The world’s biggest hussle

Alex Pikoulas

Harper Bernays

There is something quite mystical about government bonds. It is astounding that such a simple financial instrument could be held in such high regard that it can offer an expected negative real return and still be considered a mainstay investment tool for many. Government bonds have become the greatest hussle of all time.

Past performance guarantees lower future return

Bond returns are purely mathematical. The return from inception to maturity is fixed, the only question is the path of that return. A capital gain can be made through interest rates falling, but that only represents a “bring forward” of future returns, and the subsequent return to maturity will be equal to the now-lower interest rate.

The only determinant of long term bond returns is the yield to maturity at the time of purchase. If you buy a bond and hold it to maturity the total per annum return you receive is the yield at which you bought the bond. Period. Importantly, even if you actively manage a bond portfolio and don’t hold individual bonds to maturity the return over the long term can also only mathematically equal the moving average of the prevailing interest rate. This is just a simple mathematical fact.

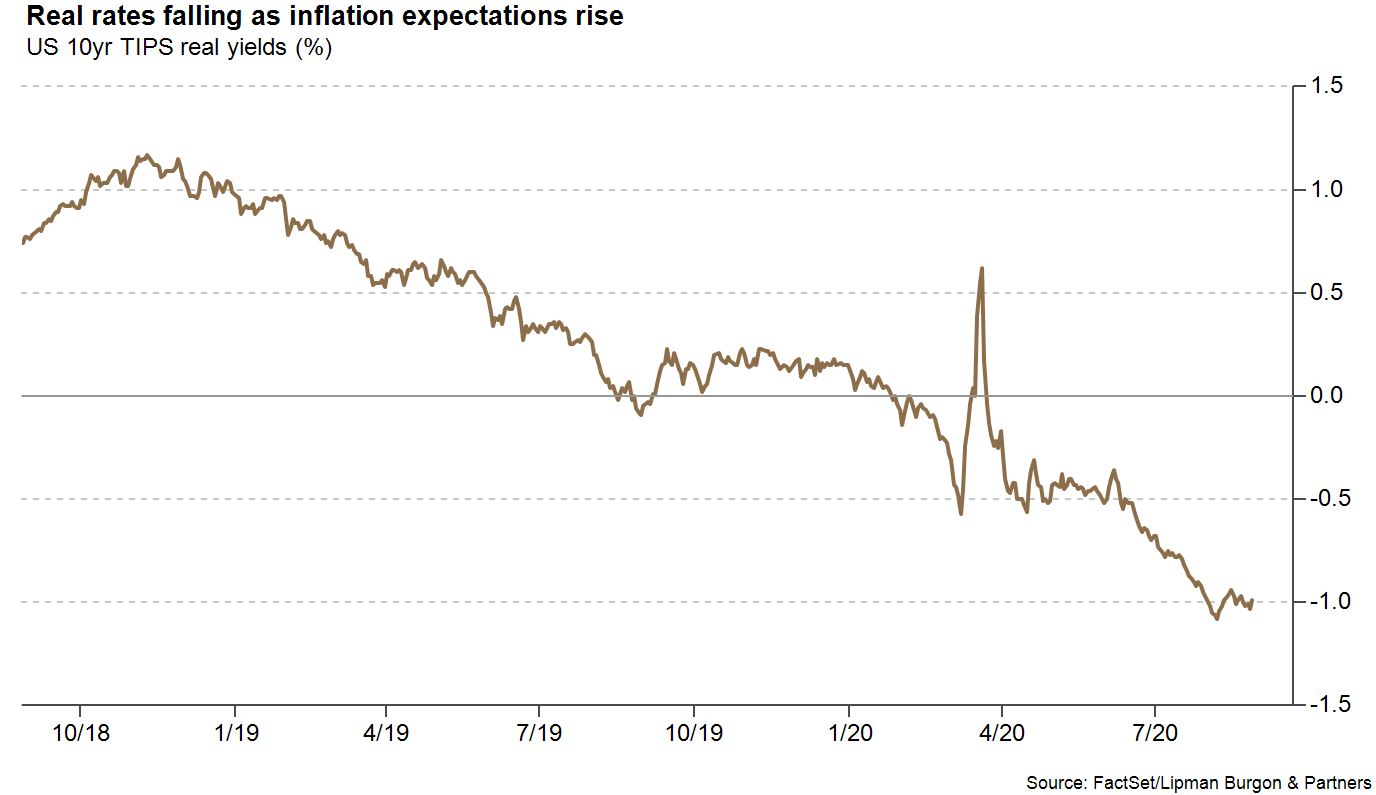

Negative real rates here to stay

Global nominal interest rates collapsed with the onset of COVID-19. 10yr government bond yields in the US and Australia fell to ~0.5% in March and have since risen to 0.75% and 0.92% respectively. In contrast to the increase in nominal yields since March, real yields have fallen a further 0.5% in the last five months to -1% as inflation expectations have increased (see chart below). This shift is important because it is ultimately a real return that investors seek.

Negative real rates are likely to remain in advanced economies for an extended period for one key reason – the high level of government indebtedness.

Advanced economies have reached a new record debt/GDP level as economic stimulus packages support economies that have been shuttered. The last time the world reached such high levels of public indebtedness was the result of wartime spending in WWII.

After WWII debt/GDP in the US declined for 30 years. The entire decline was driven by nominal GDP growth rather than absolute debt reduction. Nominal GDP growth was driven by a productivity boom and helped by higher inflation in the later years.

Interest rates and inflation are important drivers of debt burden and nominal GDP growth (particularly when productivity growth is low as it is today). Without government budget surpluses, population growth or a productivity boom (none of which appear likely), the only way out of high government indebtedness is through persistently negative real interest rates.

Fed Chair Powell’s speech on 27 August at the annual Jackson Hole economic policy symposium gave some insights into the outlook for nominal levels of interest rates and inflation. Powell stated that “inflation that is persistently too low can pose serious risks to the economy” because it leads to low interest rates, taking away a key tool of the Federal Reserve to stimulate the economy when needed.

By implication, Powell is saying that negative policy rates are not part of the tool kit, which is consistent with the message from RBA Governor Philip Lowe. Powell also stated that “assessments of the potential or longer-run, growth rate of the economy have declined” from both slowing population growth and productivity growth. So with this in mind, the Fed have increased their inflation target by seeking “to achieve inflation that averages 2% over time. Therefore, following periods when inflation has been running below 2%, appropriate monetary policy will likely aim to achieve inflation moderately above 2% for some time”. This move had been telegraphed and was widely anticipated.

Could inflation overshoot to say above 4%? This is difficult to predict. In the decade-long expansion post the GFC in the US the historically strong labour market did not trigger a significant rise in inflation. Many commentators cite the current combination of large fiscal and monetary stimulus as likely to see significantly increased inflation in the future, however offsetting that is an enormously increased global labour pool driven by countries such as China and India entering the global economy.

The spread between interest rates and inflation (real rates) is the more important driver of value creation from government bond investments over time, and also significantly impacts the outlook for assets that have some inflation protection such as equities, real assets and gold.

Quasi default

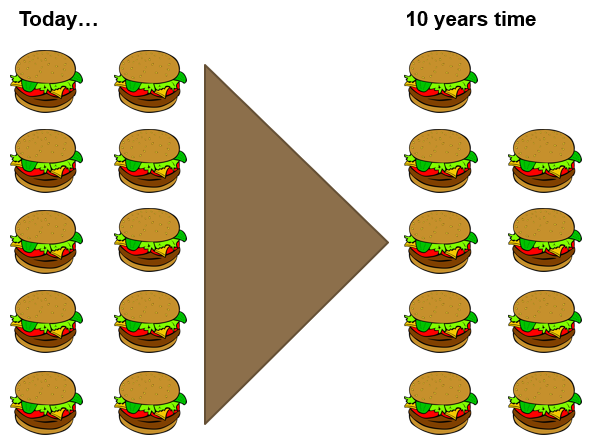

Real interest rates of -1% on US 10yr government bonds represent a decline in purchasing power of 10% over the life of that bond. It’s hard to fathom why someone would invest in an instrument that has an expected return over its life of -10% in real terms. If you gave me 10 hamburgers and I gave you back 9 hamburgers in 10 years time would you consider that full and fair payment?

In most people’s language if a borrower pays back less than the amount lent it is considered default... in this case it is dressed up as a nominal gain in a currency that is slowly declining in value (inflation). Incredibly though it is not being disguised at all… the Fed have told us that they are targeting inflation that is higher than bond yields.

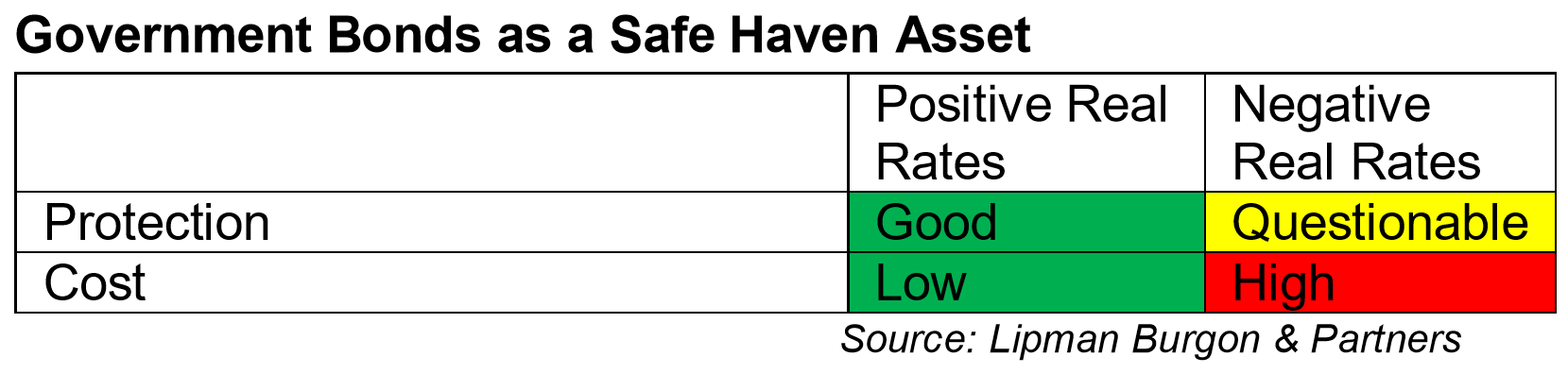

Disqualified as a safe haven asset

Government bonds have traditionally been seen as a safe haven asset. A safe haven asset should be assessed using two characteristics:

- The protection it provides your portfolio, and

- The opportunity cost of holding the asset.

When nominal interest rates were higher and real interest rates were positive the protection government bonds provided was significant. During recessionary periods interest rates were reduced leading to increases in bond prices. Today, with interest rates globally around the effective zero lower bound (implicit in the Fed’s commentary) there is little scope for any capital appreciation. As such the protection government bonds now provide to portfolios is now questionable.

Similarly, with a long term holding of government bonds certain to reduce in real value the opportunity cost of this investment has become very high.

Beware close relatives

The transmission mechanism is a powerful force… risk-free interest rates are the base rate off which most assets are priced. However, there are varying degrees of linkage to the risk-free rate between different asset types. Investment-grade corporate bonds are very closely linked to risk-free rates, whereas private debt is less so.

In an environment where risk-free rates don’t make much investment sense there is also a need to be wary of close relatives. On the other hand, assets that have a friendly relationship with an accommodative policy are likely to continue to perform well. In this extreme environment, this particularly includes assets that carry some inflation protection like equities, real assets (property & infrastructure) and commodities (gold).

A new method of playing defence and receiving income

Government bonds used to provide portfolios with real income as well as defence. These characteristics need to be replaced.

- One strong source of income that is growing in availability is private debt. Banks have been pulling back from lending to various segments of the market due mostly to regulatory pressure. This has opened the door for private capital to fill that void, and some attractive rates can be earned. The private debt market is somewhat opaque and quality manager selection is critical.

- Another growing source of reliable income is absolute return bond funds. These funds use various strategies to generate stable income without taking interest rate duration risk. Replacing the defensive characteristic that government bonds used to bring to portfolios is more difficult.

- Gold is probably the most readily available investment that provides a negative correlation to equity markets in times of economic and market stress. As a store of value gold is also seen as providing protection against inflation and currency debasement, two things that are worth protecting against in these extraordinary times.

Keep it simple

Government bonds are simple fixed coupon instruments. Current anaemically low nominal interest rates of sub 1%, and negative real interest rates, mean that long term government bond holdings are certain to destroy real value.

There is no place for this sort of asset in any portfolio whose objective is to protect and grow long term wealth.

About the series

Livewire asked two of our contributors who have strong views on government bonds to produce a bear versus bull case on this critical sector for fixed income and defensive investors. View the other wires in this series:

- How should investors allocate to government bonds today?

- Why you can’t afford not to own government bonds

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Alex has over twenty years of financial markets experience within leading global investment banks and brings a wealth of knowledge on global financial markets across asset allocation, fund manager selection, risk management, and financial analysis.

3 topics

Alex Pikoulas

Executive Director

Harper Bernays

Alex has over twenty years of financial markets experience within leading global investment banks and brings a wealth of knowledge on global financial markets across asset allocation, fund manager selection, risk management, and financial analysis.

Expertise

Alex Pikoulas

Executive Director

Harper Bernays

Alex has over twenty years of financial markets experience within leading global investment banks and brings a wealth of knowledge on global financial markets across asset allocation, fund manager selection, risk management, and financial analysis.

Expertise

Comments

Comments

Sign In or Join Free to comment