Don't get barbequed this Summer

Credit is smouldering right now. When that smoke becomes fire, the door becomes a key hole and only the first few get through. The rest get burnt. Holding credit risks with your equity holdings into 2019 and 2020 seems mighty dangerous. Don’t get barbequed this season.

Credit spreads are starting to gap wider and liquidity is drying up. If the beast of credit is really awakening from a 10 year slumber we should all be collectively terrified as credit is the oil of the financial system. The policy settings that would alleviate negative credit issues are years away from helping (rate cuts and more Quantitative Easing), portfolios are already bleeding with smoke appearing, and investors are still overweight and huddled together in a crowded space. Commentary from our investment banking counterparties who specialise in credit are that 80% of enquiry is looking to sell, pricing is gapping wider (offshore financial paper by up to 0.25% without trading yesterday) and no one is stepping up to take the other side. And why would they? Credit has a long history of asymmetry with powerful positive correlations to equities markets. Mind the gap, the market settings are negative for credit into likely harder market years of 2019/2020.

The normal cycle is higher rates, wider credit, and change in equities – not this time.

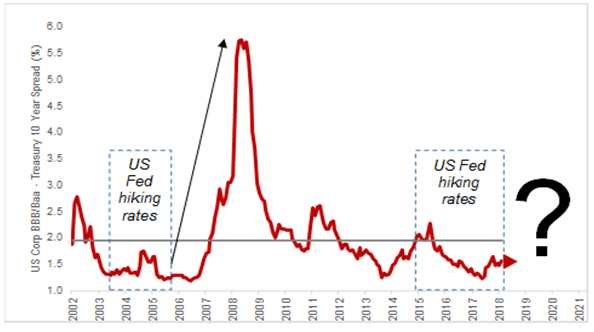

In a normal market cycle, ‘risk free’ rates rise towards cycle-end as the Central Bank raises rates to contain inflation expectations (we can tick this off in the U.S. cycle). Short-dated Government bond yields rise, but such a rise of risk free rates often leak into credit, widening credit spreads (the difference between the costs of risk free Government debt and riskier corporate debt) as spreads readjust to add credit premium. Once credit spreads start to widen, combined with higher risk free rates, equities markets re-collaborate as corporates and personal consumption is affected by higher funding costs. Credit spreads have a long history of being a fantastic lead indicator for equity performance – they widened aggressively in mid-2007, months ahead of a peak in equity markets in late 2007, and they started tightening aggressively in late 2008, a few months ahead of equity market lows of early 2009. So far in this current U.S. Fed hiking cycle, credit spreads have remained very tight. Volatility seems to have jumped direct from U.S. interest rates into equities, avoiding credit. That is highly unusual.

Why has this cycle been different? Trump tax cuts elongated the corporate cash flow cycle.

Everyone loves free money, and heaping a massive fiscal spend onto an already hot private sector market certainly got the corporate cash flow party started in early 2018. Baseline effects were of the magnitude of a 500 basis points kicker to corporate cash flows coming straight off the U.S. Government’s balance sheet. Credit has held its ground despite higher risk free rates, as corporates have been swimming in ‘tax cut’ cash and re-calibrating their default risk, which hasn’t been warranted until now. With the Democrats regaining control of the House, we expect the credit party has just been shut down as Trump’s ability to spend is curtailed by a hostile House. Trump can no longer buy votes by giving away money to be repaid another day. Year on year change goes from a baseline of +500 basis points to zero. From here on, the cycle should behave in a far more normalised way, where credit delinquency from higher rates starts to bite. In the U.S., housing and autos are already in significant decay.

Credit quality is weak, covenant quality is thin, and liquidity is appalling. If that beast of credit awakens, you’d better run and keep running until the Fed cuts rates or restarts more Quantitative Easing.

More than half of all U.S. investment grade debt is rated BBB, one notch above junk, making it highly susceptible to a credit ratings downgrades. Such a move would trigger forced liquidations from investment grade only products, many of which are housed in ETF products. The amount of asset protection underpinning high-yield credit contracts is at the weakest point in the cycle viewed through the prism of covenant lite issuance, and on top of these negatives – secondary market liquidity is one sixth of the size of liquidity that was available into the last crisis. So the structure of the market is twice as much corporate debt outstanding, more than half at a lowly BBB credit quality, but only 17% of the available liquidity from the prior crisis to serve twice as much outstanding debt. It doesn’t take a genius to identify the obvious flaws in this set up. When that smoke becomes fire, the door becomes a key hole only the first few get through. The rest get barbequed. Adding those risks to your equity holdings into 2019 and 2020 seems mighty dangerous.

What’s the trigger?

Refinancing seems the likely trigger. 16% of companies in the Russell 3000 are ‘zombies’ – defined as firms that are unable to cover debt servicing costs from current profits. Will it be GE, the poster child of 2000’s who’s first to get caught? Or maybe an oil company after the recent collapse in oil? Just like the Eurozone crisis of 2011, one day the market wakes up and says “Spain, Ireland, you owe us 100 billion Euro’s due for repayment next week. We don’t have faith in your credit (ability to repay) so we will not roll your debt obligations forward. Oh, and we’d like to be repaid in full next week as well.’’ This triggers a cataclysmic financial bottle neck. Weak borrowers cannot borrow to repay their debts due today and become immediately insolvent.

Would you lend your hard earned money to a company that has declining cash flows, weak sales growth and compressing margins, at close to lowest prices of the last decade? The macro market settings are not looking supportive.

BBB rated USD ‘investment grade’ spreads

Source: Bloomberg

The investment ground has shifted and isn’t coming back soon.

Just a year ago the world was enjoying a synchronised economic acceleration. In 2017, growth rose in every big advanced economy except Britain, and in most emerging economies. Global trade was surging and America was booming; China’s slide into deflation had been quelled; even the Eurozone was thriving. In 2018, the story is very different. Investors are fretting materially, concerned over trade wars and monetary policy tightening. The world economy’s major problem in 2018 has been uneven momentum. Leading economic indicators from Asian export nations have been in marked decline, coupled with weakening European data and fiscal drag in the U.S. into 2019. JCB believes all of this makes for a stark reality check and has lead the International Monetary Fund (IMF) to forecast slowing growth in 2019 in most advanced economies (excluding the U.S.). For 10 years, buying dips in risk markets has been rewarded via excess liquidity (QE), low interest rates and easy credit availability.

All of those structural elements are now gone.

The fundamental pillars supporting most asset prices are experiencing violent cracks in the framework. The investment ground of the last 10 years has disappeared. Looking ahead, JCB see that markets will face less liquidity, higher rates and tighter credit conditions, all of which should curtail economic activity moving forward. Less economic activity, combined with higher rates means credit delinquencies. Be careful this barbeque season because it’s getting hot out there.

Further insights

As we continue to face volatile market periods, bonds will offer the stability of principal and income, as investors seek the highest quality investments. Find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from 2001 in New York, Tokyo, London and Sydney, with Merrill Lynch/Bank of America Merrill Lynch. Over his career, Charles has managed large Government Bond portfolios in key major currencies and derivative instruments. During this time, he has managed through the spectrum of financial market dynamics, including September 11, 2001, the Global Financial Crisis, Eurozone crises, the US credit rating downgrade and Chinese/Greek concerns.

7 topics

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from...

Charles is a co-founder of Jamieson Coote Bonds (JCB) and oversees portfolio management of the Australian and Global High Grade Bond and Dynamic Alpha investment strategies. Prior to JCB, Charles forged a career as a seasoned bond investor from...

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management