TOL - 18th Dec, 2020

Three ways to win with decarbonisation

There’s no denying the world is ‘going greener’. A major structural shift in the way we produce and consume energy is underway and will accelerate significantly during the next decade.

Ignoring this is ignoring a generational investment opportunity.

In the last episode for 2020 on Antipodes’ Good Value podcast, we delve into the political and economic tailwinds supporting the decarbonisation super cycle. These include Europe’s ‘New Green Deal’ which is underwritten by a carbon emissions trading scheme, investment in renewables in the US which could be accelerated under a Democratic Presidency even with a split Congress and China’s push into electric vehicles.

Listen to the episode here or continue reading below, where I highlight three ways to gain exposure to the decarbonisation super-cycle.

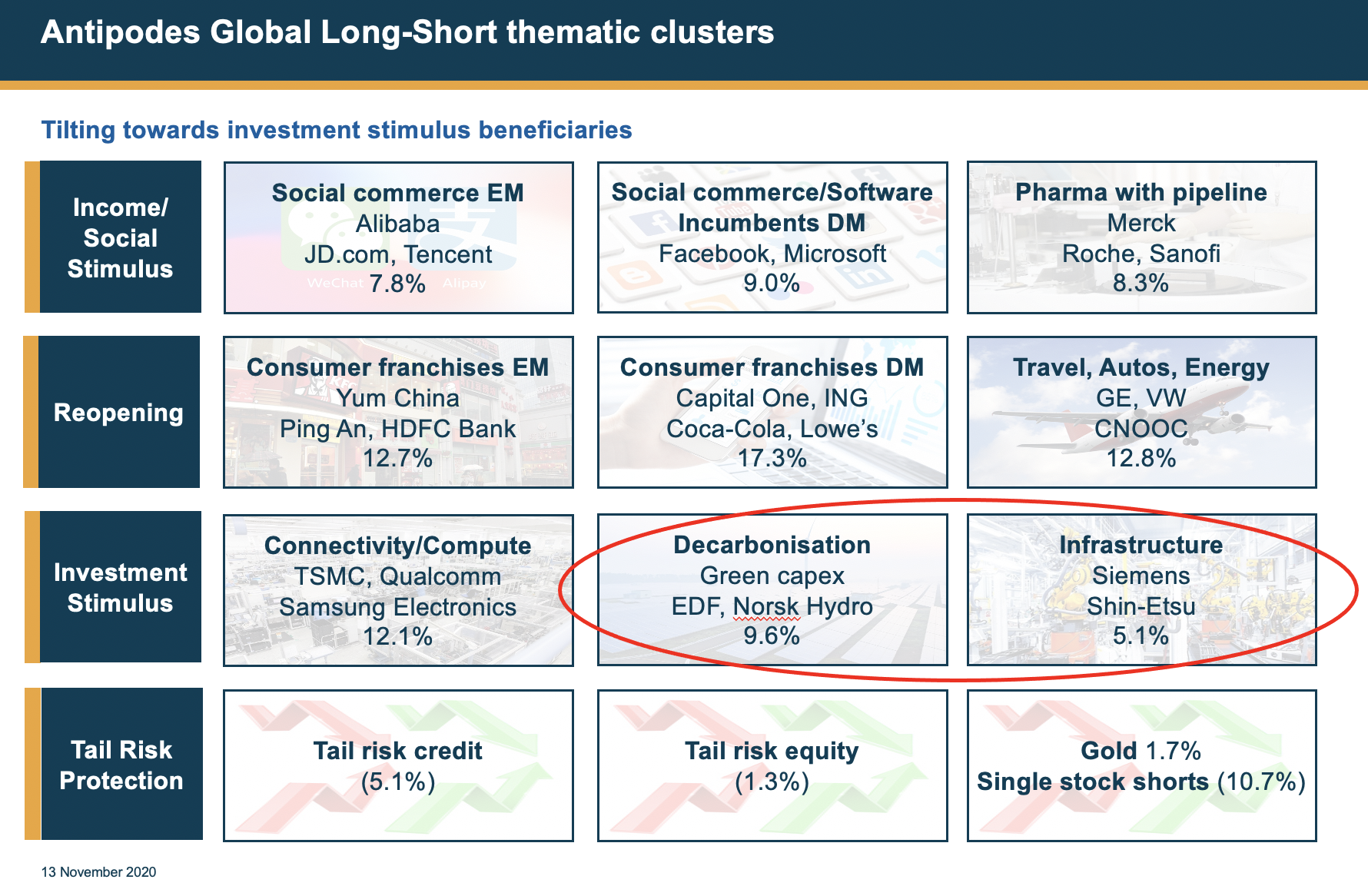

Antipodes’ overall global portfolio exposure to beneficiaries of decarbonisation and infrastructure investment has grown to around 15% (as at November 2020).

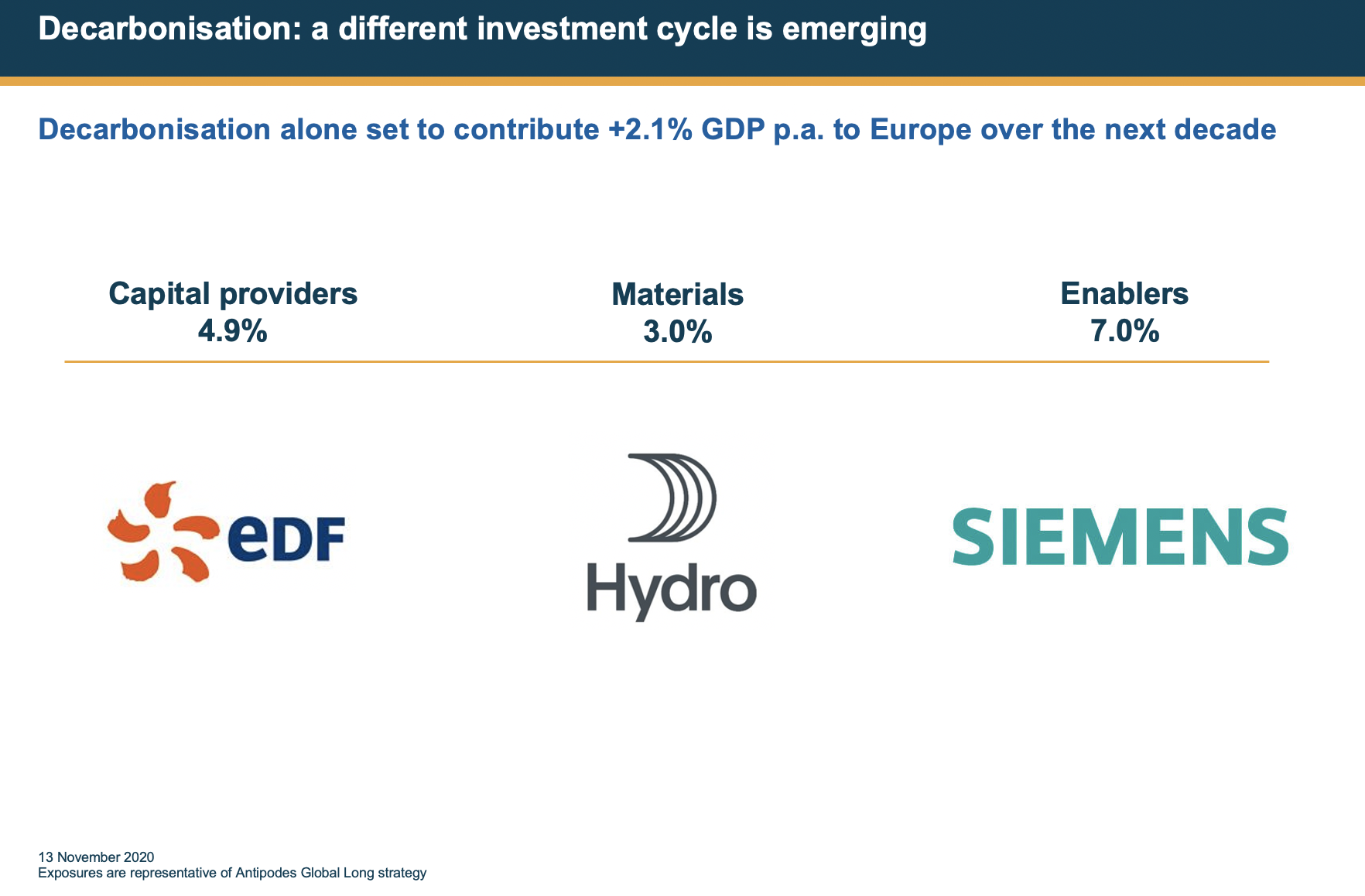

This exposure is split into three key groups – capital providers, materials companies and enablers - where we think winners will emerge. This provides a robust overall exposure to a key long-term structural trend while achieving a protective form of diversification

Capital providers

Antipodes has around a 5% exposure to ‘capital providers’. These are the power companies that are deploying renewables and will get paid a return for greening the grid.

One the of the key holdings in our portfolio is EDF (Electricity de France) which is Europe’s largest low carbon electricity producer. It owns world scale nuclear, hydropower and renewable assets. We see a huge increase in the demand for electricity under Europe’s ‘New Green Deal’ - whether that’s coming from EVs or reducing fossil fuel-based home heating and power generation.

EDF is also well-advanced in its discussions with the regulator to not only increase the price it receives for regulated nuclear power output which would materially boost returns (the speculation is a 15-20% lift in this regulated price), but also undertake a potentially value-creating company split which could see the company separate its nuclear and renewables business into a separate entity, in which current investors will hold shares. This entity will likely become one of the largest owners and operators of renewable assets in Europe and is materially undervalued within the larger group.

Materials companies

We have around 3% exposure to materials companies. One of our larger holdings is Norsk Hydro, a global aluminium producer.

Aluminium smelting might often be thought of as an old-world industry, but usage is increasingly new world given its light-weighting and recyclable properties. Producing aluminium is incredibly energy intensive, which has typically meant a reliance on cheap coal.

But what we love about Norsk Hydro is that it produces its aluminium from predominantly hydropower, which is sustainable. Norsk’s aluminium has a dramatically lower carbon footprint, it’s approximately 80% lower than the coal-based producers. Demand for lower-carbon aluminium will have a profound effect on the supply side too.

In terms of opportunities on the demand side, autos are a great example. The average car today uses around 180kg of aluminium per vehicle while larger EVs, in a bid to offset battery weight, are increasingly replacing steel with aluminium.

For example, the Tesla Model S and the Audi 8 Tron use 700 – 800kg of aluminium per vehicle. That’s a four-fold increase, which is quite typical for EVs. We think demand from EVs, the light-weighting of SUVs, low-energy buildings and packaging will mean aluminium demand can grow at least 3% p.a. Yet Norsk is valued at a 50% discount to the replacement cost of its unique assets.

There are other interesting materials that we have exposure to in the portfolio, such as nickel and copper, which are also key to decarbonisation and electrification.

Enablers

Around 7% of our portfolio is invested in Decarbonisation ‘enablers’. The Siemens group is a great example.

Siemens parent is a global leader in factory automation, and it’s the only company globally that provides both the hardware to make a plant run as efficiently as possible and also the software, which controls and optimises processes.

As we move into a low carbon world, manufacturers will need to re-tool. On the hardware side this will include robots or energy efficient drives and motors to reduce energy consumption.

On the software side, amongst other things, Siemens’ software allows a company to build a “digital twin” of its product. Rather than having to produce endless prototypes, products can be built and stress-tested in the virtual world. This is incredibly efficient.

Siemens has a Smart Infrastructure division which sells energy efficient building, factory and grid control systems to manage power consumption.

There are also two other subsidiaries which will benefit. There’s Siemens Energy, which supplies the high voltage transmission equipment required to reconfigure the grid and is one of only a handful of companies globally that can produce utility scale gas turbines. The end goal may be zero emissions, but gas is an important ‘transition’ energy as it’s greener than coal and can also help manage peak load. And the other subsidiary is Siemens Gamesa Renewable Energy, which manufactures wind turbines and is a global leader in offshore which is the main growth engine of wind penetration – so a clear facilitator of decarbonisation.

Despite how well-positioned Siemens is, its valued at just 16 times 2022 earnings as cyclical businesses globally have fared poorly this year thanks to COVID and concerns around economic health.

We also have exposure to certain automakers and battery companies.

The market and the media are obsessed with Tesla, but there is another automaker – Volkswagen (VW) – which already produces cars at scale, is on the front foot of electrification, and will likely produce more EVs than Tesla when EV adoption begins to properly ramp up. Only VW is valued at single digit multiples.

Learn more about Antipodes Partners and the firm's approach to investing in global equities.

Visit Antipodes website, or click the 'contact' button below to get in touch.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

In almost two decades of investing in equities based in Sydney and Singapore, Alison has worked through various market cycles and navigated major market events. Alison is an investment director at Antipodes and a member of the senior investment team.

Prior to joining Antipodes she worked as an investment analyst with Smith Tan Asset Management in Singapore and a deputy portfolio manager at Kingfisher Investments. From 2004 to 2015, Alison was a senior investment analyst at Platinum Asset Management.

........

This communication has been prepared by Antipodes Partners Limited (‘Antipodes Partners’, ‘Antipodes’) ABN 29 602 042 035 AFSL 481580.

Interests in the Antipodes Global Fund (ARSN 087 719 515), Antipodes Global Fund – Long Only (ARSN 118 075 764) and Antipodes Asia Fund (ARSN 096 451 393) (‘Funds’) are issued by Pinnacle Fund Services Limited, ABN 29 082 494 362, AFSL 238371. Antipodes Partners is the investment manager of the Funds. The Product Disclosure Statements (‘PDS’) for the Funds are available at www.antipodespartners.com/funds. Any potential investor should consider the relevant PDS in deciding whether to acquire or continue to hold units in a fund. The issuer is not licensed to provide financial product advice. Please consult your financial adviser before making a decision to invest in a fund.

Antipodes Partners and Pinnacle Fund Services Limited believe the information contained in this communication is reliable, however no warranty is given as to its accuracy and persons relying on this information do so at their own risk. Any opinions or forecasts reflect the judgment and assumptions of Antipodes Partners and its representatives on the basis of information at the date of publication and may later change without notice. The information is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. This communication is for general information only. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. Past performance is not a reliable indicator of future performance. Unless otherwise specified, all amounts are in Australian Dollars (AUD). Options exposure represents the market downside. For put options (typically used to limit potential downside) delta-adjusted exposure is used and for call options (typically used to capture potential upside) exposure is calculated using the current option value.

To the extent permitted by law, Antipodes Partners and Pinnacle Fund Services Limited disclaim all liability to any person relying on the information in respect of any loss or damage (including consequential loss or damage) however caused, which may be suffered or arise directly or indirectly in respect of such information contained in this communication.

The information contained in this communication is not to be disclosed in whole or part or used by any other party without the prior written consent of Antipodes Partners. Antipodes Partners and their associates may have interests in financial products mentioned in this communication.

.jpg)

2 topics

1 contributor mentioned

.jpg)

In almost two decades of investing in equities based in Sydney and Singapore, Alison has worked through various market cycles and navigated major market events. Alison is an investment director at Antipodes and a member of the senior investment...

Expertise

In almost two decades of investing in equities based in Sydney and Singapore, Alison has worked through various market cycles and navigated major market events. Alison is an investment director at Antipodes and a member of the senior investment...

Expertise

Comments

Comments

Sign In or Join Free to comment