TOL - 24th Nov, 2020

Value ready for catch-up

Nothing lasts forever, in particular not in financial markets, or as I like to put it: this too shall pass, eventually.

With “this” I am referring to the relentless, and extreme, bifurcation of equities into “winners” and “losers”, with very few shades of grey in between, certainly since the arrival of the pandemic.

Before the virus hit economies and life as we knew it up until that point, many a market expert had already observed the distance between “popular” and “unpopular” had probably never been recorded as wide as it had become.

Since the arrival of the virus, however, the distance between the two opposing categories of equities has only widened further.

Now we really can conclude the gap between Winners and Losers, Growth & Quality versus Value and Cyclicals, might have never in the history of financial markets been pushed out as far as it has in 2020.

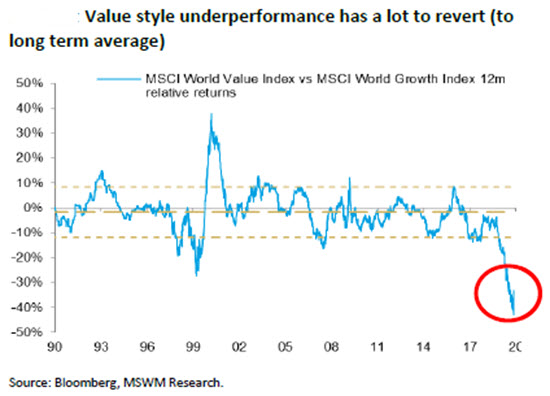

Just about every market researcher has published a chart to illustrate equity markets’ extreme polarisation in recent years, and many of them are updating the data this month.

The example I picked below is from Morgan Stanley. It shows how much further the elastic band has been stretched; much, much further than at any other point over the past three decades.

****

The theme of share market polarisation is far from new.

The current dynamics favouring Growth & Value started during the GFC, initially in the US where the origin of that crisis -housing and finance companies- gave way to global tech giants and emerging new technologies.

Australia caught up after the euro-crisis of 2011/12. First gradually, then relentlessly with companies such as Xero ((XRO)), Afterpay ((APT)) and NextDC ((NXT)) climbing up the rankings of the ASX200, while large cap energy producers, the banks, and property owners ended up as the proverbial ball-and-chain throughout the elongated bull market.

It has been a torturous seven years for many an investor who likes to pick up “cheap” looking value stocks, with rather brief periods of relief along the way. Which is but one reason as to why many today are looking forward in full anticipation.

Could it be? Can 2021 finally bring the turnaround that switches market momentum from expensive looking winners into the beaten down cheaply priced stocks in markets?

The chart above suggests such a narrowing of the gap, at the very least, is long overdue.

****

The answer, this time around, may well be provided by corporate results and AGM updates post August reporting season.

Thus far, corporate updates and announcements in November have created a positive news flow, which in return is feeding into a distinct wave of upgrades for earnings expectations in Australia.

For example, the FNArena Corporate Results Monitor (see further below) is currently showing 44.7% of companies reporting financial performances are beating market expectations with an additional 21.1% performing in-line with consensus forecasts.

These numbers do not include trading updates and AGM commentary which are equally contributing to the current upswing in market forecasts for next year’s corporate profits.

What makes the current turnaround different from the recent past is it is no longer exclusively carried by Winners like Xero, Afterpay et al. This time around Amcor ((AMC)), AusNet Services ((AST)), EclipX Group ((ECX)), GrainCorp ((GNC)), CSR ((CSR)), and News Corp ((NWS)), among many others; they are all forcing analysts to lift estimates for the year ahead.

The importance of this lays with the difference in relative valuations: the Winners are still performing well, but their share prices are already reflective of it. The laggards have now started to build up positive momentum, but in most cases their share prices are much more cheaply priced.

This is why investor expectations are growing for a general revival of the “Value” part of the markets. Think banks, small caps and cyclicals, and mining and energy stocks.

****

As businesses increasingly return their focus towards post-covid and growth, the return of M&A deals is one logical consequence, and one straightforward reason to get excited about exposure to Value stocks again.

All of AMP ((AMP)), Coca-Cola Amatil ((CCL)), Link Administration ((LNK)), the Vitalharvest Freehold Trust ((VTH)) and Village Roadshow ((VRL)) have seen corporate suitors come knocking on their door recently.

Many more deals should be expected as forthcoming.

Again, here too, one important detail is the willingness of share market laggards to restructure and to invest in order to leave behind the malaise of recent years, and (finally) unleash/create value for shareholders.

One prime example of exactly such a beneficial restructure was announced by long-term shareholder disappointment Telstra ((TLS)). The decision to restructure all operations into three separate divisions instantly opens up a variety of options, including selling the farm, or substantial parts of it, to the highest bidder.

One logical and straightforward way to look at the potential benefits from the restructure for shareholders is through Telstra’s balance sheet: the mobile towers are currently valued at $280m while their true market value is estimated at $4bn, or close to that figure.

Telstra’s balance sheet currently has the fibre, ducts and pipes valued at $9.8bn versus an estimated market worth of circa $28bn.

A similar no-holds-barred corporate transformation is taking place at mortgage-lender Resimac ((RMC)) which, through partnerships with four technology providers, is reinventing itself as a lower-cost, digital fintech.

Resimac recently acquired IA Group. Perpetual ((PPT)) purchased Barrow Hanley and Trillium in the US. Nine Entertainment is investing in Stan Sports, while Pendal Group ((PDL)), formerly known as BT Investment Management, has publicly explained its ambition to grow funds under management by 50% over the next five years.

These are but a selection from recent announcements, but the message to investors seems obvious: Value stocks are no longer simply a victim of the times, best ignored. With a little bit of optimism added, they can easily become the next source of share market excitement.

****

Economies in countries like the UK, France, Austria and Belgium are facing another uncertain time of lockdowns, but the world will survive and learn how best to deal with covid, one way or another.

Financial markets, looking forward beyond the immediate obstacles, have thus already absorbed the initial bouts of investor optimism.

As every student of financial history knows, economic recoveries go hand-in-hand with value stocks outperforming their Growth & Quality peers, as well as the broader share market indices.

Next calendar year should present the global recovery. To what extent this translates into a broad boost for the 2020 share market laggards remains very much dependent on the shape and speed of that recovery.

But some are already dreaming of the Biggest Boom in Modern History. Certainly, there is potential for upside surprise in 2021 and if everything falls into place, share market momentum can temporary become as one-sided as it has been with this time Value in favour.

Imagine the quick roll-out of a vaccine, with governments and central banks continuing to provide stimulus and liquidity, while businesses are restructuring, becoming leaner and better adapted, while consumers start spending their savings, and those businesses spend on capex and expansion.

The effect of all these factors combined would not only be much higher growth than is currently forecast by most, it most likely would trigger market concerns about inflation, pushing long bond yields higher, which is one additional factor in favour of Value and negative for Growth & Quality.

A broader economic recovery next year also favours Emerging Markets (EMs) over developed markets, as well as Australia over the US, while the US dollar should weaken, creating yet another obstacle for offshore operators on the ASX, which are mostly labelled Growth and Quality.

****

Investors should remain cognisant, however, the above forecast would be the most optimal outcome. As many question marks remain, with many more subdued scenarios equally likely, it’s probably best to remain level-headed and risk-aware.

Equally important, while this year’s pandemic, and the prospect for next year’s recovery, have unexpectedly intervened in the dominant dynamics that have benefited the cohort of Big Tech, new technology disruptors, and High Quality performers, the tectonic changes in support of these companies will still be around, economic recovery or not, and with or without a vaccine.

As such, I remain of the view the best approach for investors is through combining both market opposites in their investment portfolio, and be prepared for bouts of high volatility along the way.

Extreme market positioning is likely to benefit bond yields moving higher and Value benefiting while yesterday’s Winner will not.

It will be equally beneficial for investors to understand this is but a temporary phenomenon, as the market rebalances to a less extreme set-up.

FNArena offers impartial, ahead-of-the-curve share market insights and analyses, on top of proprietary tools and applications for self-managing and self-researching investors. Our service can be trialed at (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

FNArena is a supplier of financial, business and economic news, analysis and data services.

3 topics

5 stocks mentioned

FNArena

FNArena is a supplier of financial, business and economic news, analysis and data services.

Expertise

FNArena

FNArena is a supplier of financial, business and economic news, analysis and data services.

Expertise

Comments

Comments

Sign In or Join Free to comment