the last 10 years through December 2017, which suggests a downward trajectory of the RBA target cash rate and term deposit rates (Chart 1).

With the target RBA cash rate currently sitting at 0.25%, we believe that achieving the returns of the past in cash products seems unlikely for Australian investors.

Chart 1 - RBA Target Rate and 1-Year Term Deposit Rate

Source: Reserve Bank of Australia (RBA), as of May 2020.

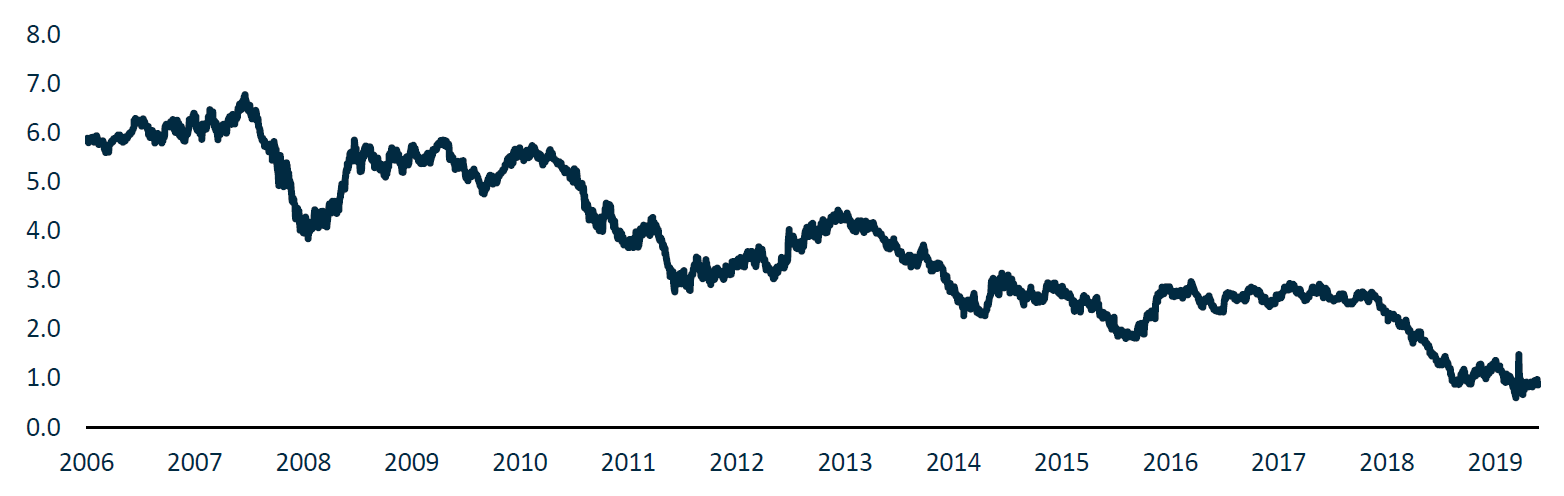

Moving up the risk spectrum (with risk defined as asset price volatility) in the last 10 years, Australian government and corporate bonds have offered attractive yields, generating higher income and returns than cash, with the same ASX report showing returns of c. 6% p.a. for the 10 years to December 2017.

These attractive returns and levels of income have partly been due to a falling yield environment which generates capital gains in fixed rate bonds. When realised, these gains are distributed as income alongside interest payments.

As illustrated in Chart 2 below, over the last 10 years to March 2020, Australian 10-year government bond yields went from over 5% to below 1%, and in the last 12 months, from over 1.5% in March 2019 to below 1%. This latest drop has driven strong returns and provided the expected counterbalance to riskier assets such as equity in such periods of volatility.

However, looking ahead, with 98% of Australia government bonds currently trading at or above 100% of face value and little room for yields to move further down (although they could go negative!), we believe income generation and outsized returns are unlikely to be what investors have experienced in recent periods.

Chart 2 - Australia 10-Year Bond Yield

Source: Bloomberg, as of 22 May 2020.

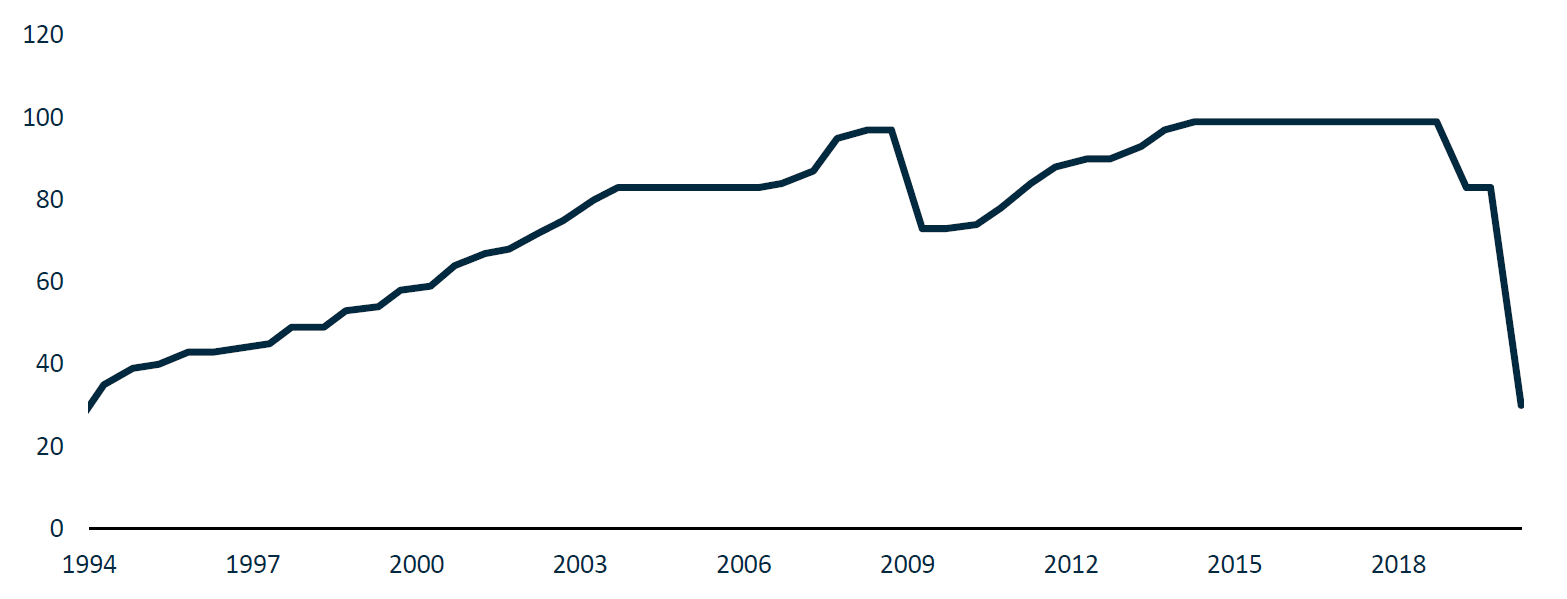

Finally, moving all the way up the risk spectrum to equities, Australian investors have enjoyed many years of high and dependable dividend payments from the major Australian banks. For those happy to endure some price volatility going up the risk spectrum, the four major Australian banks have been a reliable source of higher income.

However, in the wake of the COVID-19 crisis and the ensuing economic turmoil, an unprecedented level of uncertainty leaves many questioning the likelihood and reliability of those dividends as the banks employ a more conservative approach to cash management. As an example, NAB decided to cut their next dividend payment by 64%. NAB has not seen such low dividends since 1994; even during the Global Financial Crisis (the “GFC”), dividends did not decrease as precipitously as they have recently (Chart 3). This decision and the uncertainty around what other banks will do, has highlighted to investors that unlike fixed income and credit instruments, shares have no contractual obligation to a fixed level of distribution.

Chart 3 - National Australia Bank (NAB) Dividend Rate per Share (AUD)

Source: National Australia Bank (NAB), as of May 2020.

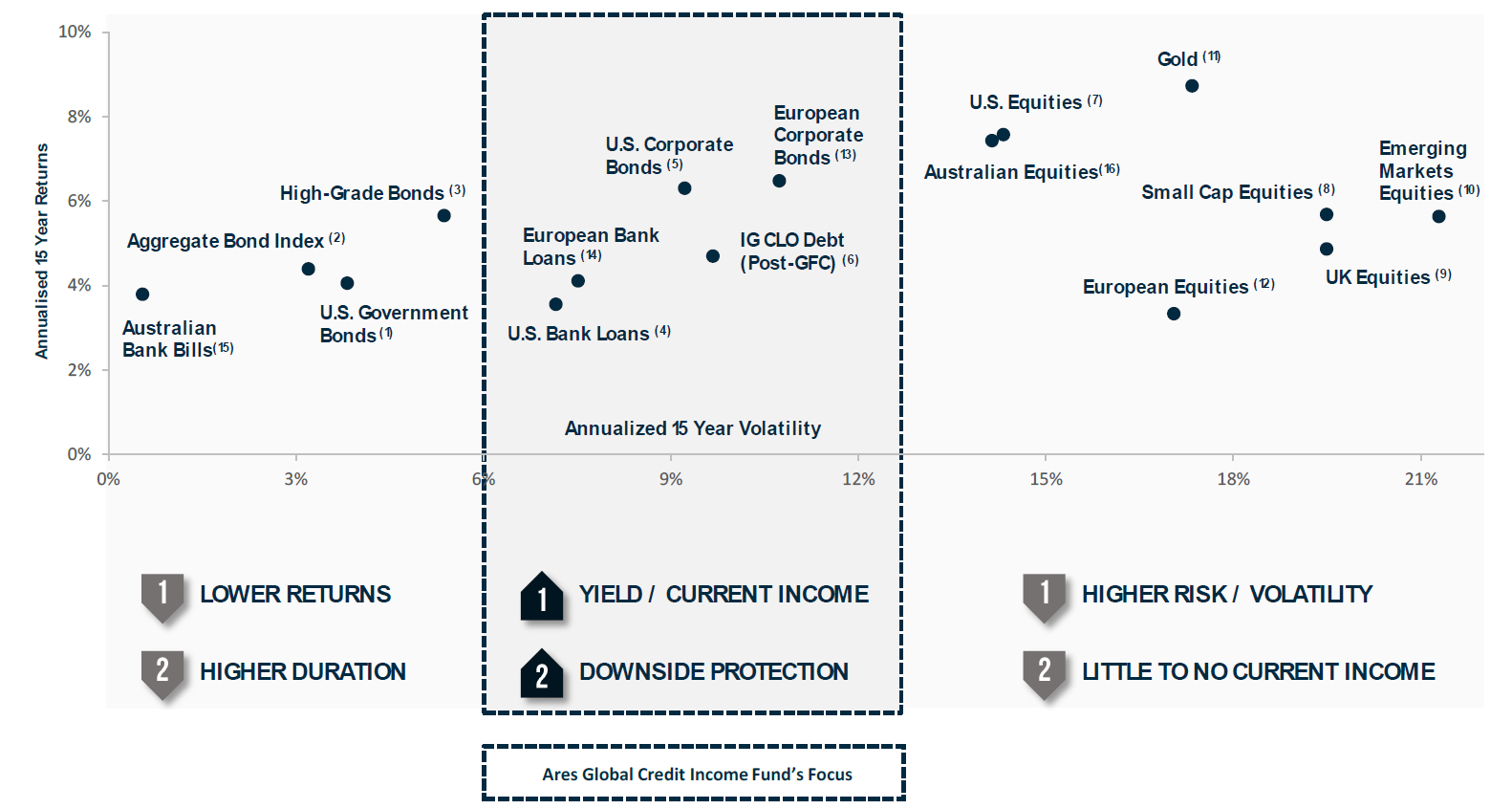

The “Sweet Spot” of Credit

The challenge posed by low yields is not new for many global investors. Since 2007, the Ares Credit Group has been able to diversify portfolios with asset classes that we believe offer attractive yields and current income within global fixed income markets. We call it the “sweet spot” of credit.

We believe high quality corporate and structured credit presents the most compelling risk-reward opportunity.

Our strategy seeks to avoid riskier asset classes (equities) as well as minimizes exposure to the more stressed, lower quality segments of the credit market (CCC-rated bonds and loans), which reduces volatility and default risk, and further takes advantage of the downside protection offered by senior and often secured credit position in the capital structure of corporate bonds and loans and asset backed securities. In tandem, Ares believes this particular focus offers greater opportunities for current income in yield than traditional fixed income and passive strategies.

Chart 4 - The “Sweet Spot” of Credit

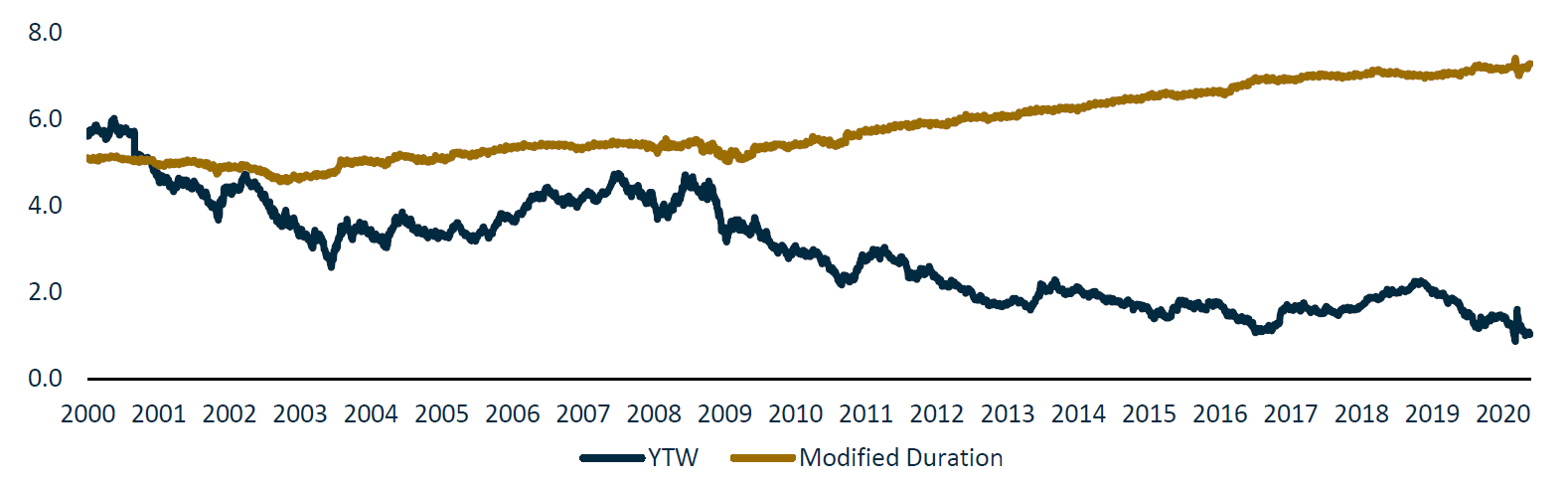

Within global fixed income specifically, falling yields accelerated by the recent sell-off in risky assets resulted in past performance favouring higher interest rate duration assets (Chart 5). For example, U.S. government bonds and high-grade corporate bonds that have higher interest rate duration risk than bank loans or investment grade CLO debt have outperformed (higher return and lower volatility). But, with government bond yields at or close to historical lows, the potential return and current income generation from the lower end of the risk spectrum seems challenged.

Chart 5 - Bloomberg Barclays Global-Aggregate Index (Unhedged US$) Yield Versus Duration

Source: Bloomberg, of April 30, 2020. Please refer to pages 9-11 for Index Definitions and an important index disclosure.

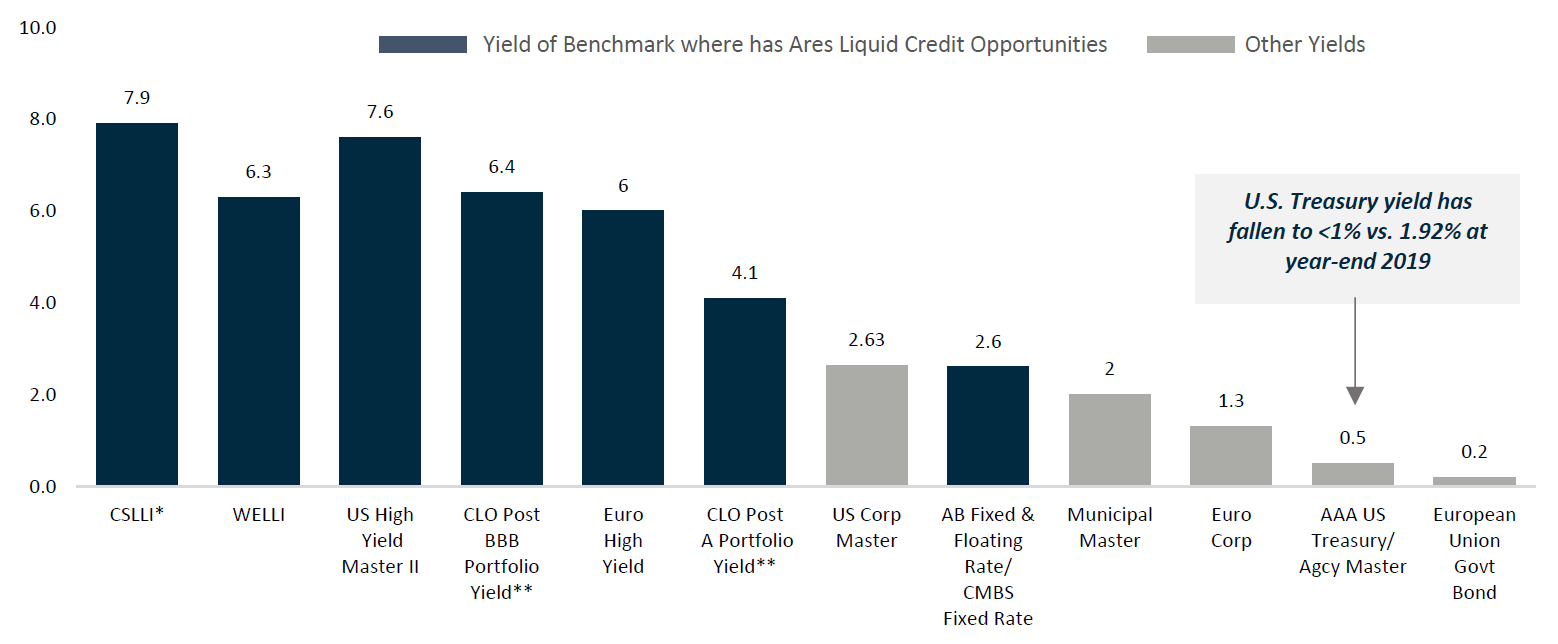

Our focus is therefore on the asset classes that currently offer higher relative yields. These higher yields are largely derived from the credit spreads these securities pay on top of government bond yields. These spreads compensate investors for the additional risk that they take by investing in credit. As of the date of this letter, credit spreads in bank loans and corporate bonds are wide by historical standards, partly due to elevated fears around default risk for credit instruments and uncertainty in general which has pressured technicals. We believe this environment presents ample opportunity for managers looking to take advantage of inefficiently priced segments of the fixed income markets. And, while dynamic allocation across asset classes is certainly a distinctive feature of Ares’ strategy, we recognize that falling yields is a global trend across developed and emerging markets and seek to opportunistically allocate across regions.

Chart 6 - Relative Yields Across Asset Classes

Source: ICE BofA Indices, S&P Capital IQ, Credit Suisse Leveraged Loan Index, JPM CLOIE Indices, as of May 20, 2020.

In other words, current income and potential returns are attractive in the sweet spot of credit, but to fully optimise the strategy, we believe managers must be focused on minimising default risk.

Protecting the Downside

While outperformance is certainly a key component of successful investing, as a steward of investor capital, Ares places an equally important emphasis on downside protection and capital preservation. A heightened focus on portfolio positioning, volatility and duration are of particular importance during times of stress and economic uncertainty.

Default risk analysis is fully incorporated into Ares’ investment process, which employs rigorous monitoring of credit performance with the robust use of data analytics to identify potential downgrade candidates. This focus has resulted in Ares experiencing significantly lower defaults in its broadly syndicated bank loan and high yield bond strategies since inception during times of stress. At the height of the GFC fall-out in 2009, U.S. high yield bond and loan markets saw default rates rise close to 11% and 15%, respectively, while Ares’ flagship bank loan fund and U.S. High Yield composite have experienced fewer than 4%. Ares’ European portfolios performed similarly, with its flagship European high yield portfolios experiencing a 3.4% default rate during the GFC versus the market’s 13%. During the same period, Ares’ flagship European loans portfolios experienced 0 defaults.

Independent of the fund’s 50% allocation to investment grade credit, Ares expects to maintain a higher concentration of double B-rated loans and bonds and will opportunistically consider single B-rated debt with strong fundamentals and the potential for upside. In current market conditions, we believe our ability to significantly under-default the market will again prove critical to capitalising on opportunities available in the sweet spot of credit.

The Opportunity Set Has Broadened Amidst Uncertainty, Volatility and Bifurcation in the Credit Markets

Our investment process places a strong emphasis on relative value analyses to identify optimal risk-adjusted investment opportunities. In this uncertain, volatile and bifurcated environment our process has highlighted the following opportunities within the sweet spot of credit.

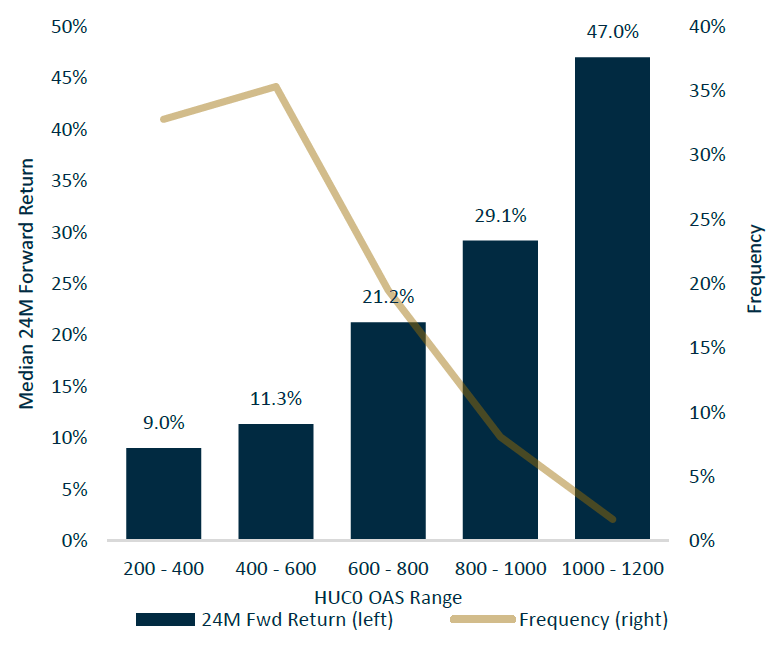

Volatility and uncertainty around corporate defaults have pushed credit spreads (Option Adjusted Spreads or “OAS”) in the high yield bond market (“HY”) to levels not seen since 2009. As it has become increasingly rare to see spreads widen past 800 bps, it is interesting to note that HY OAS have only been wider than 600 – 800 bps c. 20% of the time since 1996.

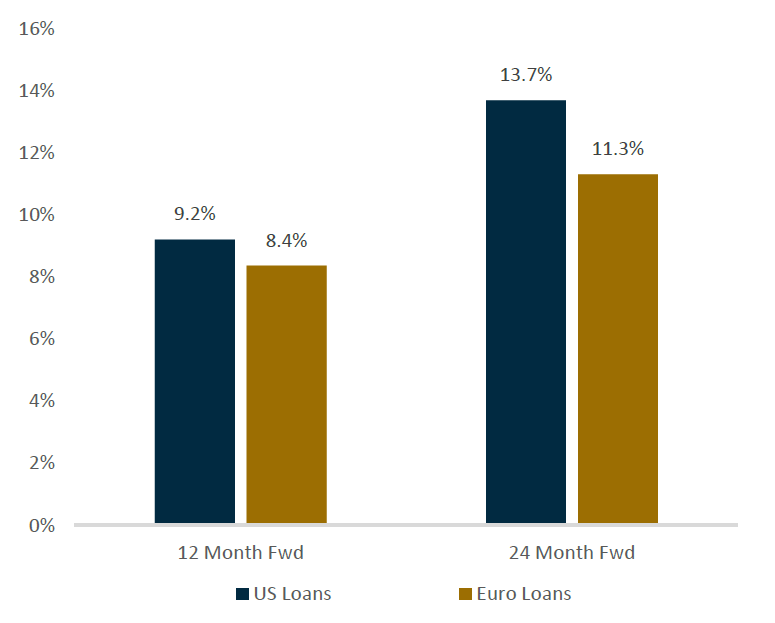

Additionally, when loan and high yield spreads widen past 800 bps, if they were to return to their historical averages in the next 12 or 24 months, potential returns in that space may be significant as illustrated below.

Chart 7 - Forward Returns When Loan Spreads Are Between 600-800 bps

Chart 8 - Median 24M Forward Return Potential vs Frequency

Alternative credit provides multiple ways to find value and protection in different market conditions. CLO Debt in particular has consistently provided a premium to corporate yields across rating classes, ranging from 3.5% for single-A tranches to 9.3% for double-B rated tranches. Most recently, shorter-dated, de-levering deals that have substantial loss protection have been attractive, and we are also starting to see strong value in clean, post-COVID-19 issuance. Regardless of the market environment, the Ares approach to investing with full transparency to the underlying assets allows for the ability to sift through a variety of available investment opportunities to find the assets that best provide the combination of current income with loss protection, which we can combine with loans and bonds to build a portfolio that meets our investors’ needs.

Conclusion

We believe the “sweet spot of credit,” comprised of corporate and structured markets, offers a compelling opportunity for Australian investors seeking diversification and stable current income in varied market environments. To be successful in the so-called “sweet spot,” we believe an arduous focus on capital preservation and the flexibility to select the most attractive relative value are key.

We believe nimble and flexible style of portfolio management with the ability to dynamically allocate across asset classes when shifts in relative value occur is important.

Further, we believe the ability to identify and unlock value especially in currently volatile and bifurcated markets is a strength. Finally, with capital preservation as a key characteristic of the strategy, managers should be intently focused on finding those opportunities with optimal downside protection and lower volatility.

Looking for alternative income?

Ares takes both a bottom-up and top-down approach, with a deep focus on disciplined credit selection and active asset rotation, as well as current, and forward looking global macroeconomic and technical factors impacting each sector. For more information, fill in the contact form below, or visit our website to learn more.

Written by Charles Arduini, Seth Brufsky, Boris Okuliar and myself. To view the full article, including relevant sources, please click on the pdf below

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Samantha is a Partner, Portfolio Manager and Head of U.S. Liquid Credit Research in the Ares Credit Group, where she is primarily responsible for managing Ares' U.S. bank loan credit strategies. Samantha serves as a Vice President and one of four Portfolio Managers for the Ares Dynamic Credit Allocation Fund (NYSE:ARDC). She also serves as a member of the Ares Credit Group's U.S. Liquid Credit Investment Committee, and the Ares Dynamic Credit Allocation Fund Investment Committee. Prior to joining Ares in 2004, Ms. Milner was an Associate in the Financial Restructuring Group at Houlihan Lokey Howard & Zukin, where she provided advisory services in connection with restructurings, distressed mergers and acquisitions and private placements.

Featuring

Charles Arduini,

Ares Wealth Management Solutions

Charles is a Partner, Portfolio Manager and Strategy Head for CLOs in the Ares Credit Group. Mr. Arduini serves as a Vice President and Portfolio Manager for the Ares Dynamic Credit Allocation Fund, Inc. (NYSE:ARDC). Additionally, he serves as a member of the Ares Dynamic Credit Allocation Fund Investment Committee. Prior to joining Ares in 2011, Mr. Arduini was a Managing Director at Indicus Advisors LLP, where he focused on structured credit investment opportunities. Previously, Mr. Arduini was Director of Structured Credit in the Fixed Income Investment Group and a Manager in the Risk Management Group at TIAA-CREF. Mr. Arduini is a CFA® charterholder and a member of the New York Society of Security Analysts.

Seth Brufsky,

Ares Wealth Management Solutions

Seth is a Partner in the Ares Credit Group, Co-Head of Global Liquid Credit, Portfolio Manager and a member of the Management Committee of Ares Management. Mr. Brufsky also serves as a Director, President, Chief Executive Officer and Portfolio Manager of the Ares Dynamic Credit Allocation Fund, Inc. (NYSE:ARDC). Additionally, he serves as a member of the Ares Credit Group's U.S. Liquid Credit Investment Committee and the Ares Dynamic Credit Allocation Fund Investment Committee. Prior to joining Ares in 1998, Mr. Brufsky was a member of the Corporate Strategy and Research Group of Merrill Lynch & Co., where he focused on analyzing and marketing non-investment grade securities.

Samantha Milner,

Ares Wealth Management Solutions

Samantha is a Partner, Portfolio Manager and Head of U.S. Liquid Credit Research in the Ares Credit Group, where she is primarily responsible for managing Ares' U.S. bank loan credit strategies. Samantha serves as a Vice President and one of four Portfolio Managers for the Ares Dynamic Credit Allocation Fund (NYSE:ARDC). She also serves as a member of the Ares Credit Group's U.S. Liquid Credit Investment Committee, and the Ares Dynamic Credit Allocation Fund Investment Committee. Prior to joining Ares in 2004, Ms. Milner was an Associate in the Financial Restructuring Group at Houlihan Lokey Howard & Zukin, where she provided advisory services in connection with restructurings, distressed mergers and acquisitions and private placements.

Boris Okuliar,

Ares Wealth Management Solutions

Boris is a Partner in the Ares Credit Group, Co-Head of Global Liquid Credit, Portfolio Manager and a member of the Management Committee of Ares Management. Additionally, he serves as a member of the Ares Credit Group's European Liquid Credit and European Direct Lending Investment Committees. Prior to joining Ares in 2016, Mr. Okuliar was a Managing Director and Head of Capital Markets for Global Market Strategies at The Carlyle Group, where he focused on sourcing credit investment opportunities from banks and sponsors, syndicating excess risk, and developing new business opportunities.

........

The information in this publication is current as at the date of publication and is provided solely by Ares Management LLC (Ares). Ares is exempt from the requirement to hold an Australian Financial Services Licence. Ares is subject to regulation by the Securities & Exchange Commission of the United States of America under US laws, which differ from Australian laws. None of Ares Australia Management Pty Limited, Fidante Partners Limited, nor any of their associates, has prepared the information in this publication and accept no liability whatsoever in relation to it.

This publication is only made available to 'wholesale clients' or 'sophisticated investors' under the Corporations Act 2001 (Cth) in Australia.

This publication has been prepared without taking into account any person's objectives, financial situation or needs. Any person receiving the information in this publication should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting on the advice. Persons receiving this information should obtain and read any disclosure document relating to any financial product to which the information relates before making any decision about whether to acquire that product.

No reliance: This publication is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The publication has not been independently verified. None of Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd, nor any of their respective related bodies corporates, associates and employees, make any republications, warranty or undertaking (express or implied) and accepts no responsibility for the adequacy, accuracy, completeness or reasonableness of the publication or as to the performance of any product. The information contained in the publication does not purport to be complete and is subject to change. No reliance may be placed for any purpose on the publication or its accuracy, fairness, correctness or completeness. None of Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd, nor any of their respective related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the publication or otherwise in connection with the publication. Any forward-looking statements in this publication: are made as of the date of such statements; are not guarantees of future performance; and are subject to numerous assumptions, risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Ares undertakes no obligation to update such statements. Past performance is not a reliable indicator of future performance.

Confidentiality and intellectual property: This publication is confidential and may not be copied, reproduced or redistributed, directly or indirectly, in whole or in part, to any other person in any manner.

Risk: no person guarantees the performance of, or rate of return from, any product or strategy relating to this publication, nor the repayment of capital in relation to an investment in such product or strategy. An investment in any such product or strategy is not a deposit with, nor another liability of, Ares, Fidante Partners Limited, Ares Australia Management Pty Ltd nor any of their respective related bodies corporates, associates or employees. Investment in any product or strategy relating to this publication is subject to investment risks, including possible delays in repayment and loss of income and capital invested.

This may contain information sourced from Bank of America, used with permission. BANK OF AMERICA IS LICENSING THE ICE BOFA INDICES AND RELATED DATA “AS IS,” MAKES NO WARRANTIES REGARDING SAME, DOES NOT GUARANTEE THE SUITABILITY, QUALITY, ACCURACY, TIMELINESS, AND/OR COMPLETENESS OF THE ICE BOFA INDICES OR ANY DATA INCLUDED IN, RELATED TO, OR DERIVED THEREFROM, ASSUMES NO LIABILITY IN CONNECTION WITH THEIR USE, AND DOES NOT SPONSOR, ENDORSE, OR RECOMMEND ARES MANAGEMENT, OR ANY OF ITS PRODUCTS OR SERVICES.

This may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard & Poor’s. Reproduction and distribution of third-party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. THIRD PARTY CONTENT PROVIDERS GIVE NO EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. THIRD PARTY CONTENT PROVIDERS SHALL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, EXEMPLARY, COMPENSATORY, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES, COSTS, EXPENSES, LEGAL FEES, OR LOSSES (INCLUDING LOST INCOME OR PROFITS AND OPPORTUNITY COSTS OR LOSSES CAUSED BY NEGLIGENCE) IN CONNECTION WITH ANY USE OF THEIR CONTENT, INCLUDING RATINGS. Credit ratings are statements of opinions and are not statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. They do not address the suitability of securities or the suitability of securities for investment purposes and should not be relied on as investment advice.

REF: CP-00514

2 topics

Partner, Portfolio Manager and Head of U.S. Liquid Credit Research

Ares Wealth Management Solutions

Samantha is a Partner, Portfolio Manager and Head of U.S. Liquid Credit Research in the Ares Credit Group, where she is primarily responsible for managing Ares' U.S. bank loan credit strategies. Samantha serves as a Vice President and one of four...

Expertise

Comments

Comments

Sign In or Join Free to comment