Does this mark the end of value investing?

The unfortunate recent underperformance of value has many investors calling the end of value investing as a style and suggesting that it is structural not cyclical. The problem with answering such a question is that the underperformance of value for such a long period is unprecedented and thus will always lead many to question whether it is different this time. The folly in assuming riskless growth for decades is illustrated by the number of service sectors that have been shut down in this COVID-19 crisis.

Economic dislocations such as one we are in will see substantial changes to how people live their lives and thus the economic upheaval will be profound and long term.

There will be winners and losers and it is up to active bottom-up managers to determine which is which.

The academic shorthand methods of value investing find it difficult to account for the new wave of companies that have large ‘brand value’ and invested R&D that account for a large percentage of the company’s worth. This naive systematic valuation approach tends to ignore anything beyond the near term and is arbitraged out by quant systems quickly.

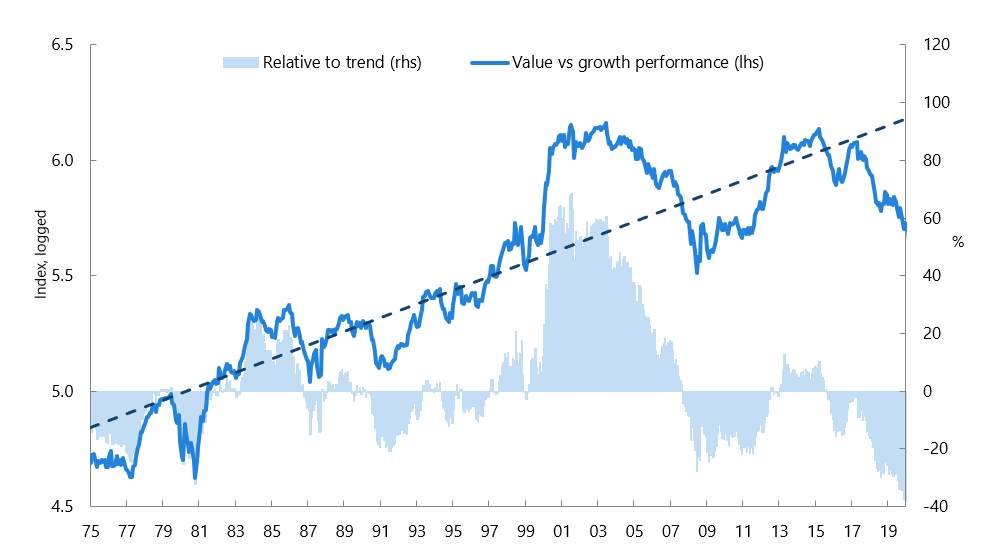

Chart 1 - MSCI Australia value relative to growth

Source: Datastream, Deutsche Bank, Bloomberg, Nikko AM

Our version of value is “intrinsic value”. This approach accounts for future growth, its associated risks and potential accounting distortions and adjusts for the economic cycle, thus appropriately valuing cash flows based on conservative long-term assumptions. The implications of our investing style is that we are comfortable at times owning stocks that may be trading at a high headline multiple, so long as the enterprise trades at an attractive discount to our estimate of its true intrinsic value.

The efficacy of value investing is driven by basic human nature of fear and greed whereby investors buy and keep winners and sell and avoid the losers. The result is that investors expect winners to thrive forever and losers to struggle forever and thus price companies according to this theory.

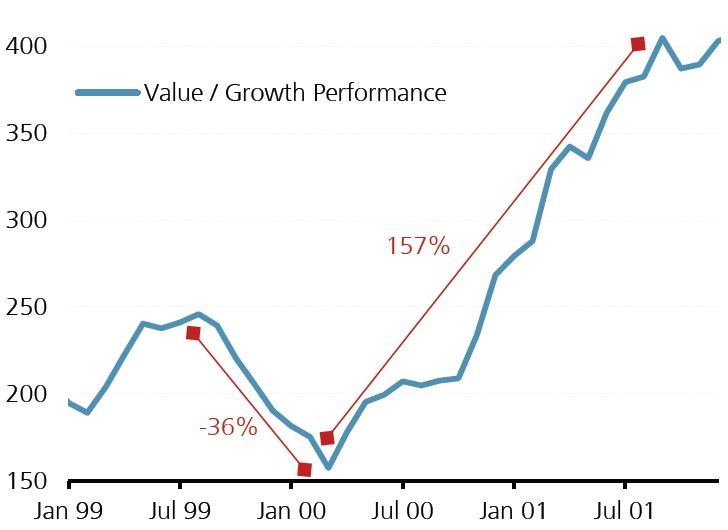

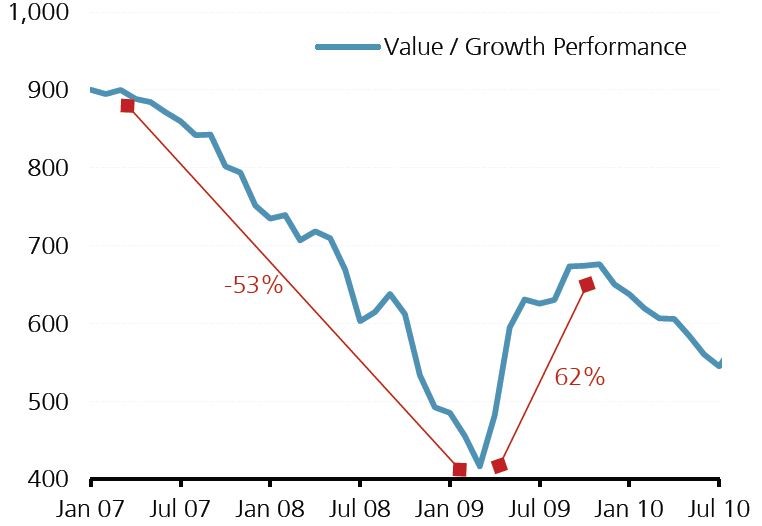

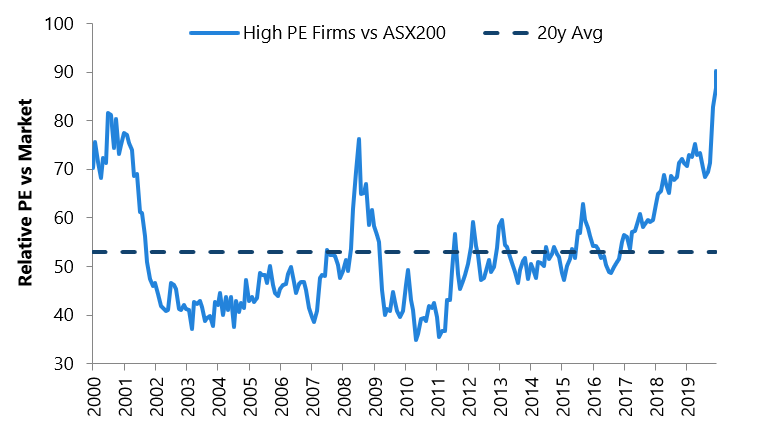

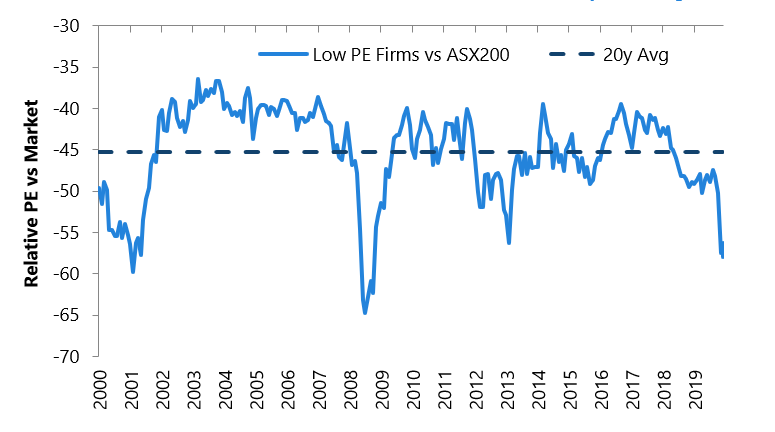

Value stocks tend to be pro-cyclical and have historically performed strongly coming off the bottom of an economic cycle. The bursting of the dot-com bubble led to a switch to value and the GFC also caused a reversal back to value (Charts 2 & 3). The value drawdown that started at the beginning of 2017 is one of the worst investors have witnessed as not only has growth pulled ahead but value has lost ground as shown in Charts 4 and 5 where low PE stocks are trading 12% below long-term averages but high PE stocks are trading 36% above. The high premium for high PE stocks is illustrative that growth continues to trade at a significant valuation premium relative to earnings growth expectations. Therefore, the forward PE of growth is extremely elevated on both an absolute basis and relative to value.

Chart 2 - Dot-com bubble burst

Source: Lessons from styles about the downturn & recovery, UBS

Chart 3 - Global Financial Crisis

Source: Lessons from styles about the downturn & recovery, UBS

Chart 4 - High PE trade at a 90% premium to the market, which is 35% above the 20-year average

Source: Goldman Sachs Investment Research, FactSet, as at 4 May 2020

Chart 5 - Low PE firms trade at a 58% discount to the market, which is 12% below the 20-year average

Source: Goldman Sachs Investment Research, FactSet, as at 4 May 2020

How we have responded—Spotlight on the CVA strategy

The fastest bear market in history followed by one of the fastest bull markets has made investing difficult, particularly given the unprecedented times driven by global government shutdowns. Even the word unprecedented has been searched an unprecedented amount of times.

Adjustment to our earnings and valuations were a priority given the speed and depth of the dislocation with particular emphasis on balance sheet, cash flow and scenario analysis around the impacts. This resulted in identification of opportunities that provided attractive risk adjusted returns. New positions of Transurban and Telstra were traditional defensive stocks that have been sold off and thus presented opportunities that are rare. In the case of Transurban, the high quality defensive road assets were being ignored due to the risks of a capital raising. Our entry into the stock was based on a view that we were comfortable supporting a raising if it indeed occurred. The stock has subsequently re-rated substantially.

We continue to take profits in a number of our winners such as Coles, RIO and Metcash and rotate them into more attractively valued stocks that should do well as the economy comes out of hibernation. We are starting to dip our toe back into the banks after having a large underweight for the last six months. Nikko AM have been supportive of companies such as NAB, QBE, G8 Education, Lend Lease and Oil Search in their capital raisings allowing them to navigate the uncertain and changing economic landscape.

Conclusion

The tough decade for value investors has created attractive investment opportunities that a well-disciplined value investor can harness. Our process is well positioned to take advantage of the opportunity set that requires a long term investment horizon that looks through the current uncertainty; a detailed bottom-up focus that identifies attractively priced companies that we believe are positioned to come through the downturn. It is worth reflecting that for a value investor to ignore growth is as foolish as a growth investor to ignore the price—owning only the most overpriced stocks.

Stay one step ahead

We manage using an intrinsic value style that seeks to identify good value stocks that offer the best compromise between risk and expected return. Click 'follow' to be the first to read our latest insights, including where we are finding the most compelling opportunities on the ASX.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was Director, Corporate Finance with Westpac, a Senior Resource Analyst with Ord Minnett and in his early career, a geologist working with a number of resource companies. Brad has portfolio management responsibilities for the Tyndall Australian Share Wholesale Fund and Tyndall CVA Plus Strategy. He has analyst responsibilities for Banks.

1 topic

11 stocks mentioned

Tyndall AM

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was...

Expertise

Tyndall AM

Brad joined the business in 2002. He has 28 years’ experience primarily in the funds management and stockbroking industry, and has overall responsibility for managing the Australian equities team, process and portfolios. Prior to joining, Brad was...

Expertise

Comments

Comments

Sign In or Join Free to comment