Three Small Cap Recovery Stocks

Markets remain divided on whether we’ve seen the bottom or not. But whenever stocks fall to the extent they did in March, and uncertainty reaches the levels that it has, it is worth getting interested.

Depending on your time horizon this period may well prove to be a fantastic buying opportunity, but it will be stock specific as COVID-19 divides the winners and losers. The sort of change this crisis has created, and the existing trends it has accelerated, will prove company makers for a select group of stocks.

Here’s 3 stocks set to benefit as we emerge from this crisis and the recovery begins.

5GN Networks (ASX:5GN) – Market Cap $60m

I’ll kick off with 5GN as it is a stock that I’ve written about on Livewire twice before (here and here).

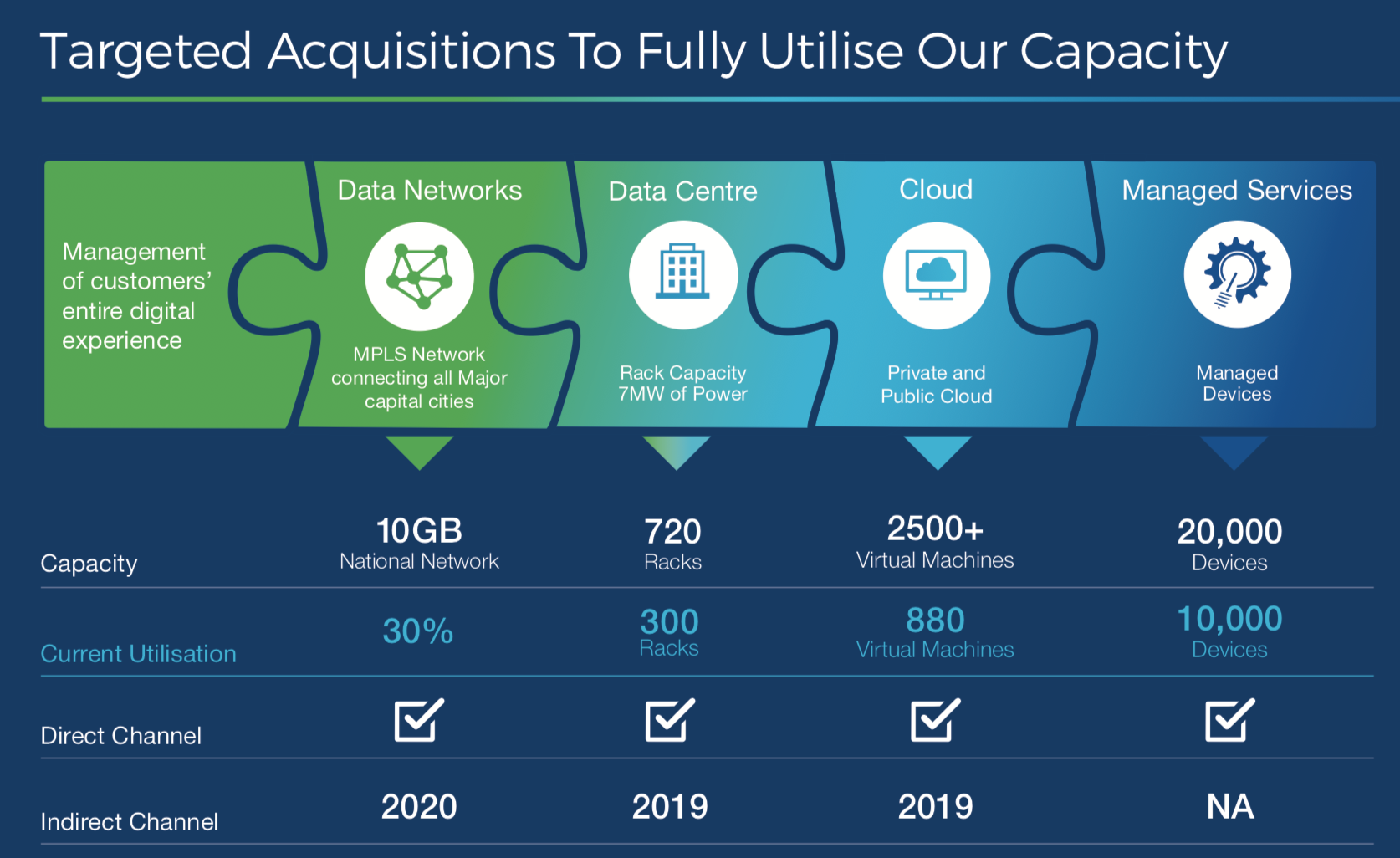

5GN provides telco, managed cloud, data centre and connectivity services to business and enterprise clients.

The ‘shift to the cloud’ is one of the thematics that has accelerated as a result COVID-19. If you didn’t have the ability for your employees to seamlessly work from home going into this crisis you were left behind. While we may not all end up working from home on the other side of this the trend towards flexible working will certainly accelerate.

The business saw no material negative impact from COVID-19. There has been a marked increase in remote access services as customers rush to allow employees to work from home and as we emerge from lockdown they will have a large pipeline of new customers to shift to the cloud and support the growth of their annuity revenue base (>80% of total revenue).

5GN is generating $1.5-$2m of operating cash flows per quarter and has given guidance for a mid-range of c.$6m EBITDA in FY20. I expect the business to be run-rating at c.$7m EBITDA as they enter FY21, putting it on a multiple of 8-9x.

5GN have spent the last 12 months buying data centres (one in Melbourne, one in Sydney) and building out their fibre network. This has given them substantial excess capacity in their infrastructure that, as filled, will result in operating leverage that the market is yet to appreciate.

The tailwinds behind the shift to the cloud will help support organic growth in network and data centre revenue as we emerge from the lockdown. But the real upside for 5GN is acquisitions.

5GN will shift focus to now acquiring managed service providers (MSPs) in order to fill up that capacity. The market is underestimating how accretive some of these deals could be.

MSPs spend a large % of revenue on hosting and data centre services every year. On acquisition, 5GN will be able to incentivize the acquired client base to shift their spend to their own infrastructure and any resulting synergies will be pure margin to the bottom line.

Joe Demase (MD) recently stated they have a number of acquisition targets in the pipeline. He’s also stated that where they typically paid 4-5x EBITDA they are now in a position to pay 3-4x due to less competition for assets.

If they can sustain current run-rate earnings and make one or two acquisitions in the next 12 months then EBITDA should comfortably exceed $10m in FY21. That would make 5GN a candidate to move up the ranks in the small and midcap telco sector, with a resulting multiple expansion likely.

Schrole Group (ASX:SCL) – Market Cap $22m

Schrole is a developer of HR software products for the international and domestic school market. The lead product is Advantage – a platform for the recruitment of teachers at international schools.

Think of a mix of Seek and LinkedIn, designed specifically for schools, with a host of additional modules provided on top of Advantage.

On one side of the platform is schools, about 400 of them today, that pay up to US$7k annual subscription fees. On the other side is candidates (teachers - about 6,000 of them) that pay US$75 to build a premium profile on the platform and engage with potential employers.

SCL has the potential to be a high quality, cash generative business with network effects and winner-take-all dynamics in a growing niche that is disrupting the traditional recruitment process.

That traditional process involves placements, recruitment fairs, face to face meetings & networking. These methods will be near impossible over the next 12 months due to COVID-19.

But international schools are opening up again and the recruitment process continues. It will ramp as we enter the peak recruitment season in the September and December quarters, which are strong ones for Schrole’s revenues and cash flows.

This provides a window of opportunity where existing schools on the platform, and new schools yet to engage with Schrole, will be seeking an alternative means for recruitment, preferencing one that is entirely online.

SCL should be perfectly positioned. I asked the MD about this recently and his response was this:

“Absolutely. Our platform was designed around schools and candidates engaging online. We always felt that attendance at face to face fairs was declining, and that these would in time become less relevant. That has now accelerated to the point that it is hard to imagine any face to face fairs in the next 12 months. International travel restrictions coupled with the fact that people won’t want to be in group meetings will mean that everything has to go online. We are well positioned to capitalize on this and will be looking at other opportunities to provide different levels of subscriptions that our competitors will not be able to match.”– Rob Graham, MD of Schrole Group

Schools need to be on the platform with the most candidates, and candidates need to be on the platform with the most (and best) schools. It will be a market with one or two winners that in the end will likely prove highly profitable and highly valuable.

The key is to be the first to dominate the space. That requires rapid growth.

SCL have 400 international schools out of an addressable market of 11,000. They had A$5.1m of annual recurring revenue (ARR) at 31stMarch and grew at c.30% over the last year when currency fluctuations are stripped out.

That rate of growth is nice but with an opportunity as attractive as this they should be growing at c.100% a year, not 30%. They should be adding 500-1000 schools a year, not 100-150. This is what the market needs to see to really reflect the underlying potential of this business in the share price, which is multiples of current levels if they get it right.

Management knew this and embarked on a strategy to help quickly scale the business through partnerships with larger players.

In this regard, a potentially company making deal was announced this week with Faria Education Group.

Faria provide a broad suite of software products to over 3,000 international schools and 8,000 US domestic schools. They one of the leaders in the space, providing a massive endorsement to SCL.

As part of the deal, Faria subscribed for a convertible note which on conversion will result in 19.99% ownership of SCL. They will participate in, and are incentivized to help drive, the increase in value of Schrole’s business.

Schrole will integrate their full product offering with Faria’s, opening up a massive base of potential customers.

The vast majority of SCL’s A$5.1m of ARR today is from Advantage, and that will be the immediate growth opportunity with Faria, but Verify and Cover now have a path to become meaningful revenue generators in their own right. These both have the potential to generate revenue similar to that of Advantage today.

The potential blue sky is Schrole Connect and how that might be leveraged into Faria’s 8,000 US domestic schools. Connect is SCL’s Advantage platform customized for domestic schools and is yet to generate revenue but has an enormous untapped opportunity in front of it.

It now shapes as an interesting 12 months for SCL. International schools are opening again and recruitment is continuing, with traditional recruitment methods difficult or impossible, forcing schools to try online alternatives. They will have the support and existing 10,000 school network of Faria behind them.

If you fully dilute for the new shares issued to Faria, SCL’s market cap is just $22m. They will have cash of c.$6m post this deal and are nearing an inflection in earnings. Importantly, they now have a path to grow ARR from the current $5.1m to $10m-$20m over the next couple of years.

In a recent podcast interview, I tipped SCL as my candidate to be a 10-bagger and their recent deal with Faria reinforces that view. As the market better understands the significance of the Faria deal and the implications for growth and profitability I suspect it may start to agree.

Elanor Investors (ASX:ENN) – Market Cap $125m

While 5GN and SCL are in sectors likely to experience tailwinds as a result of COVID-19, ENN is quite the opposite. As a property funds management business with large investments in commercial and retail property, as well as a substantial portfolio of tourism assets, it is the kind of stock the market was quick to dump in March and April.

But in beaten up sectors you can often find opportunities. The issues in commercial and retail property are real but ENN’s assets are holding up better than the share price implies.

ENN had $1.50 of NTA on the balance sheet at the last reporting date vs a current share price of $1-$1.10. In this environment you should rightly apply a discount to that NTA. But at the implied discount of 30% on a portfolio of what is mostly high-quality assets that should emerge from this crisis in reasonable shape, that looks decent value in itself.

The real kicker is that at current prices you are getting a well regarded funds management business with $1.7b of FUM, a solid track record and a loyal investor base, many of whom have been through the GFC. And you are getting it for free, if not being paid to buy it, so long as you have confidence in the $1.50 of NTA on the balance sheet.

The funds management business generates c.$13m of recurring revenues a year, before any performance fees. The group typically co-invests to seed new funds, holding 10-20% of their own funds on the balance sheet. With c.$70m of growth capital available to the group, and assuming standard gearing, ENN has the capacity to grow FUM by c.$800m.

ENN’s bread and butter is buying quality assets with short term problems and fixing them up. This kind of environment should be their time to shine. They have an investor base that is likely to back them to purchase distressed assets at good prices through this downturn, and that should set them up well for years to come.

In a couple of years, it is reasonable to expect ENN to be managing $3b+ of FUM and generating $20m+ of recurring management fees. That could justify a valuation greater than the current market cap by itself.

The question becomes, how are their existing assets that comprise the $1.50 of NTA (in managed funds and on balance sheet) performing?

There isn’t space to do a deep dive on all their assets in this note, so I’ll touch briefly on each category.

The commercial fund (ASX:ECF) is holding up quite well. 87% of its income is generated by government, multinational and ASX listed tenants. Occupancy is still 97%+ and they remain on track to meet prospectus guidance of 8.3% funds from operations yield.

They’ve experienced some requests for rent relief but this has mostly been from the smaller retailers surrounding the anchor tenants and shouldn’t have a material impact to income. Distributions are continuing.

The healthcare fund is in similarly good shape although saw an interruption from the pause put on elective surgeries. These properties are tenanted by doctors, day surgeries, specialists, fertility clinics and hospitals, all of which require unique fit outs and typically experience minimal turnover. The long term thematic is attractive here and I’d expect ENN to grow FUM in this space over time.

The retail fund (ASX:ERF) is a bit more uncertain but plugging along reasonably well given current conditions.

Aldi just replaced Big W as the second anchor tenant at Auburn Central. ENN will redevelop this space and from November the relevant rental income will rise from $1m to $3m, a solid return on the capital invested.

There was some impact to their Tweed Heads asset, which sits right on the border, from the border closures. This will normalize soon enough. The retailers providing discretionary products and services will no doubt find it tough. It is hard to quantify what this looks like in the near term.

Then there are the tourism assets, including a portfolio of luxury hotels across Australia held on the balance sheet. No prizes for knowing that tourism has been exceedingly difficult lately. But there is light at the end of the tunnel.

Firstly, essentially all of these assets will receive JobKeeper and government support to get them through the crisis. The two wildlife parks (Mogo and Featherdale) will receive access to a $100m package designed to assists zoos through the crisis. They will likely get to the other side.

Second, as we emerge from lockdowns, ScoMo is increasingly pushing Australians to explore in their own backyard. The Government know they will need to support tourism in this country as it is an integral part of our economy and is not going to be see any international tourists anytime soon.

Any Australian who had intentions to travel overseas in the next 12 months is either going to stay home or redirect those plans domestically. I’d favour the latter for many of them. There will certainly be an impact from depressed consumer confidence but a decent part of the population is likely feeling cooped up at home and itching for a holiday.

Investors should keep in mind that the dollars spent by Australians on domestic tourism dwarfs what international tourists were spending here prior to the crisis. ENN’s tourism assets are some of the best in Australia and generate most of their income from domestic tourists.

If there is anything holding the stock back it is the uncertainty around liquidity and cash flows at the group level. But if you assume only management fees and distributions continue just from the commercial and healthcare funds, the group should still be cashflow positive. Anything else is a bonus.

If there is a need to raise cash in the interim to improve the balance sheet there are two options.

The first is a capital raise, which the market seems to be pricing in, but I don’t think is a certainty by any means. If they did indeed raise it would likely be a very strong buy and would remove the pressure on the share price anyway.

The more likely way they free up cash is to sell down some of their holdings on the balance sheet. Again, if this happens, it should prove a catalyst.

The longer the share price stays at these levels the more interested a potential acquirer is likely to become. There are larger listed property fund managers that would benefit from acquiring a meaningful amount of FUM essentially for free given the NTA discount.

In one or two years I can see a situation where their property assets are returning to normal conditions and the market has confidence in the $1.50+ of NTA on the balance sheet.

The funds management business, which you get for free at current prices, could itself be worth $100m+ at that point, if it isn’t already worth near that today. Prior to the crisis the share price was trading at ~$2.20, implying 70c of value for the funds management business, or approx. $80m.

It could be a bumpy short-term ride but I think ENN is the type of business you can buy at these levels, back the managers, put in the bottom draw for a couple of years and on the other side of this you should do well.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund.

Previously worked for Pie Funds and Bligh Capital.

2 topics

3 stocks mentioned

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

HD Capital Partners

Co-founder of HD Capital Partners and founder of Capital H Management. Portfolio Manager of the Capital H Inception Fund. Previously worked for Pie Funds and Bligh Capital.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management