US bond yields heading higher in 2018

Elizabeth Moran

Elizabeth Moran Consulting

In this second of a three-part series from guest contributor, ex ANZ Chief Economist, Warren Hogan, this note assesses the outlook for US bond yields and explains why the US 10 year Treasury yield could be heading for 3.50%.

Rates still at historic lows while conditions are improving

The long-awaited normalisation of global monetary policy is now underway with many of the world’s leading central banks starting to lift short-term rates off the zero floor.

The recovery from the GFC has been a long hard slog, but a synchronised upswing in global growth offers hope that a return to more normal macroeconomic conditions is near. Even unconventional monetary policies are being earmarked for withdrawal. Despite improving economic conditions and less stimulatory monetary policy, long-term interest rates remain near historically low levels.

Another bond market conundrum is upon us

The new conundrum for the US bond markets is why long-term interest rates are not rising despite the Fed raising short-term rates as well as signaling a reversal of QE over the years ahead.

The recent confirmation testimony from incoming Fed Chair Powell made it clear that he expects the FOMC will continue to raise the funds rate while gradually winding back the portfolio of securities the Fed has accumulated as part of QE.

You would think investors would be running for the hills in anticipation of higher short-term funding costs combined with the removal of one of the biggest buyers in the market.

This conundrum is critical for global bond yields because the US market is the benchmark from which all other markets are priced. What happens in the US impacts interest rates just about everywhere else. Not only is the US dollar the world’s primary reserve currency, but the US debt capital markets are the largest and deepest in the world.

How do we make sense of this conundrum?

“It’s the economy stupid…..”

What determines the level of interest rates is what is happening in the economy, specifically, the real rate of growth of the economy plus inflation. Real economic growth plus inflation broadly equates to nominal growth. An economy experiencing a very slow rate of growth will tend to have low-interest rates while an economy that is growing strongly will create forces that put upward pressures on interest rates. This is Economics 101.

The long-term interest rate should reflect the market’s view of nominal economic growth over the next 10 years. But this requires perfect foresight, which none of us have. So, the 10-year bond yield will reflect investors’ expectations for future growth which is strongly influenced by what has happened in the past and what is happening right now.

The episode of the great inflation of the 1970s is an example of how investors can get it wrong. They were universally caught off guard by the big rise of inflation in the 1970s. As a result, bond yields failed to keep up with rising inflation right through to the late 1970s. In this period, bond yields were generally lower than nominal growth.

Then in the 1980s, investors were surprised with the decline of inflation. In this period, bond yields tended to be higher than nominal growth.

This relationship is general in nature and does not attempt to account for other factors which can influence the level of interest rates in the short term. The proposition here is that nominal growth is an anchor in determining the level of interest rates in the economy.

Chart 1 shows the nominal rate of growth of the US economy since the 1960s and the 10 year Treasury yield. The relationship is quite clear. The 10 year rate can diverge from nominal economic growth in the short run. Over the long run however, they will tend to converge. To support the point, since 1962, the average level of the 10 year Treasury yield has been 6.25% while the average rate of nominal growth has been 6.57%. This is a remarkable alignment over such a long period (almost 60 years), especially when one considers that the 10 year bond yield has fluctuated between 1% and 16% in this time.

Chart 1: The US long-term interest rate and nominal growth

Source: Warren Hogan, BEA, Federal Reserve

… plus a little bit of QE

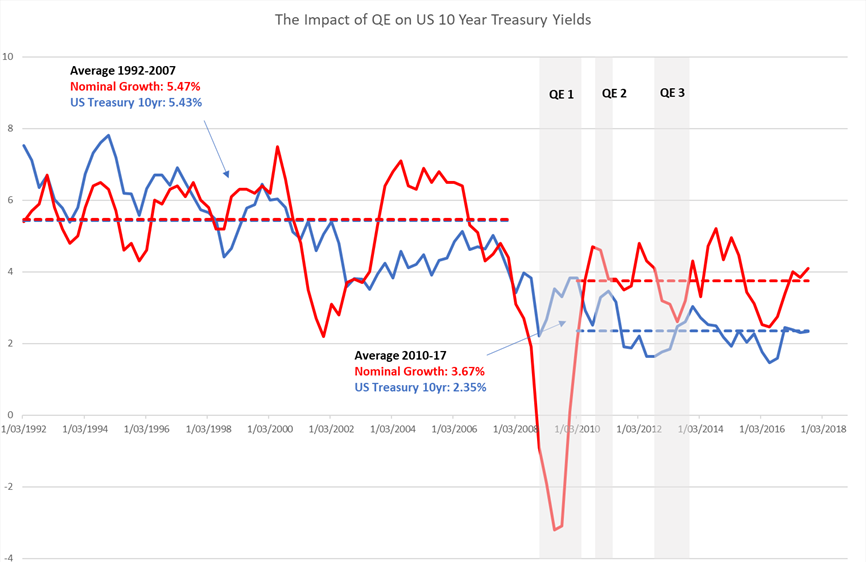

More recently, the relationship between nominal economic growth and the 10 year bond yield has been complicated by Quantitative Easing. For the first time since the 1970s, bonds yield have been persistently below the nominal growth rate in the US. That is to be expected given that the whole objective of QE is to put downward pressure on long term interest rates once the short term interest rate reaches the zero boundary.

It is clear from Chart 2 that QE has ‘dragged’ the 10 year bond yield to a level lower than otherwise would have been the case:

- In the two economic expansions prior to the GFC (1992-2000 & 2001-2007), the nominal growth rate averaged 5.47% and the 10 year bond yield averaged 5.43%, precisely as expected nominal growth and term rates aligned

- In the current economic expansion (since 2010), the average nominal growth rate has been 3.67% while the 10 year bond yield has fallen, on average, to 2.35%

Chart 2: The impact of QE on nominal growth and long term interest rates

Source: Warren Hogan, BEA, Federal Reserve

This simple framework allows us to say with some confidence that QE has been, and is still, keeping long-term interest rates below a ‘normal’ level. Normal defined as the historical tendency for 10 year rates to converge towards the nominal rate of growth of the economy over the course of the economic cycle.

This makes the current conundrum all the more remarkable

Over the past seven years, the 10 year Treasury yield has, on average, been approximately 130bps lower than what the analysis above would regard as ‘normal’. In this environment, one could be mistaken for thinking that investors would be very sensitive to any tightening of monetary conditions. Indeed, the mere talk of ‘normalisation’ could spark a significant sell off in bond markets.

When QE was implemented the market reaction was swift. In each of the three episodes of QE (marked in Chart 2), the yield on government bonds declined ahead of the actual purchases of bonds. Once the Fed purchase programs got underway, the bond yield stabilised at the new lower level or even rose a little bit.

When introducing QE, the markets were extremely forward looking. But in the current episode of QE withdrawal, the markets are not forward looking; if anything they are disbelieving.

There have certainly been numerous commentators and analysts who have warned of a bond market bubble and the risk of a disorderly adjustment in debt markets on any turn in the Fed’s monetary policy cycle. The market volatility known as the ‘taper tantrum’ was in response to then Fed Chair Bernanke’s suggestion that QEIII would soon come to an end.

So why in late 2017, is the market confounding everyone by holding term bond yields so stable in the face of both a rising funds rate and the rundown of Fed holdings of bonds? Here are some possible explanations:

- Markets don’t believe the Fed or at least don’t believe they can follow through with their plans for monetary policy. In this view, the economy will soon weaken in response to tighter monetary policy. This will halt the current cycle of rate hikes (and even force rate cuts again) while QE unwind will be put on hold. This view can also be framed as the market expects nominal growth to be much lower over the next 10 years compared to the recent past.

- In a world of low inflation and high demand for long-term yield, the way the FOMC executed QEI through III meant that markets had to ‘get ahead’ of the Fed. Specifically, the Fed bond purchases were in the secondary market. Market makers and investors rushed to own the bonds that the Fed would eventually buy from them. QE withdrawal will happen when a security matures, and the Fed does not reinvest the proceeds. In this process, there is no obvious trade for market participants to be short the bonds the Fed is letting go. They will just roll off and the US Treasury will issue a new, presumably longer term security.

I have much more sympathy for the second perspective. It explains how the markets have reacted to QE in the past and more importantly, implies a gradual response to QE withdrawal as the supply/demand balance for long term debt changes.

US Monetary Policy in 2018 will maintain upward pressure on global bond yields

The Fed is set on a path of interest rate normalisation. The FOMC’s ‘dot plot’ is projecting a funds rate of around 2.5% to 3% by 2020 which includes another 1% of rate hikes by the end of 2018.

We should believe the Fed on this. Only a disruption to the US economic expansion will meaningfully change this course for short-term interest rates.

The wind-down of the Fed’s balance sheet will really start to impact in 2018. The withdrawal of QE was only announced in September this year. The Fed’s balance sheet is currently just under USD4.5trn. Approximately USD2.5trn of this is in Treasury securities of which USD1.4trn is maturing in less than five years.

Once in full swing, the Fed will allow up to USD50bn a month of securities to leave the market, that is, approximately USD600bn a year. If the FOMC stick with the current plans, then the ‘normalisation’ of the Fed’s balance sheet will be almost one third complete in the next few years.

There have been numerous attempts to quantify the impact of QE on long rates by central banks and private financial institutions as well as academics and think tanks.

My assessment is that the order of magnitude of the impact of removing QE is in line with the nominal growth framework put forward above. This means that QE withdrawal alone should push the US 10 year Treasury security up by about 1% over the next few years.

The US 10 year Treasury yield can reach 3.50% in this cycle

To get the US 10 year yield back up to 3.5% in the next 12-18 months requires three supporting propositions.

- The US economic expansion continues generating nominal economic growth of around 3.75%, which is precisely what it has averaged in the past seven years (Figure 2).

- The downside risk to this projection is a major disruption to the economy, most likely from geopolitical conflict but potentially due to a new financial crisis - the seeds of which have been sown by super-easy monetary policies since the crisis.

- The upside risk is that the expansion gains real traction, most likely through a broad-based housing construction upswing and nominal economic growth is stronger and more persistent than the central case.

The risk tilt is 2 to 1, that is, I believe the upside risk is twice as likely as the downside risk on a 12-18 month horizon. The Fed continues to increase the funds rate as projected by the current FOMC ‘dot plot’. This will take the funds rate above 2% in 2018 and near 3% in 2019.

QE withdrawal occurs as flagged. The Fed’s balance sheet falls below USD4trn in 2018 and is on track for full ‘normalisation’ within 10 years.

Global yields will be impacted

While policy normalisation will be much slower in the other major central banks, specifically the Bank of Japan (BoJ) and the European Central Bank (ECB), the US yield push higher will ‘re-set’ the base for global markets. All long-term bond yields will be dragged higher, even if many markets see yields move below those in the US. As long as the global economy continues to expand and inflation remains stable or even moves a bit higher, the policy actions of the US Federal Reserve should ensure a modest rise in global long-term interest rates over the course of 2018.

In the final article of this three-part series I will bring together these global perspectives, with the outlook for Australian short-term interest rates as described in artilce 1: "Why Australian interest rates will rise in 2018", to assess prospects for Australian bond yields in 2018.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

5 topics

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Comments

Comments

Sign In or Join Free to comment