Want to make a quick profit by shorting Australian bonds? Not so fast! This time could be different.

Recently Australian bond yields have moved below those of the US. Historically such negative spreads have tended to be uncommon and short lived. So let’s all rush out and short Australian bonds relative to US Treasuries and make some quick money. Not so fast! This time things could be different.

To see why let’s start by asking “What are the minimum conditions required to generate negative spreads?“ By negative spreads we are specifically referring to when Australian 10-year bond yields are lower than US 10-year bond yields. Allowing for the linkage between inflation and monetary policy there are arguably a couple of minimum conditions required to generate negative spreads. Firstly, the level of interest rates as defined by the official cash rate in Australia being at least the same as, if not lower than, those in the US. Secondly, inflation expectations attached to longer-dated bonds being lower in Australia than the US. Not only would it be presumed that these two factors would need to be lower in Australia but that they would need to be materially lower to generate negative spreads. Why does the differential need to be materially lower? It would be expected that to generate a negative spread a larger differential would be required to offset the country risk premium historically applied to Australia given (a) the relatively small size of the local bond market, (b) the more cyclical nature of its economy and (c) the fact that the USD is a reserve currency.

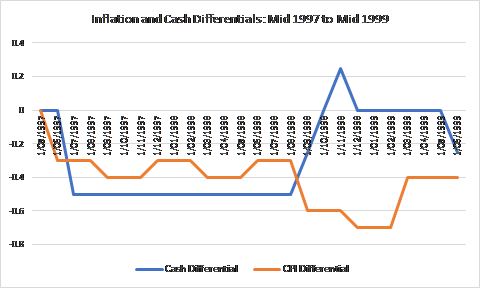

But are these conditions in themselves sufficient to generate a negative spread? To address this question, it is useful to observe when these conditions occurred in the past. While the minimum conditions previously outlined occur infrequently, such conditions did prevail in the late 1990’s when both cash rates and inflation in Australia were materially below those in the US. As Chart 1 highlights both official cash rates and inflation ranged between 0.25%-0.70% below the US from 1997-1999.

Chart 1 :

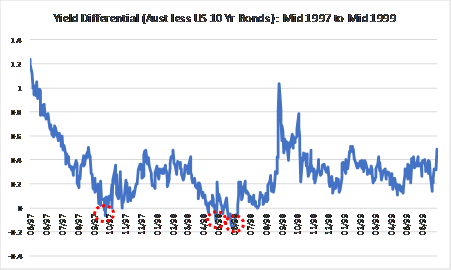

Unfortunately Chart 2 highlights that despite the minimum conditions required prevailing Australian 10-year bonds traded at an average of 0.3% above US treasuries. Though Australian bonds did at times trade at negative spreads (circled areas) such periods were episodic and didn’t persist for long. Such historical experiences lend weight to the idea of “let’s all rush out and short Australian bonds relative to US Treasuries and make some quick money”.

Chart 2 :

Can history repeat itself?

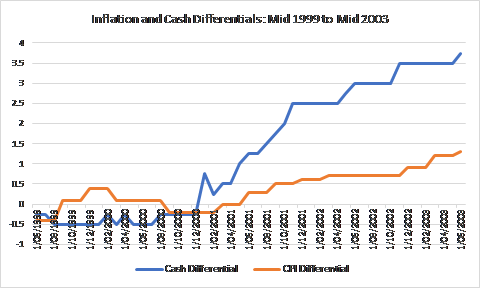

A potential stumbling block in looking at historical inflation and cash rates as drivers of negative spreads is that one risks failing to identify within which country inflationary pressures are more likely to be building; i.e. inflation expectations are forward looking. Going back to the period from 1997-1999 a key point is that inflationary pressures were building in Australia and not the US. This can be seen by the behaviour of inflation and cash differentials from 1999-2003 (Chart 3).

Chart 3 :

While cash rates in Australia remained below those in the US until late 2000, inflation in Australia began to rise above that in the US in the second half of 1999. By 2001 both inflation and cash rates in Australia were again materially higher than those in the US and continued to rise higher. Against such a backdrop of building inflationary pressures in Australia it is not surprising that bonds could not sustain negative spreads even though the minimum conditions appeared to be satisfied; i.e. sub US cash and inflation rates were not viewed as being sustainable.

Three reasons why this time should be different?

Looking out over the next 12-18 months there are several reasons why it would be expected that this time around inflationary pressures, and hence cash rates, will remain materially lower in Australia visa vis the US.

Firstly, while the next move in Australian cash rates is most likely to be up, the pace of rate rises is expected to be materially slower than in the US. Importantly this signals that with cash rates at similar levels, the Reserve Bank of Australia sees inflationary pressures as far less of an issue than the US Federal Reserve. Unlike cash rates in the post 1999 period, US cash rates are likely to continue moving relative higher compared to Australian cash rates.

Secondly, labour market underemployment rates in Australia remain materially higher than those in the US. Persistence of such a differential will continue to put downward pressure on Australian wage growth relative to the US.

Finally, recent moves by the US government to undertake additional expansion of fiscal policy are more likely to prove inflationary given the advanced state of the US economic cycle. By contrast the recent expansion in infrastructure expenditure in Australia is occurring at a time of weakening investment in residential construction thereby dampening any potentially deflationary impacts.

While recent history is less than encouraging, there are solid grounds for arguing that this time is different and that going forward Australian bonds should be able to sustain negative spreads over a more extended timeframe. Determining how large such a negative spread can become is more problematic and will depend on the extent to which (a) investors require a country risk premium to hold Australian bonds and (b) the magnitude of the inflation/cash differential. Leaving that aside the key takeaway for investors should be that, while shorting Australian bonds relative to US treasuries may eventually make money, this time around it may take a lot longer to bank that profit than historical experience suggests.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

1 topic

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment