The unwinding of QE in 4 charts

Paul Wylie

Mason Stevens

In October 2017 we wrote that our biggest concern for the market was the unwinding of Quantitative Easing (QE). At the time, we used Marc Faber's analogy which is repeated below:

"If you have four asset classes in a room - real estate, bonds, equities and commodities; and in this room you have the Federal Reserve, in the form of Mr Bernanke flying around in his helicopter dropping dollar bills on you, then he can control the quantity of dollar bills that will come into this room, but what he doesn't control is where it will go to. At times it can go into real estate, and at other times it can go into commodities and so on."

We wrote at the time, "The key is that all money must go into one of those asset class piles eventually. If too much money goes into one asset class, it becomes overvalued. If one asset class is overvalued, then another asset class must be undervalued. But if the Federal Reserve dumps a whole bunch of cash into that room (instead of a trickle), what happens? Well, as we have seen with QE, all asset classes go up. QE money eventually finds its way into every one of those piles. It inflates all asset prices.

So, what happens if QE is removed by the Federal Reserve (and other central banks around the world)? The most likely outcome is that the opposite happens, and all asset classes deflate. The Fed realises this and therefore intends to remove QE at a glacially slow pace. They hope markets won't notice such a gradual removal process, and that the effects of inflation will overpower the effects of reducing QE."

How is it playing out so far?

A year on, and with net central bank support firmly being unwound, we can see the effect on markets.

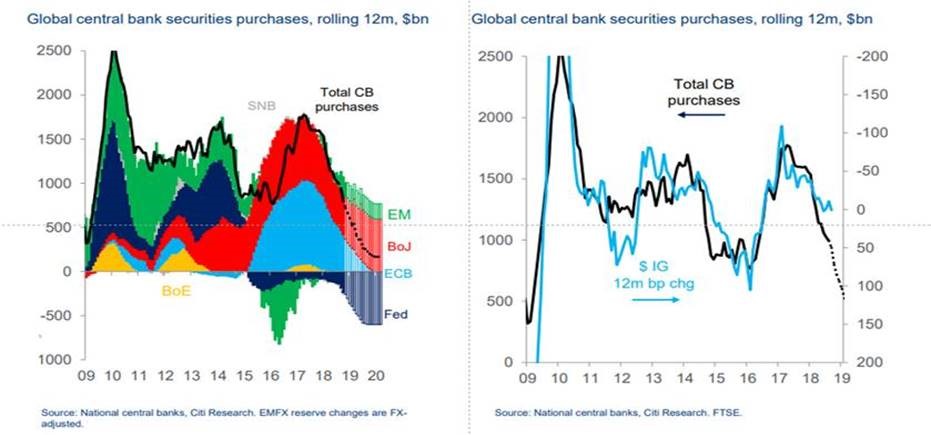

The Fed is already reducing the size of its balance sheet. Other central banks are still expanding theirs but at a reducing rate, a trend that will continue (see charts below).

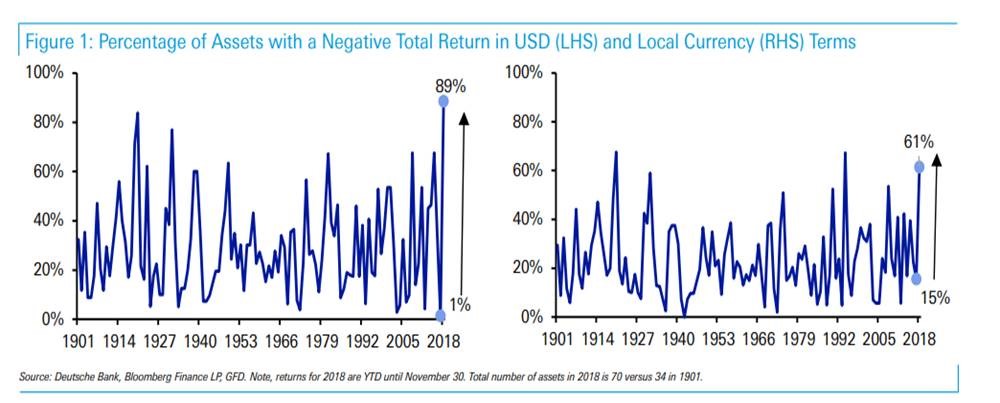

The effects can be seen in the following charts. They show the proportion of assets with a negative return year-to-date (to 30 November 2018) in USD and Local Currency terms.

Just as QE inflated all asset prices when being implemented, it is doing the opposite when being unwound.

The high percentage of assets with negative returns this year seems to be consistent with the reduction in net purchases by central banks this year. Given this is expected to continue, it will be something that will continue to weigh on performance next year, particularly for equities.

What about bonds?

Whilst bonds are not immune from these effects (credit spreads are widening and overseas bond index returns are negative this year), bonds have something that equities do not.

They benefit from a fixed maturity, which means that although bond prices might vary today, provided you don't sell between now and maturity, you know exactly what you are going to get back. You are not subject to the whims of the market price. The closer the bond is to maturity, the closer to par value the bond trades. To use a bond market phrase, you benefit from the "pull to par".

The pace of QE unwind is not set in stone and, like interest rates, will be data-dependent.

However, its effects will continue to overshadow financial markets next year and beyond.

--

This article is prepared by Mason Stevens Limited (Mason Stevens) ABN 91 141 447 207 AFSL 351578 and is general advice only and does not take into consideration yours or your client’s personal objectives, financial circumstances or needs and should not be relied upon as personal advice. You should consider this information, along with all of your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Securities, by nature, rise and fall and as a result investing in securities including derivatives involves risk. Past performance is not a reliable indicator of future performance and may not be achieved in the future. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.

Mason Stevens ensures that the information provided is accurate and complete but does not warrant its accuracy or reliability. Opinions and or information may change without notice and Mason Stevens is not obliged to update you if the information changes. Mason Stevens and its associated companies, authorised representatives, agents and employees exclude to the full extent by law, liability of whatever kind, including negligence, contract, fiduciary duties or otherwise, to investors or anyone else in respect of any loss or damage, including indirect or consequential loss or damage, foreseeable or not, arising from or in connection with this information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Paul is an experienced global credit portfolio manager, having recently held the positions of Global Head of Credit Solutions and Strategic Trading for Lloyds Banking Group.

4 topics

Paul Wylie

Fixed income Investment Strategist

Mason Stevens

Paul is an experienced global credit portfolio manager, having recently held the positions of Global Head of Credit Solutions and Strategic Trading for Lloyds Banking Group.

Paul Wylie

Fixed income Investment Strategist

Mason Stevens

Paul is an experienced global credit portfolio manager, having recently held the positions of Global Head of Credit Solutions and Strategic Trading for Lloyds Banking Group.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management