Unlocking the Value Inside Enero

Daniel Mueller

Forager Funds

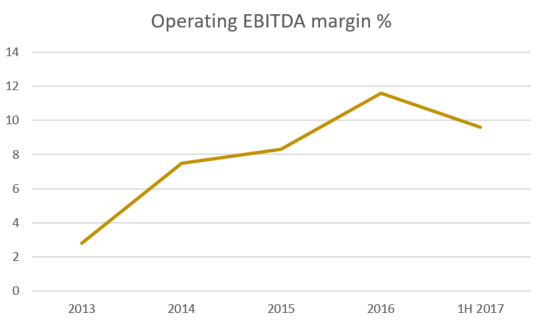

Marketing conglomerate Enero Group (EGG) has been a volatile and frustrating investment in recent years. Following a near death experience under previous management, the current management team gradually increased EBITDA margins. It looked like Enero was reaching its potential after a long, grinding turnaround. But in the last 10 months things started to go wrong.

The Brexit vote led to the depreciation of the pound, where Enero derives almost half of its revenue. This was followed by UK client timidity with the final kick in the guts being the loss of its largest client, Virgin Atlantic, which was 7% of revenue.

Where does that leave things now?

Enero’s Valuation

The stock currently looks expensive on an earnings multiple basis, trading on over 20 times forecast 2017 profit. So it will take years to realise the value of the investment if we have to wait for an earnings recovery.

We need the board and management to take the initiative and unlock the value inherent in the company.

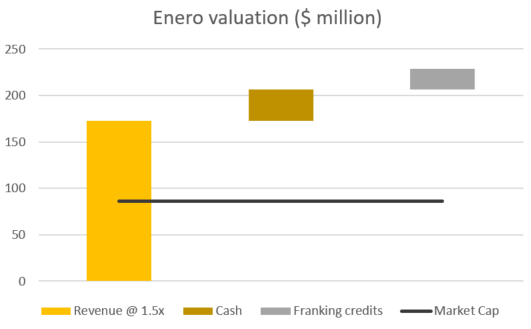

How much could Enero be worth? The current $1.00 share price equates to a market capitalisation of $86m. For this shareholders get $34m of cash, $22m of franking credits and about $110-120m of revenue.

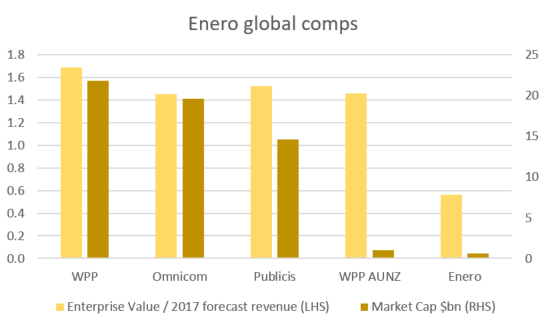

Compared to global peers, $1 per share is an absurdly low price. Enero’s peers trade on an enterprise value to revenue multiple of 1.5 to 1.7 times. Enterprise value refers to the total of a company’s market capitalisation and its net debt.

Since Enero has a net cash position, its enterprise value is just $52m. If it traded on the same multiples as its peers, its enterprise value would be up to four times larger than today. This equates to a share price of $2.30.

So why is Enero trading at less than half of this valuation? There are two main reasons.

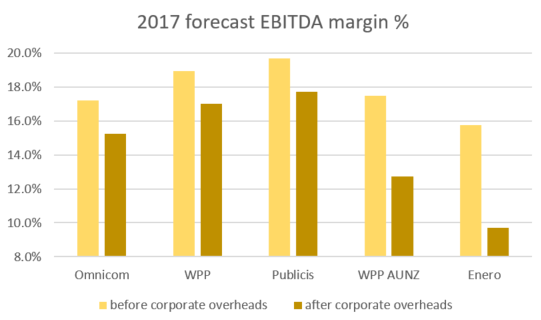

Low Margins a Result of Being Sub-Scale

Enero’s depressed share price is partly a function of being sub-scale. Its operating margins before corporate costs are comparable to global peers. But a relatively low revenue base results in high corporate overheads as a percentage of revenue. Corporate costs are crimping Enero’s margins.

We believe management can do little more to reduce corporate costs following their strong focus on reducing these in recent years. The only way to improve margins is to increase scale, i.e. grow revenue. But this could take years and involve risky acquisitions. A quicker and less risky solution would be for a global peer to acquire Enero.

Restriction on Paying Dividends

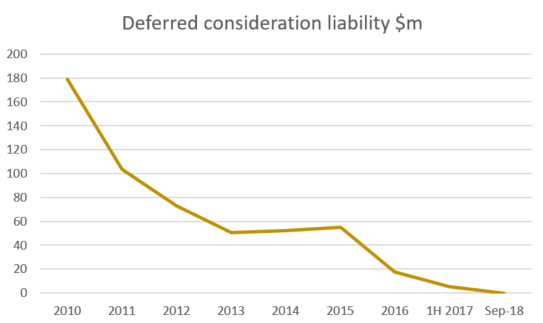

The other main reason for Enero’s low share price is its inability to pay dividends. This relates to a historical agreement with the vendors of its acquisitions. A key contributor to Enero’s near death experience in 2010 was its large deferred consideration liability for acquisitions made. Enero underwent a restructure and capital raising with earnout agreements modified to restrict Enero from paying dividends or buying back shares until the earlier of September 2018 or when they have been paid. With Enero’s cash build up and unused franking credits, being unable to pay dividends is not ideal.

Fortunately, the deferred consideration liability is down to $5m. We believe management may be able to renegotiate the vendor agreement to bring forward the payment of dividends (presumably at a small cost).

Value Extraction

With 2017 expected to produce five cents per share of profit and low capital requirements, the company should be able to pay out all of its profit as a fully franked dividend. This would lead to a 5% fully franked dividend yield, which should grow as earnings recover after Brexit induced weakness.

We also estimate that the company has about $20m excess cash (i.e. cash not required for the day to day running of the business). So we will be encouraging management and the board to use this cash to pay a fully franked special dividend, which would equate to 23 cents per share.

This article first appeared on the Forager Bristlemouth blog (VIEW LINK)

The aticle is a modified extract from the March 2017 quarterly report (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Daniel joined Forager in April 2016 as a senior analyst / portfolio manager for the Australian Fund. He is an avid value investor having previously worked at Investors Mutual and MMC Asset Management. He has a Bachelor of Commerce degree (Accounting and Finance) from the University of New South Wales, and is both a qualified Chartered Accountant and a CFA® charterholder.

2 topics

1 stock mentioned

Daniel Mueller

Senior Analyst/Portfolio Manager

Forager Funds

Daniel joined Forager in April 2016 as a senior analyst / portfolio manager for the Australian Fund. He is an avid value investor having previously worked at Investors Mutual and MMC Asset Management. He has a Bachelor of Commerce degree...

Expertise

No areas of expertise

Daniel Mueller

Senior Analyst/Portfolio Manager

Forager Funds

Daniel joined Forager in April 2016 as a senior analyst / portfolio manager for the Australian Fund. He is an avid value investor having previously worked at Investors Mutual and MMC Asset Management. He has a Bachelor of Commerce degree...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment