Value or Growth - why not have both?

The small-cap index returned 10.2% in November, spurred on by three separate positive vaccine announcements and the US election outcome. Whilst this performance was impressive, it is notable that the small-cap US Russell 2000 index rose 18%. Strong returns from unloved value stocks in the financial, travel and resources sectors sparked debate on whether we are at the tipping point of a value/growth rotation.

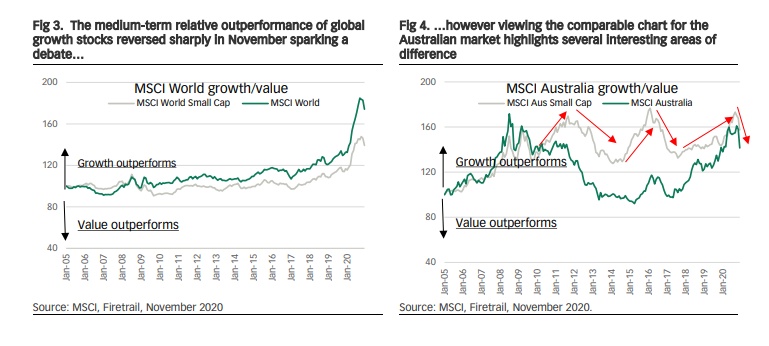

The recent outperformance of growth stocks has been driven by rerating AND earnings growth

Growth stocks have performed remarkably since early 2017 to October 2020, with the MSCI world global small-cap growth

index rising 49.7%. Over the same period, the value index returned -0.2%. A COVID driven acceleration of structural trends, such

as the shift to online, and expectation of lower interest rates saw a trend that began in early 2017 accelerate in 2020. Though

the outperformance of growth has been partially driven by valuation re-rating, it is also a function of earnings growth. On

average, growth stocks have delivered superior earnings growth relative to value stocks over the past several years.

Australia is unique

The differences between Figures 3 and 4 clearly demonstrate that Australia is unique in terms of the relative performance of

value and growth stocks. At a high level, the following observations can be made:

- Australian small caps have diverged from large. The relative performance of growth and value indices in the Australian small-cap market has diverged from the large-cap index, particularly when compared to equivalent global indices. The Australian small-cap index has displayed shorter, sharper cycles of relative growth/value performance with three clear ‘mini’ cycles since mid-2019

- Australian value has fared much better on a relative basis. Since 2009, the relative performance between Australian growth and value indices has been broadly similar, while at the global level growth has outperformed value by ~50%. This is perhaps not entirely surprising when we consider the performance of the mega-cap US technology stocks over the past decade.

What is causing this difference?

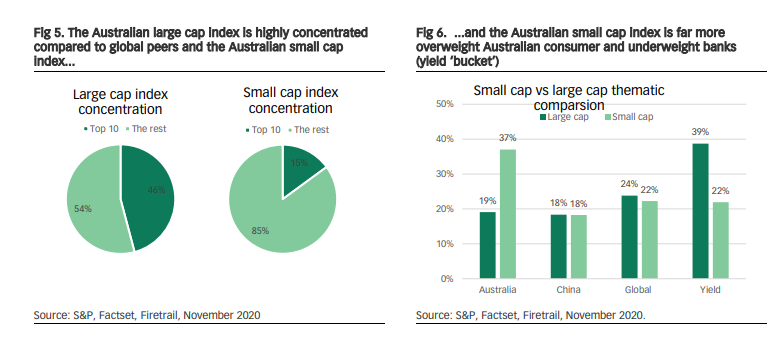

With such divergent data sets, it is worth considering the potential drivers and implications for small-cap investors. The Australian market is unique versus global benchmarks for two key reasons:

1. Concentration. The Australian large-cap index is one of the most concentrated in the world, with the top 10 stocks accounting for around 45% of the total index. We are familiar with most in our daily lives - the big four banks & MQG, supermarket chains, CSL and BHP/RIO.

2. Resources punch above their weight. As a function of our unique geological endowment, Australia has high exposure to resources companies across both small and large-cap benchmarks. Resources are typically viewed as ‘value’ stocks, hence their relatively strong performance may go some way to explaining why Australian value indices (and the Australian economy for that matter) have outperformed global counterparts.

The small-cap market in Australia is different to the large-cap market in two key ways:

- More diverse. The small-cap market is far less concentrated, with the top 10 stocks in the index accounting for <15% of the total (vs 45% for large caps).

- Less banks, more consumer. On a relative basis, the small-cap market is underweight banks and far more leveraged to a diverse range of Australian consumer-exposed stocks.

Key takeaways for investors

In our view, for small-cap investors, there are two major implications. Firstly, investing in both growth and value stocks is required in order to deliver consistent alpha generation through cycles

“History doesn’t repeat itself but it often rhymes” – Mark Twain.

Secondly, the small-cap market offers a much more diverse set of alpha drivers that are able to be exploited.

A bet each way please

Looking forward, we see strong arguments for both continued outperformance of value stocks and reversion to the growth dominance of the past few years. The good news for investors is that we do not have to choose! A key advantage of all Firetrail strategies, including the small companies fund, is that we are unconstrained. That is, we invest in both value and growth stocks in all sectors of the market. The goal is to ensure that returns are determined by stock-specific risk, rather than factor risk, such as a ‘bet’ on factors such as growth vs value.

Every investment-grade company has a price

Picking the turning point on growth vs value cycles is as difficult as timing the market… near impossible! Our efforts remain focussed on finding and investing in companies that we believe are trading at cheap valuations, regardless of whether they are characterised as ‘value’ or ‘growth’. A core part of our philosophy is that every investment-grade company has a price - so long as it meets certain quality requirements there is a price at which we will consider adding it to a portfolio of our best small-cap ideas.

Earnings matter

Importantly, over the long term, whether value or growth, the key determinant of what drives share prices is earnings, rather

than the multiple put on those earnings. With the benefit of hindsight, many of the large US technology companies (responsible

for driving growth factor returns) have justified their historic valuations with strong compound earnings growth.

Invest in Value and Growth

Fundamental analysis is the best way to capture all the different opportunities available in the market through time. To find out more about what's on Firetrail Investments' radar, click the 'FOLLOW' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matthew is a Portfolio Manager at Firetrail Investments for the Firetrail Australian Small Companies Fund. Matthew’s primary sector responsibilities are Resources and Industrial Small Companies. Matthew has over 13 years’ relevant industry experience.

1 topic

1 contributor mentioned

Matthew is a Portfolio Manager at Firetrail Investments for the Firetrail Australian Small Companies Fund. Matthew’s primary sector responsibilities are Resources and Industrial Small Companies. Matthew has over 13 years’ relevant industry...

Expertise

Matthew is a Portfolio Manager at Firetrail Investments for the Firetrail Australian Small Companies Fund. Matthew’s primary sector responsibilities are Resources and Industrial Small Companies. Matthew has over 13 years’ relevant industry...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The shift toward scarcity: a playbook for a new era of investing

Talaria Asset Management